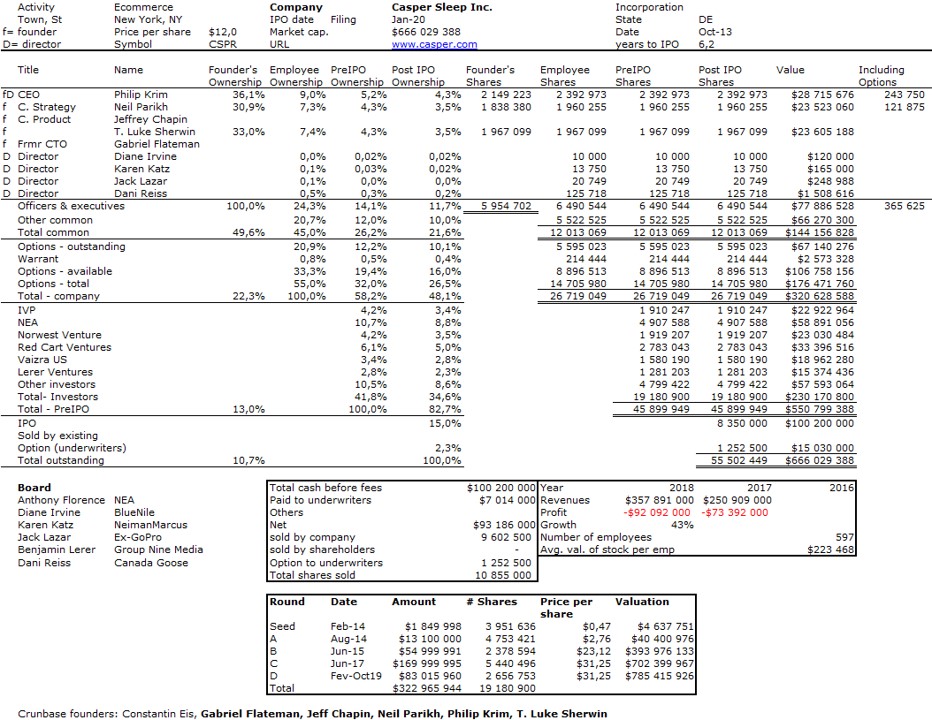

The Covid19 virus has an indirect effect, we have more time at home and in front of computers. So I updated my data in startup equity from 600 companies for which information was available, mostly because they had filed to go public. Here is the full list of individual data.

If you cannot visualize the document on scribd, here is a direct link to the pdf entitled Equity_in_600_Startups-Lebret-April2020.

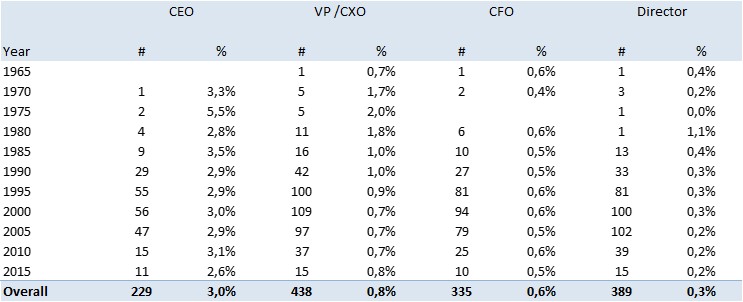

At the end of this 600+-page document, you’ll find some statistics, here they are again. I will probably come back to some results I find interesting not to say intriguing. Enjoy an react!

Some addtional comments in later posts:

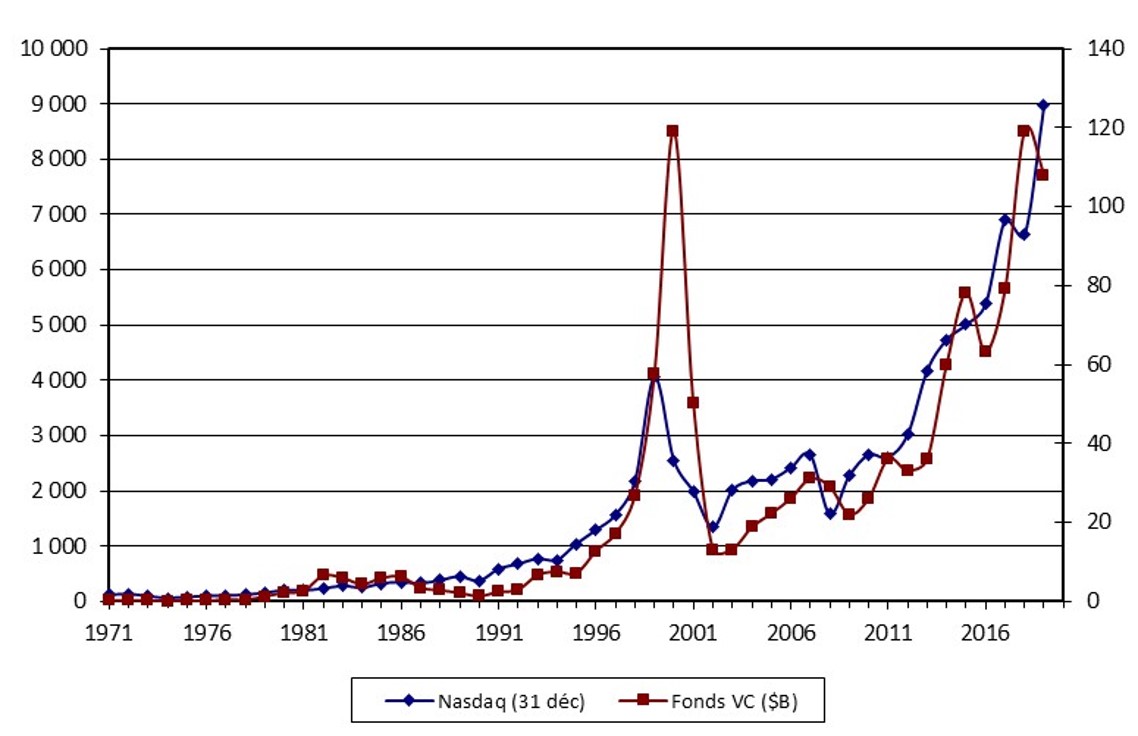

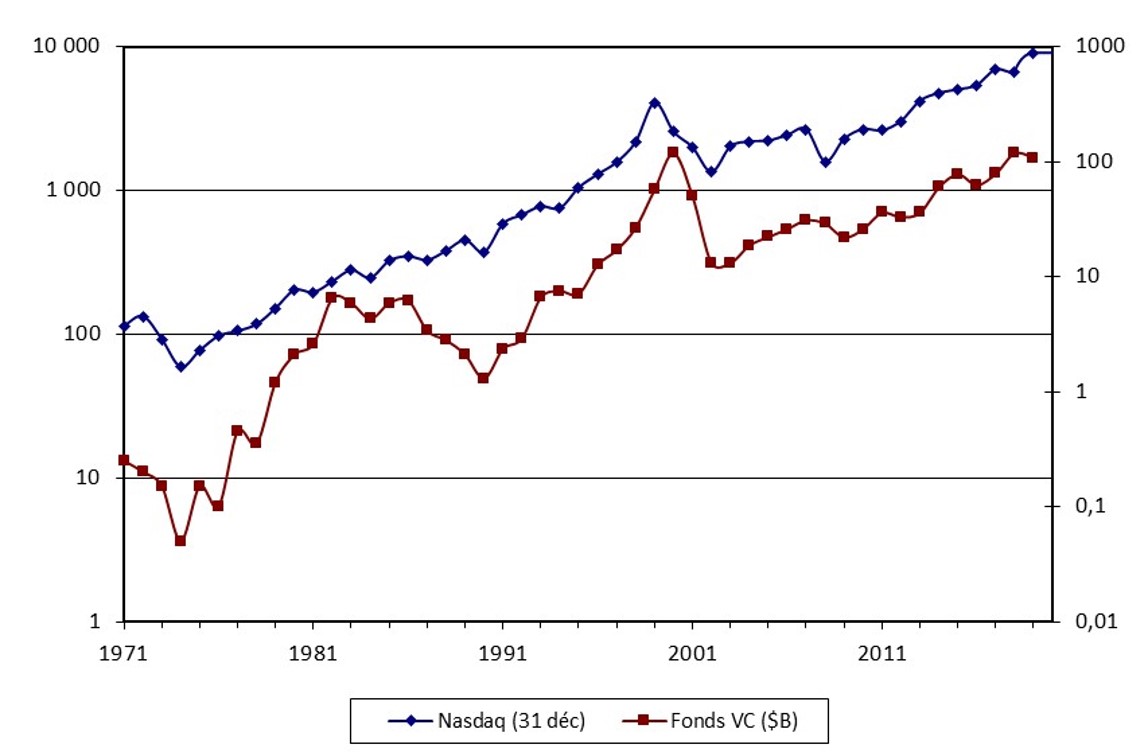

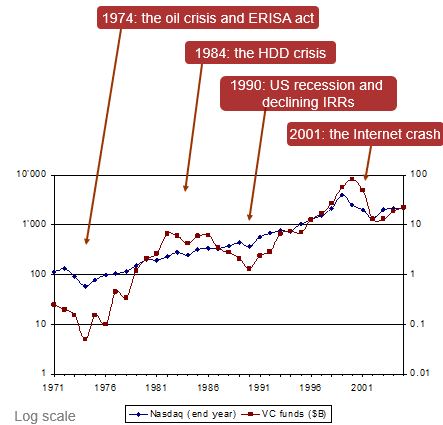

1- About venture capital: on April 7 comments 1.

2- About the age of founders: on April 8 comments 2.

3- About the equity of founders: on April 9 comments 3.

4- How is equity shared: on April 10, comments 4.

5- About the equity of non-founding CEOS: on April 11, comments 5.

6- About valuation of startups: on April 12, comments 6.

7- What have they become: on April 16, comments 7.

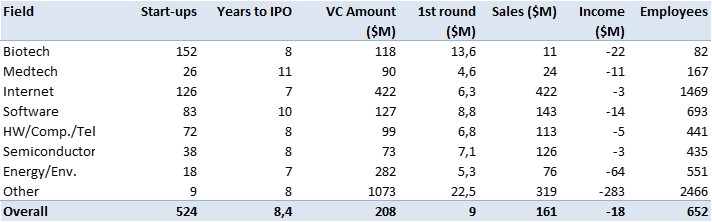

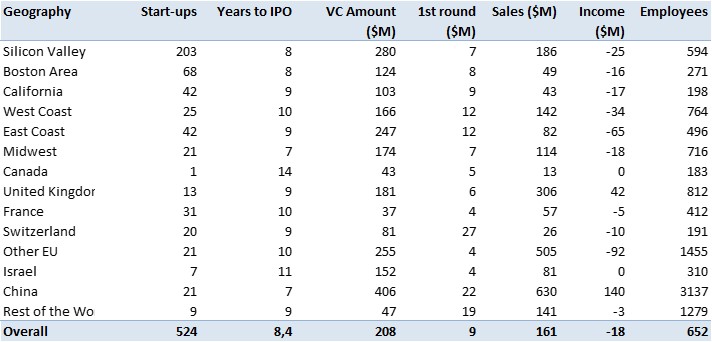

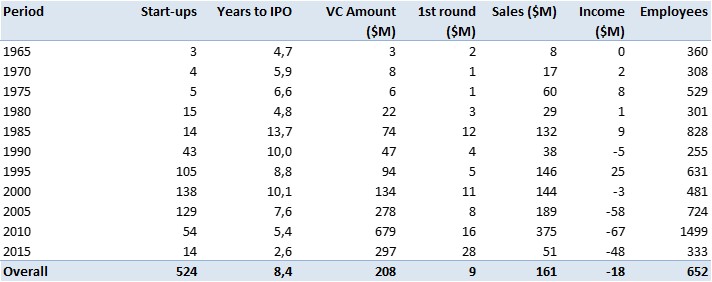

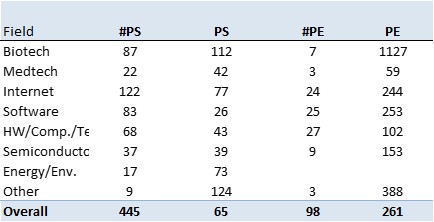

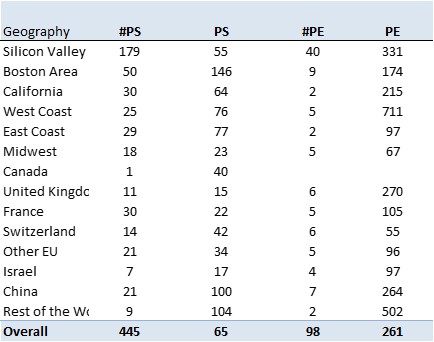

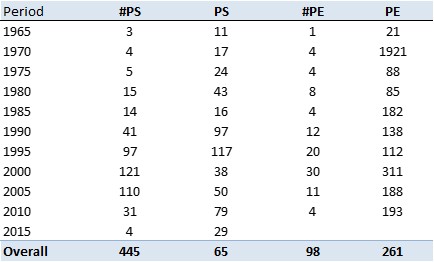

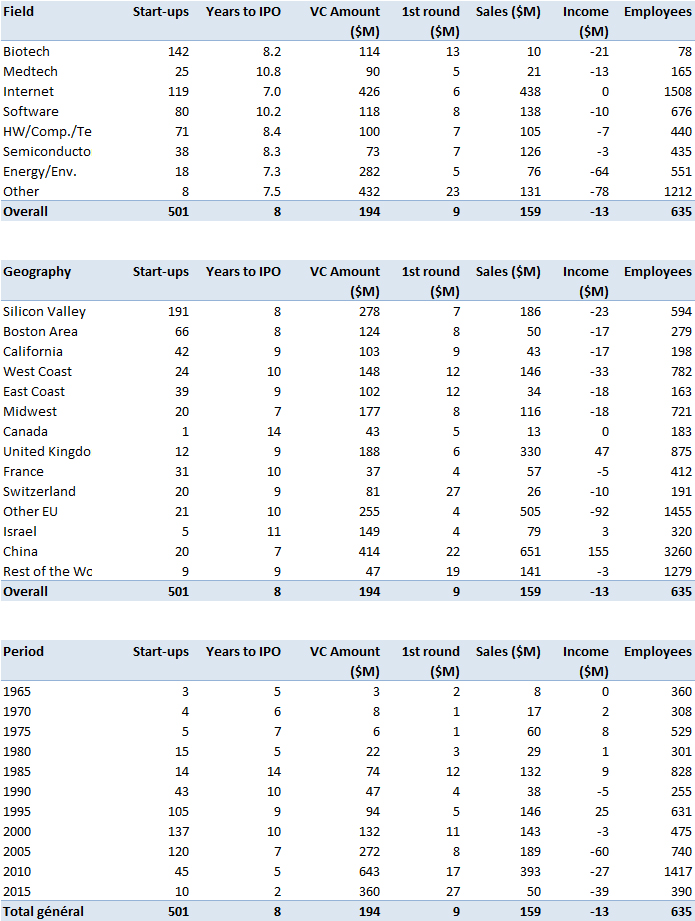

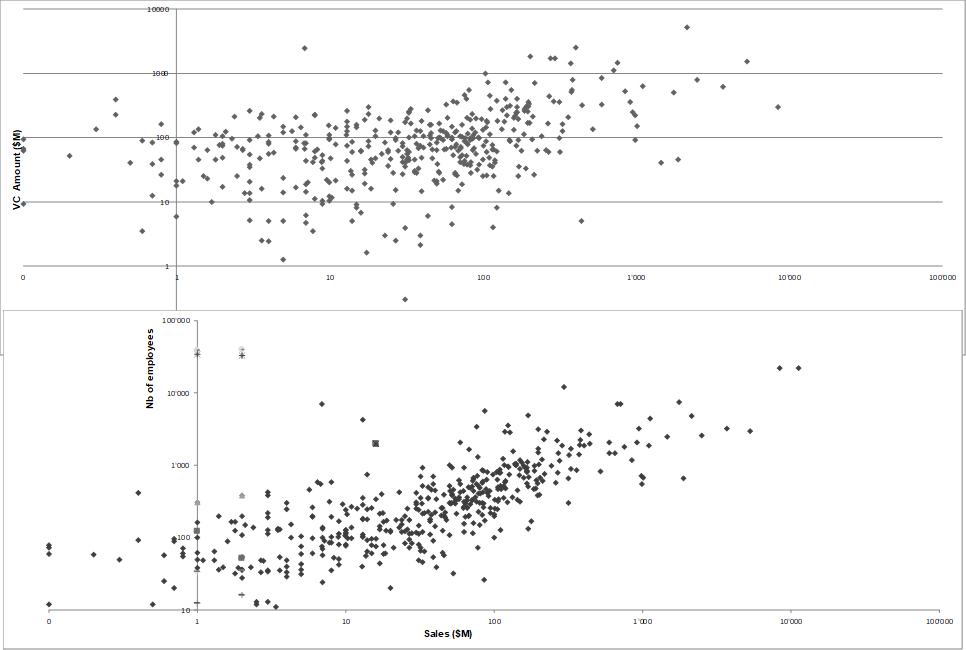

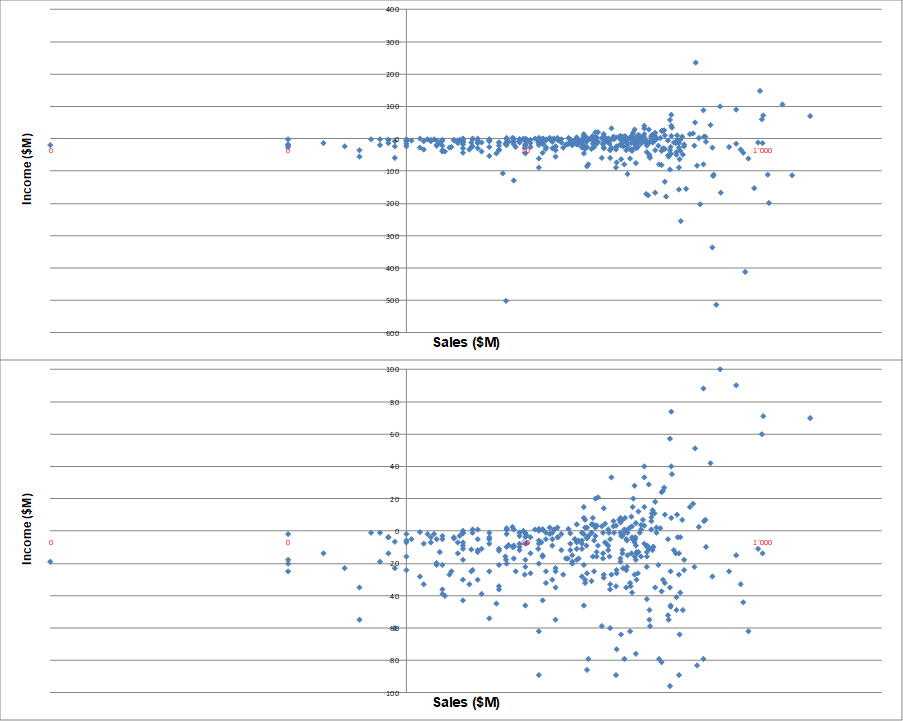

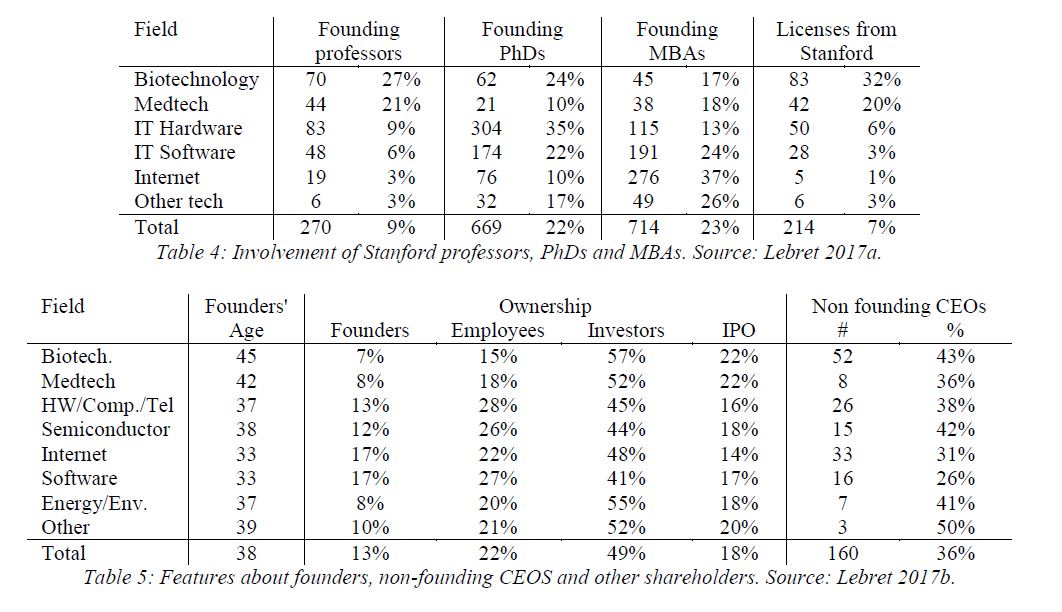

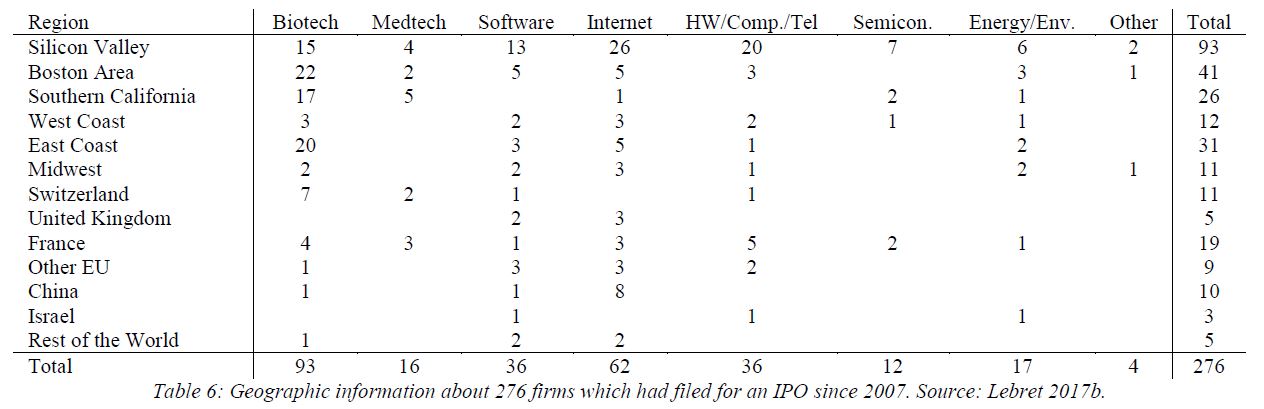

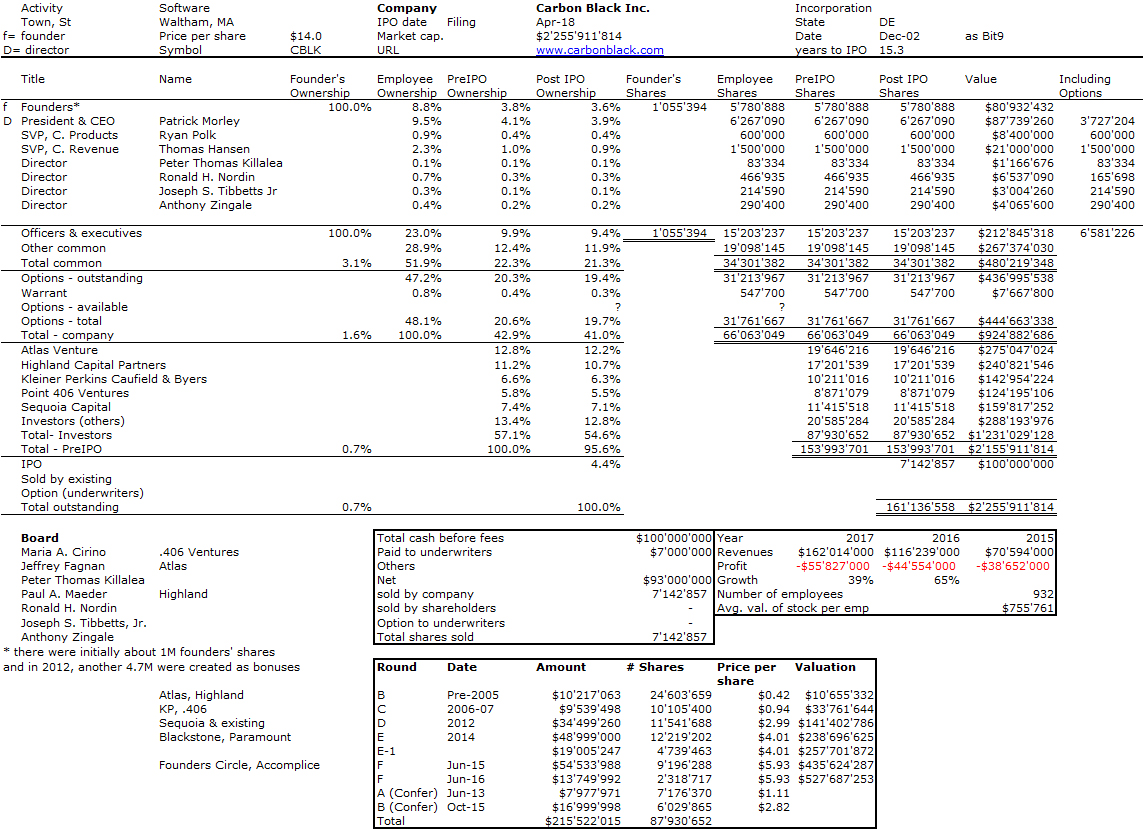

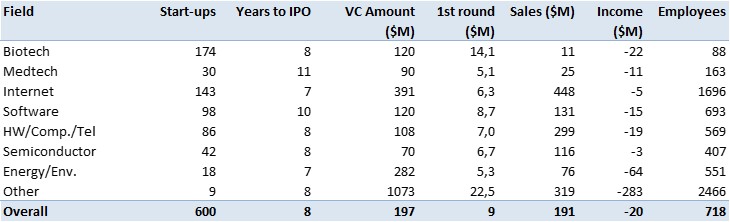

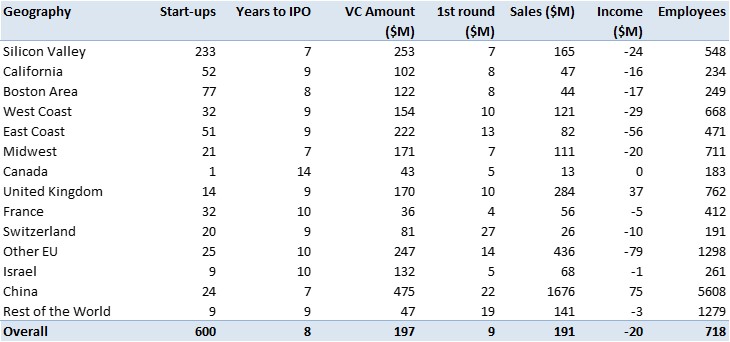

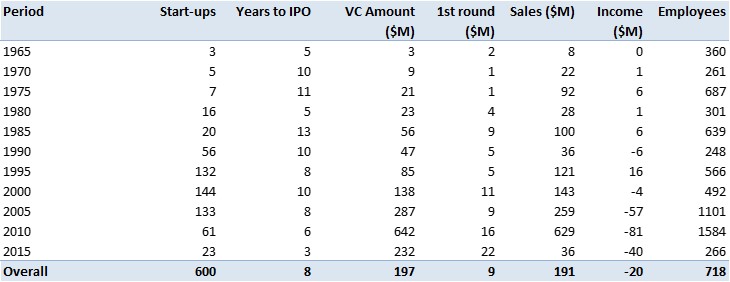

Basic data about startups (funding, sales, profits, employees at IPO and years to IPO) by fields, geographies and periods of time.

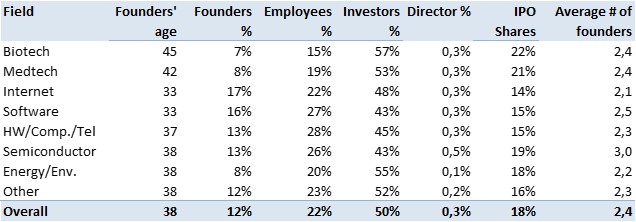

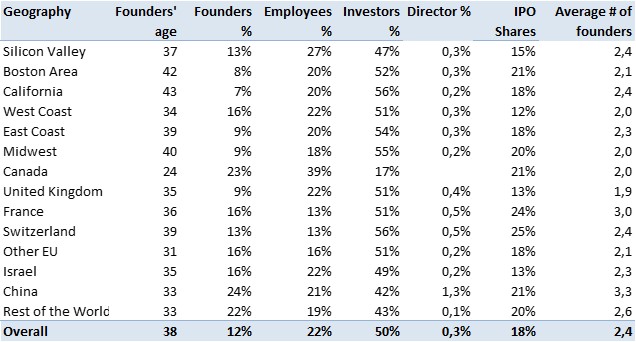

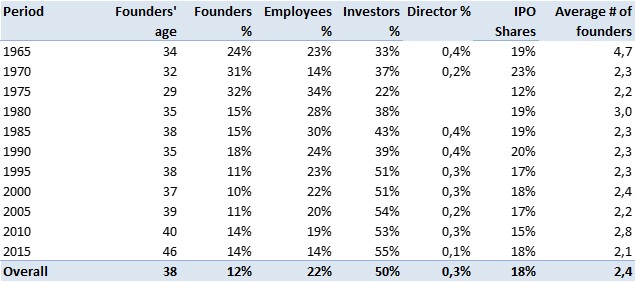

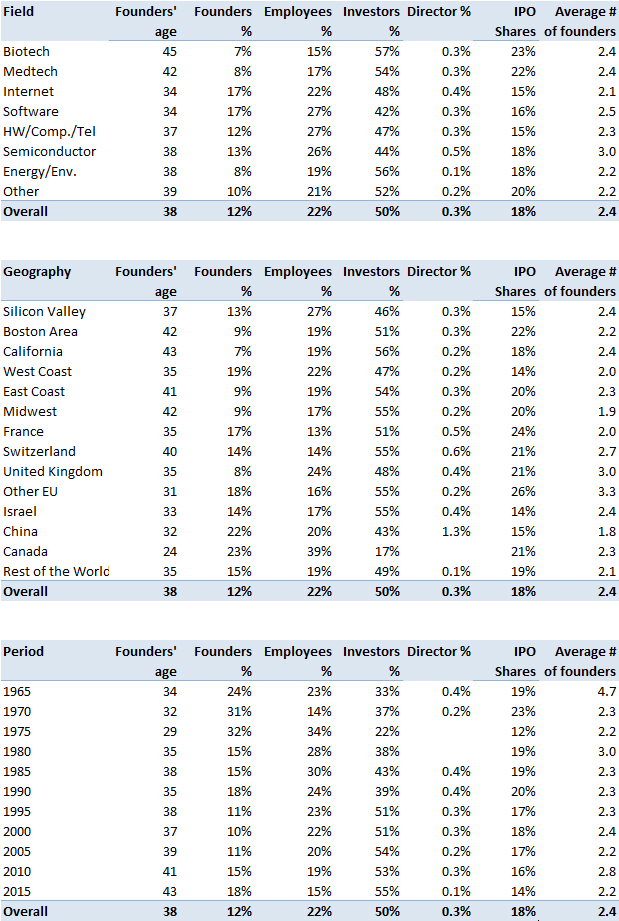

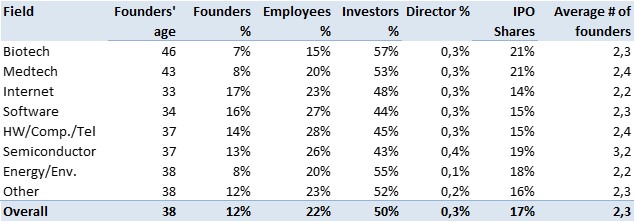

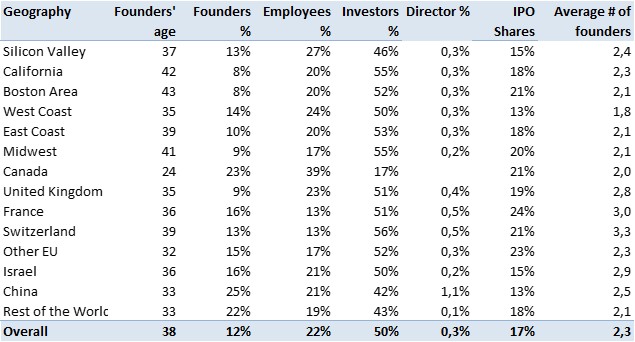

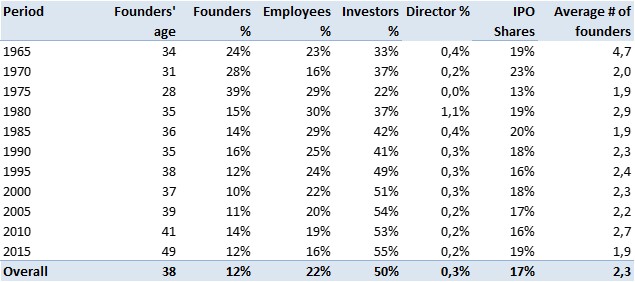

Data about founders (age, ownership and nb. by startups) and other stakeholders by fields, geographies and periods of time.

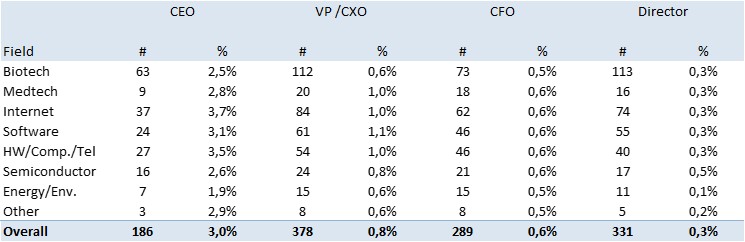

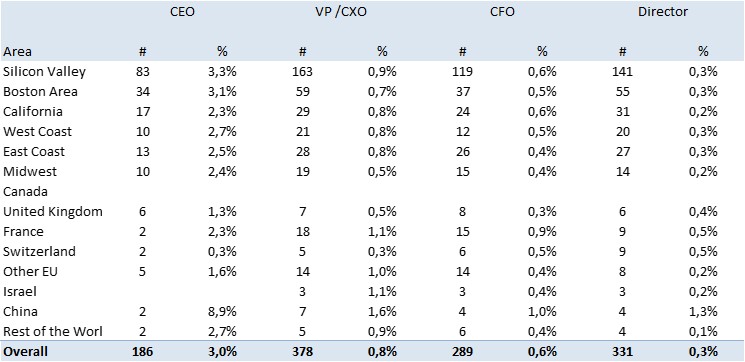

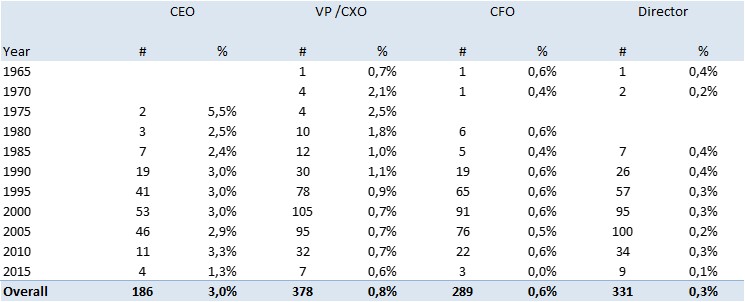

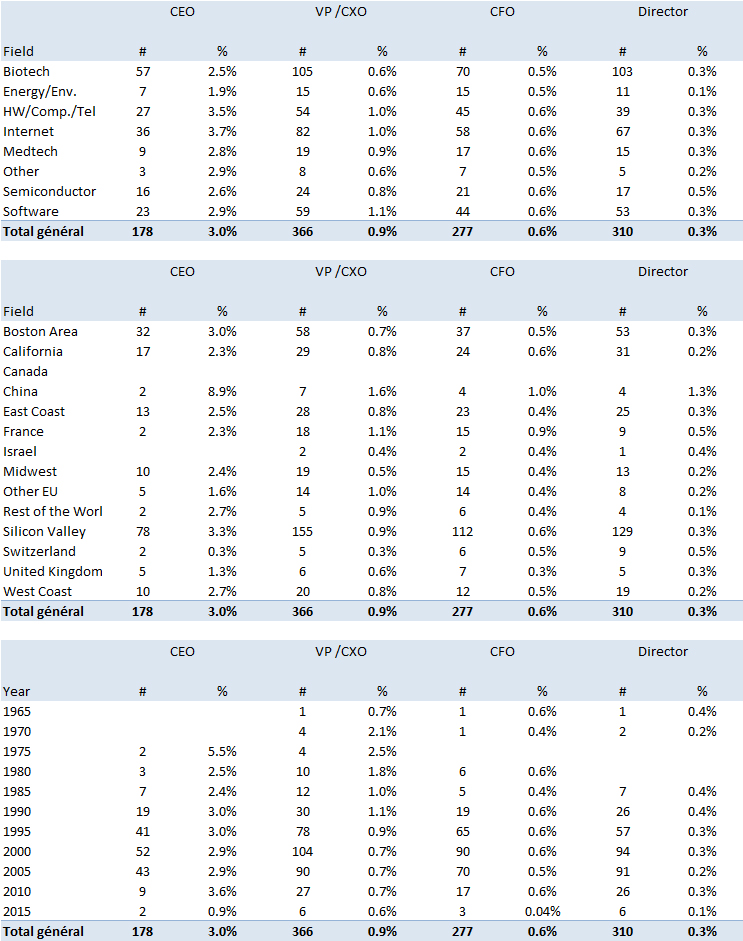

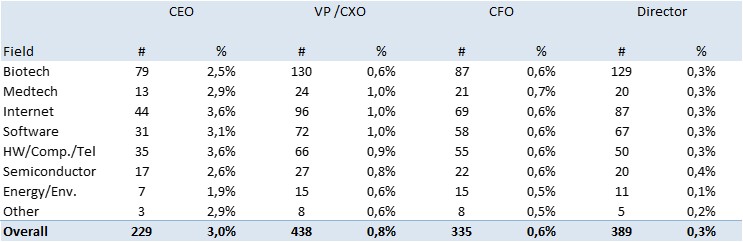

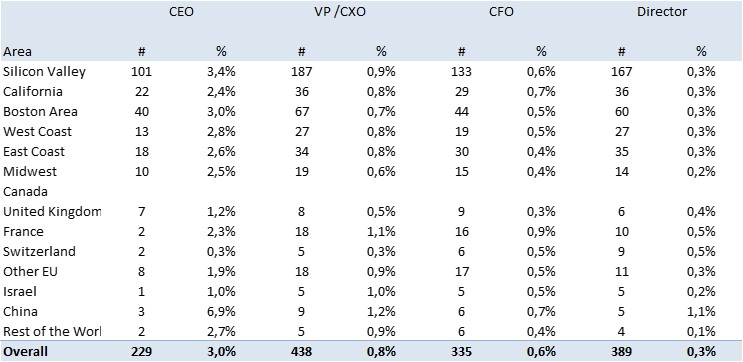

Data about ownership of non-founding CEOs, VPs, CXOs, board members by fields, geographies and periods of time.

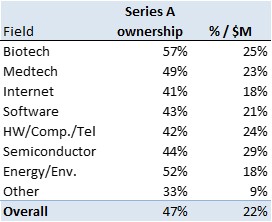

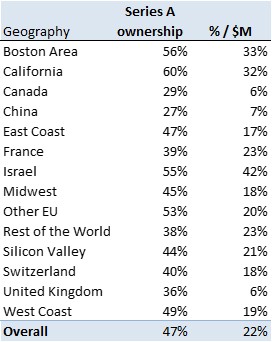

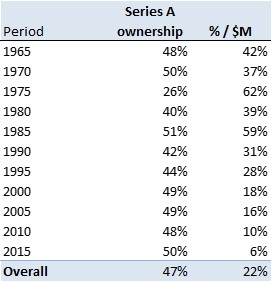

New data about ownership of series A investors by fields, geographies and periods of time.