Palo Alto: a History of California, Capitalism, and The World by Malcolm Harris is a remarkable work. Point !

Now there has been some debates about it as you can listen on NPR. It is a marxist analysis. But you cannot disagree with the claim of the Washington Post on the cover page : “Conviction and research burn through the pages and give coherence and urgency to a daunting subject”.

Usually, I cut my post in many when they were so long, but I make a big exception probably because I could not stop reading the book and could not stop adding here in a linear manner.

The beginnings – The XIXth century

Harris begins with beginnings. Early settlers, the Gold rush, but also agriculture and the early Chinese population. He introduces us to famous and less famous figures such as John Sutter, Amadeo Giannini or Leland Stanford. The story-telling is smooth and scholar at the same time. But that is not the point. Let me quote him.

The point of the story is not that […] was a bad man because he profited from [stolen…] The point is that the series of plagues visited upon California in the second half of the nineteenth century took the form of men, and we can see the character of the tendencies that shaped the state (and in turn, the world) reflected in the men seized by them. […] The state […] called out for discipline, for an ambitious outsider unbeholden to the finance elite to whip everyone into rational shape.

The impersonal force that animates this state, this country is capitalism. That’s the name we’ve given to the particular system of domination and production in which landowners, on their own behalf, proletarize the working class into being. It is a predictable system with consistent lawlike tendencies. As Karl Marx suspected at the time, California has a privileged place in that story.

What interests me is not so much the personal qualities of the men and women in this history but how capitalism has made use of them. To think that way is not to surrender to predetermination; only by understanding how we’ve made use of can we start to distinguish our selves from our situations. How can you know what you want or feel or think – who you are – if you don’t know which way history’s marionette strings are tugging ? […] Maybe we’re more like butterflies, pinned live and wriggling onto history’s collage. […] I began this project with the fact that the railroad that brought the mass of capitalist white settlers to California is the same railroad my classmates used to kill themselves. The man who built that railroad called himself Leland Stanford. [Pages 36—37]

This reminds me both of A People’s History of the United States by Howard Zinn and There will be blood by Paul Thomas Anderson.

I knew a little about Leland Stanford, who became rich with the railroad.

“The Driving of the Last Spike” painted by Thomas Hill – The painting depicts the ceremony of the driving of the “Last Spike” at Promontory Summit, UT, on May 10, 1869, joining the rails of the Central Pacific Railroad and the Union Pacific Railroad. It is worth noting that some of the people depicted in the painting were not at the Gold Spike ceremony (e.g., Collis P. Huntington, Charles Crocker, Edwin B. Crocker, Theodore Judah and Mark Hopkins). Only two of the members of the Central Pacific board of directors were present: Leland Stanford and Charles Marsh (who are depicted in the painting).

I did not know he fled San Francisco to buy a farm where he grew race horses.

Palo Alto Spring by Thomas Hill The Stanford family, relatives and friends gathered on the lawns of their Palo Alto farm, which became the Stanford University campus. Jane Stanford, dressed in white, is shown on the far left. Leland Stanford holds a painting on his lap and rests his hand on the chair of his son, Leland Stanford, Jr. The artist, Thomas E. Hill, portrayed himself looking over his patron’s shoulder. The painting originally hung in the ballroom of the Stanford’s San Francisco mansion, which was destroyed in the 1906 earthquake.

I did not know Leland Stanford was at the origin of the first moving pictures by Eadweard Muybridge

I did not know that this became both Stanford University and Palo Alto and that the tree after which the city is named is or was still around recently.

The XXth century until Second World War

There were things I knew and others I did not.

I did not know Jane Stanford was probably poisoned, and probably the responsible was David Starr Jordan, president of Stanford University. Once Jordan had full power, Stanford focused on bionomics, with people such as Lewis Terman. The Stanford-Binet IQ would be developed to select future geniuses in the student classes. However William Shockley would not be selected even if he would be awarded the Nobel Prize for the invention of the transistor in 1947. [As a side note, Shockley was also a pionneer of Operation Research and possibly creator of the man.month concept. A strange and somehow cynical count of return on investment, about the impact of bombs through a ratio of casualties on both sides…]

Silicon Valley did not exist yet, but the first technology companies were founded during that period, with Stanford alumni sometimes:

– Federal Telegraph Company (FTC) founded in 1909 by Cyril Elwell (class of ’07).

– Russell and Sigurd Varian invented the Klystron in 1937 and founded Varian Associates in 1948. Russel was class of ’27 but not accepted for a PhD.

– Charles Litton (class of ’24) worked at FTC on the vacuum tube. He founded Litton Engineering Laboratories in 1931.

– Bill Hewlett and David Packard (both class of ’34) established Hewlett-Packard in 1939.

Much lesser known are political activists, for example:

– Kōtoku Shūsui founded the Social Revolutionary Party amongst Japanese-American immigrants, with links to the The Industrial Workers of the World (IWW), whose members are nicknamed “Wobblies”.

– Lala Har Dayal met Jordan in 1911 but would not stay at Stanford and created the International-Radical-Communist Anarchist Club by “weaving together atheism, Buddhism and Marxism” as well as the Bakunin Institute of California.

From left to right

Top line: Jane Stanford, David Starr Jordan, Lewis Terman, Cyril Elwell, Russell and Sigurd Varian.

Bottom line: Charles Litton, Bill Hewlett, David Packard, Kōtoku Shūsui, Lala Har Dayal.

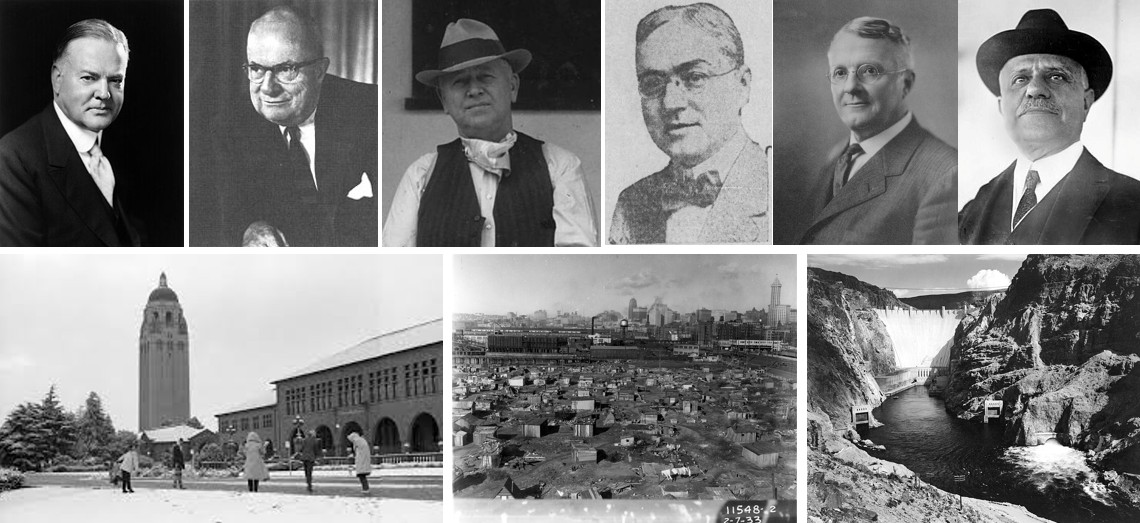

The Chief

Herbert Hoover, aka “The Chief”, is another important personality of that History. I remember the Hoover Tower on Stanford campus, I had not always made the link to Hoover Dam but certainly to the Hoover Institution which I linked to the Republican Reagan/Bush period.

I was neither aware of his links to mining, agriculture and aeronautics. This is also the 1929 crisis followed by FDR’s New Deal. Capitalism against Communism. Agriculture implied modernization, engineering with the Hoover Dam and firms like Bechtel or Kaiser. In parallel, it was the development of Aeronautics with new programs at MIT, Stanford and Caltech. Hoover helped a few friends thanks to the Air Commerce Act : “The government facilitated leading men, who in turn facilitated the government’s facilitation. It wasn’t corruption that enabled Herbert Hoover, it was coordination, the way royal families arrange marriages.”

From left to right

Top line: Herbert Hoover, Henry Kaiser, Warren Bechtel, Henry Robinson, Harry Chandler, Daniel Guggenheim

Bottom line: Hoover Institution & Tower, Hooverville, Hoover Dam

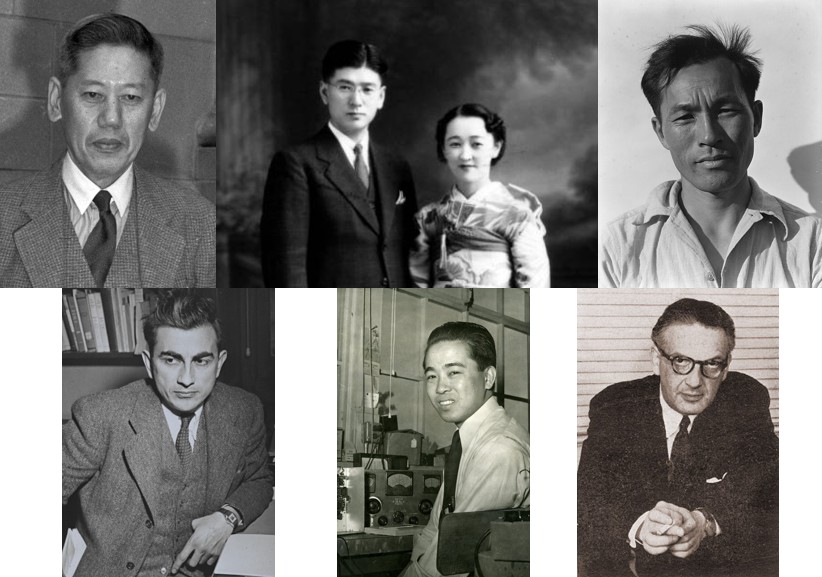

The California Japanese

I did not know about the strange perception of race and gender in California : aristocratic, racist but in a weird way. Japan was superior, the “whites of Asia”. Stanford had women, Indian and Japanese graduates…

– Yamato Ishihashi, after a PhD at Harvard got the first Stanford endowed chair (by Japanese firms) in 1922.

– Noboru Shirai, one of the 22 Stanford’s Japanese students and only one of the 4 first generation immigrant, had opposite positions against the imperialist and criminal behaviors of his native countries.

Both would be interned in camps during 2nd World War though…

– Shuji Matsui, a left-wing progressive, would suffer beatings at Camp Tulelake

– Karl Yoneda would support strikes and be seen under “STOP THE JAPANESE AGGRESSION” banners.

“While David Starr Jordan was off shaking hands with the emperor and categorizing fish, American police were rounding up Japanese leftists and shippig them back as undesirable aliens to face imperial justice.” [Page 205]

From left to right:

Top line: Yamato Ishihashi, Akiko and Noboru Shirai, Karl Yoneda.

Bottom line: Ernesto Galarza, Art Fong, Paul Baran.

A home front

Immigrants were not the only source of political fights as mentioned above but it was a strong element :

– Enersto Galarza (class of ’29) could have become an academic and decided to work all his life for better living conditions of working-class Latinos.

– Art Fong could not have housing in the while-only sector of Palo Alto despite having been hired by Bill Hewlett in 1946. “In my long career in Silicon Valley, I had always hoped that it would be my skill in science and computers that drew attention, not my race. And yet, I was often reminded of my Asian heritage. It’s a very strange thing, because in those early years, Asians seemed to have a difficult time everyplace. Other minorities like Jews, African-Americans, and Hispanics had similar problems. When we came to Palo Alto in 1946, we couldn’t find a place to live because all of Palo Alto had restrictive covenants written in the land deeds, for Caucasians only. It was illegal for me – a Chinese American – to buy or rent a house in the desirable parts of Palo Alto. But I was determined that wouldn’t stop me from trying. About that time in the post-war politics, local and national anti-discrimination activities were brewing. Soon there was US law passed which legally removed those covenants on the land deeds, all at once.” (quoted from here)

– Paul Baran, Russian-born and Stanford professor since 1949, would become the only tenured Marxist teaching economics in the USA.

After Word War II

During the post-war boom, Palo Alto developed thanks to military contracts. High-rise buildings were forbidden, zoning was carefully done, Santa Clara fruit-growing acres went down from 101’666 in 1940 to 25’511 in 1973. Thanks to the old public-private practice created since the XIXth century, “East Palo Alto went from white to 82% black within six years. When liberals suggested a north-south dividing to produce integrated schools, reactionaries created a high school right in the middle of East Palo Alto in 1958, which segregated the teenagers for the first time in a manner that endures to the present with few exceptions.” [Page 231-2]

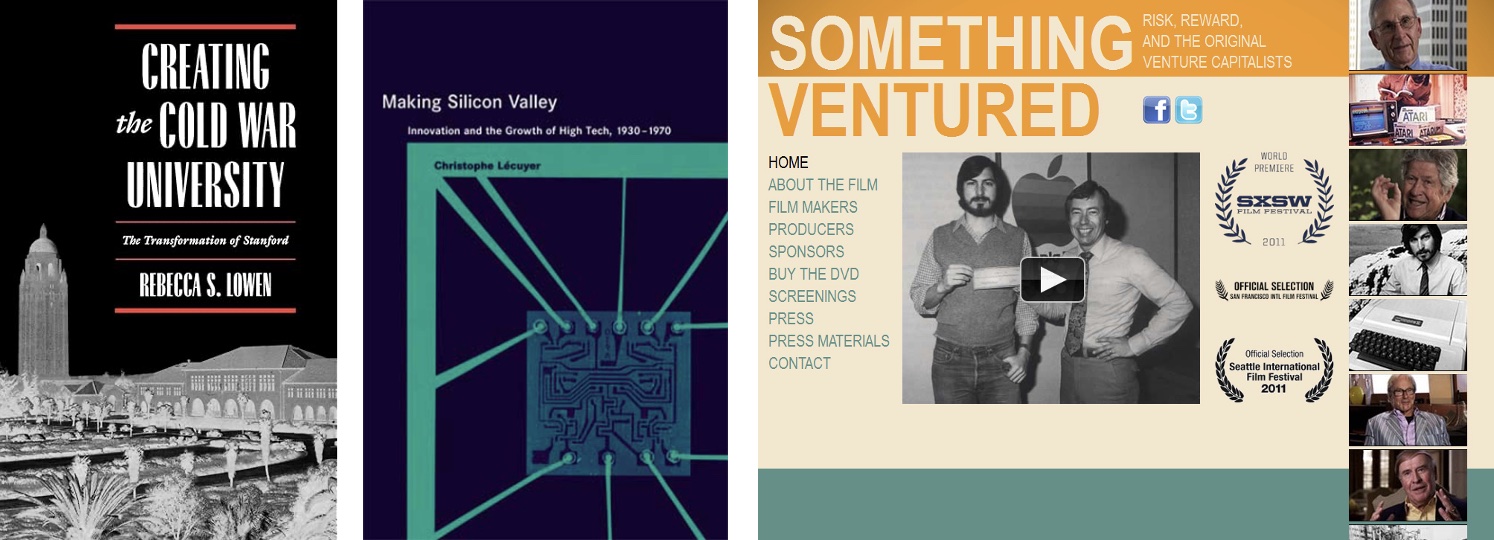

I am finally entering known territories. Malcolm Harris quotes Rebecca Lowen and Christophe Lecuyer to describe the impact of the transistor in the region. Fairchild, Intel, Arthur Rock.

And Malcolm Harris does not forget to add that the industry required a lot of low-cost workers. A tentative for a $1M machine was abandoned when workers could do the work three times faster. Fairchild would be the first to offshore with production in Hong Kong in the early 1960s (assembly work was 10 cents there vs $2.5/hour in the Bay Area and a transistor cost was 3 cents in material and 10 cents in labour.)

The Beat

“Surrounded by so much historical unfairness and noble defeat, how did white suburban winners in Palo Alto come to convince themselves and a surprising segment of the world that they were the real loser rebels?” [Page 294] This is probably the most moving chapter of the book. Again this was totally unknown to me. Artists which career never boomed. What would be the United States with a different outcome ? This reminds me of the concept of Lost Einsteins.

From left to right: Bob Kaufman, Joe Overstreet, Toy and Wing, Ruth_Asawa.

The book is worth reading for this chapter alone. Here is a poem by Bob Kaufman:

Aliens winds sweeping the highway

fling the dust of medicine men,

long dead,

in the california afternoon

Into the floating eyes

of spitting gadget salesmen,

eating murdered hot dogs,

in the california afternoon

And here is an excerpt from Alan Ginsberg [not easy for me and a bit out of context but which I wish to keep for my own archive]: Emerging up from 3rd class to First on great oceanliner – up the staircase to the deck – First thing I meet, huge faded negro Paul Robeson – in officer’s uniform – I salute him introducing myself which doesn’t mean much to him – he bows – I begin scheming immediately – Being a big officer Communist negro all these years perhaps he could get me a book in the NMU so I can ship out? I see he’s working on an open deck hole with a lift truck & wire lift placing 2nd hand turkish rugs in the hold – Old communist, I notice I am amazed at his calm – he is folding the dead in to carry that way – (Won’t they not smell up the exported carpets?) – I see one corpse in the hold lying face up on rug, he’s getting a layer of carpet to cover that. The corpse is a middle-aged man dead-faced & slightly rotten lying on a rug drest in a blue business suit. I wonder if I have the guts to face corpses like that negro communist. [Journals : Early Fifties, Early Sixties (Grove/Atlantic 2007) p177-78]

I had never thought that segregation was as high in California as it was in the South. But it was. Malcolm Harris illustrates it with many stories and I am unfair not to mention it much further. He also mentions a parallel fact about education that I found interesting : “So far I’ve focused on the state’s elite higher-education institutions [Stanford and UC Berkeley] but a number of historians give the California community college system at least as much credit for the region’s exceptional success in developing its various tech industries. . […] By the end of the 1920s, the state had 15’000 students across 34 junior colleges, more than one-third of the country’s junior college students among less than 5 percent of the U.S. population.” And this continued decade after decade. “The two-year schools switched their focus to vocational preparation, which critics alledged was designed to keep working-class youths away from professional paths, while defenders said it upheld the state tradition of the upwardly mobile technician.” [Pages 324-5]

Shoot (the computers)

There is so much violence in the history of the United States and of California in particular. More soon. Harris, again, is convincing thanks to the precision and high quantity of facts he shares with us. It is just a terrible history. Even worse: “it’s tempting to silo, say, the missile surburbs, microchip invention, the personal computer, and the political ’60s. But these developments weren’t just connected, they were the same thing.” [Page 334]

If the 60s were politically violent, the Kennedys, Martin Luther King, Malcolm X and his Ballot vs. Bullet speech, it did not stop there and went on until the mid seventies at least. If all of a sudden, it reminds me of American Pastoral by Philip Roth or more recent One Battle After Another, itself with links to Vineland by Thomas Pynchon, what should I say of Chapter 3.4, How to destroy an Empire. No doubt I did not know much about American revolutionary movements who were very close to physical violence. To protest against the war in Vietnam, the house of Bill Hewlett was firebombed. In December of 1971, militants bombed the Stanford Linear Accelerator Center.

There are again unknown figures to me. Stanford Professor H Bruce Franklin who moved from studying Hawthorne and Melville (“his thesis was based on a close reading of Moby Dick and Melville’s polyphonic use of mythology” [Page 336]) to Marx and Melville. He would not survive that long as a professor and [Lyman, then Stanford president] “suspended Franklin, obtained a court injunction banning him from Campus, and started the permanent removal process.” There are many more stories in particular in the April 3 movement web site, about Franklin or Aaron Manganiello, founder of Vencemeros. And what about these documents about SRI, Smash War Research (pdf) or even threats against David Packard (in pdf again) (who had become United States Deputy Secretary of Defense under Nixon even if for not long). In 1969, Angela Davis had been fired from UCLA.

“The dramatic dead end of the Bay Area armed struggle was a May 1974 shootout in Los Angeles. This was not the world Shockley’s equations promised. Battered first in Vietnam by the Vietnamese people and second on the home front by the Third World solidarity movement, America’s leadership came to grips with the unthinkable: losing the war. […] Partial defeat in the Cold War’s first half catalyzed a conservative revitalization as America’s ruling class came to understand the stakes. They abandoned the compensatory state and its equalizing mission to focus on individual rights. […] Tuition fees at the University of California system doubled in the ’80s then tripled in the ’90s.” [Page 357]

Another example is Cedric Robinson who “criticized his discipline’s concept of leadership and offered counterexamples of African “stateless societies” or “tribes without rulers” – particularly the anarchistic Tonga – the political science department lost its integrationist nerve. Faculty members declined to sit on his committee, passive-agressively consigning Robinson to academic purgatory.” [Page 358]

In 1975, after a series of layoffs at Fairchild, led in part by former assembly line worker Roxanne Dunbar, activists arrived to “find police snipers lining the roof of the plant building and tactical squads swarming the place in riot gear”. [Page 359]

Allard Lowenstein, a close advisor to Bobby Kennedy, spent his life trying to cool down the hard-liners and bring them into the left wing of liberalism. Dennis Sweeney, a likable Stanford student with a harsh family life (who according to others seemed to be like the first person back from Dachau) went to Lowenstein’s office in Manhattan in the spring of 1980 and shot him to death (because, mentally ill, he believed that Lowenstein was plotting against him.) Even if it was a tragic waste, there would be an unsigned editorial “No tears for Allard Lowenstein”.

From left to right: H Bruce Franklin, Venceremos, with Aaron Manganiello pictured on the right, Cedric Robinson, Roxanne Dunbar, Allard K. Lowenstein.

“With the growing unrest in the country, the increasing sophistication of saboteurs and the potential that computers offer for easily inflicted and costly damage, major precautions are necessary for data processing managers to fully protect their computers.” [Page 358]

“If the 60s and early 70s had been Power to the People, they were followed by the re-empowerment of owners relative to workers after the uprisings at home and abroad via unemployment and de-industrialization immigration, offshoring, and all manner of technological and organizational changes.” [Page 364]

Individualistic conservatism

Malcolm Harris enters a new subject with that new period : individualistic conservatism. “Immigration and offshoring were the two sides of the same coin.” He mentions again the cost of fabrication at home and assembly offshored. Even worse Shockley would become the hero of the pseudoscience of racial difference. The Vietnam war would have unpredictable consequences : “By 1984, Hewlett-Packard employed 4,000 Vietnamese immigrant workers in low-level jobs. These workers tended to be skilled, politically conservative and desperate. It’s not a coincidence that the South Bay maintains the country’s largest concentration of Vietnamese immigrants to this day. Silicon Valley firms were ready to absorb thousands of refugee workers at the same time and for the same reason they were refugees in the first place”. [Page 365] “It seems counterintuitive to pay some workers not to pay other workers, but by using stock options and grants to align professional employees’ interest with ownerhsip, firms could provide a paternalistic atmosphere for high-value engineers while keeping the aggregate wage low enough to generate double-digit profits even as prices fell. The labor-hostile surburb kept its production wages low by locking organized labor out of its factories.” [Page 366]

In 1994, AnnaLee Saxenian described the results of the previous couple of decades: “There are approximately 200,000 union members in the four-county [Bay Area] region, but virtually none work in high technology industries. No high technology firm has been organized by a labor union in Silicon Valley during the past twenty years, and there have been fewer than a dozen serious attempts.” It was a brutal period for workers and a correpondingly excellent one for the men who employed them. [Page 368]

White working-class homeowners began to identify as white and homeowners more than as members of the working class, and not without reasons. If their human capital was depreciating rapidly, their home values jumped. […] With home ownership also came guaranteed places in the California public school system, where the professionaals workers of the future were trained. […] The California dream was always about land speculation premised on racial exclusion and domination. [Pages 378-9] Education improved for the rich and got worse for the poor. [Pages 382]

Tax breaks the same… Reagan was soon to become president, and behind him the Hoover institution. Individualism, privacy, property, competition thanks to deregulation, privatization and tax cuts that reinforced each other. Workers benefited from pension funds but the unions didn’t generally manage their voting shares… [Page 406-7]

The huge capital-gains tax cut – more than 50 percent – and pension-investment deregulation helped turn venture capital from something small groups of well-connected buddies did in Cambridge. Capital in the funds quadrupled in the early 1980s, from $1 billion at the close of the 1970s to $4 billion in 1983. [Page 408]

Malcolm Harris again surprised me when I thought I was in known territory. On pages 408 and next, he begins with the Tragedy of the commons to explain the privatization of public goods. “This represented a change in the ideology, from recognizing the need to build up an intellectual property commons for new industries to creating the best investment climate possible by constraining the spread of new tech. Whereas lively antitrust enforcement ensured the proliferation of the first transistor licenses, the new state religion encouraged techno-monopolism on the public dime.” The Genentech story is well-known and I am a little surprised though with the argument here. I had the feeling the DNA patent was non-exclusive as the transistor one. I might be wrong but it seems to be mentioned here. I did not know either that Donald Kennedy, president of Stanford, had to resign in 1991 for the school’s alleged abuses of federal research funds.

New World Order

The Reagan era – which includes Carter’s presidency as well as George Bush Sr. and arguably, Clinton, George Bush Jr., Obama, Trump and Biden, at the time of this writing, put America back on its narrative track. The country’s time in the sun wasn’t over. […] Innovation was the new watchword, high-tech the new American brand. But what made this strategy more successful in this period than it was in the preceding years? Computerization didn’t add enough efficiency to the country’s manufacturing processes to make them competitive. […] The rapid Soviet acsent in science and technology proved there wasn’t anything special or inherently faster about the capitalist development road. […] The military Keynesian strategy succeeded in keeping a border with the reds – Japan, Taiwan, South Korea, and West Germany remained a solid buffer against failing dominoes. [So ? … but] As capital concentrated in fewer hands, it grew easier to get everyone on this same pager, a pager later named the Washington Consensus. Harris adds a few other points such as immigration both from this buffer countries as well as “by the end of the 70s, 99.7 percent of the more than one million people admitted under parole were from communist countries”. Harris also mentions corrupt regimes such as Iran or the Philippines which induced a lot of not to say hugh financial flows including the ones that would finance counterrevolutions all over the world. The section about Stanford Technology Corporation [pages 428-38] is particularly enlighting.

The anecdotal part about Steve Jobs and Trey (Bill) Gates is very well-known territory but again Harris’ analysis is original. “The true path of invention is rarely clean or simple, but when scientific credit fails to align with net worth, the second trumps the first in public memory. After all crediting inventors is notoriously difficult; every innovation building on the last, every inventor inextricably embedded in a series of communities. Two or more often alight on the same idea at the same time. Money provides a sort of scoreboard, an equivalent by which we can compare the otherwise incomparable.” Harris reminds us that “it’s the connectors who are more responsible than the inventors or even the specific siloed visionaries. […] More sophisticated than the Great Man version, this ecosystem analysis still takes its object for granted. The Great Region histories, like AnnaLee Saxenian’s *Regional Advantage* and John Markoff’s *What the Dormouse Said*, see Silicon Valley as a place of creation rather than transformation. By placing these stories in the context of statewide, national and global changes, we can better understand the microcomputer industry. Steve Jobs and Bill Gates are very important characters in the story, but they’re more meaningful as personifications of impersonal social forces. If Jobs and Gates hadn’t been themselves, some other guys would have been instead.” [Pages 453-54]

“There was an important difference between Gates and the hobbyist community: Trey Gates didn’t learn to code on a public system, not mostly. Gates got his computer training via an exclusive private school contracting with a private company that was financed by private capital. Trey Gates was an avatar of suburban bifurcation. […] The giants of Silicon Valley’s pre-silicon days tended to be handsome, athletic, and likable. […] Bil Gates and Steve Jobs, by contrast, had poor personal hygiene, didn’t play sports, and were both noted jerks. Neither served in the military, and both dropped out of college quickly. They ended up with two different corporate strategies, and occasionally became business opponents, but they personified the same historical forces. […] This has been described as the transition from “bureaucratic” to “nerd” masculinity. […] Any laborers a company couldn’t easily replace were aligned with ownership via stock option.” [Pages 455-59]

Then computers needed to be connected. This is the story of Bob Metcalfe and 3com, of Arpanet and wireless ALOHAnet, of ethernet and TCP/IP, of the router with William Yeager, Andy Bechtolsheim, Leonard Bosack and Sandy lerner, the last two being the founders of cisco Systems (which story of its neginnigns would be worse reminding [pages 463-4 or here at www.tcracs.org/tcrwp/1origin-of-cisco].

The Internet will soon follow and again even if the history is well documented, Harris provides an interesting point of view. America was pro-business and even if some presidents were Democrats, the Hoover institution distilled its ideology not just during the Reagan or Bush presidencies. I am not sure what Harris says of its influence over Trump. He provides interesting (Marxist) views on geopolitics and economics: “over half – up to 80 percent – of the country’s employment growth between 1984 and 1997 came in the form of externally contracted workers. And those were the jobs kept onshore; statewide, electric and electronic manufacturing employment fell 38.7 percent between 1980 and 1995. […] Capitalists were winning because their workers were losing, a reality well camouflaged by the whiz-bang excitement Silicon Valley produced.” [Page 474]. “America imported a bifurcated cohort of immigrants to fit a bifurcating pattern of employment, and for every Silicon Valley investor or board member or founder from the Third World, there was a family of refugees in a local basement performing the low-wage manufacturing labor that animated the computer industry’s numbers. Neocolonialism provided more than a market for Silicon Valley’s defense-ish electronics: it provided a labor force as well” [Page 475].

The 21st Century

His analysis of the parallel development of the coffee and cocaine markets is equally striking [Pages 479-484]. The Internet has disrupted many other markets. One need only note the stories of Netscape and the antitrust lawsuit against Microsoft [pages 485-90], recall Alan Greenspan’s famous “irrational exuberance” [page 488], the deadly competition between Healtheon and WebMD, between Pets.com and Petopia, between WebVan and Homegrocer, between Ticketmaster and tickets.com, between Rio, Naptser, Winamp and Realplayer. Republicans didn’t like Clinton, but their policies weren’t so different.

And again “Google could afford to contract low-wage workers to drive cameras around and to turn pages. . […] In the grand NorCal tradition of labor-market segregation, these laborers carried unique yellow badges, though that was hardly necessary to mark them, “it was the same group of workers, mostly black and Latino, on a campus of mostly white and Asian employees, walking our of the exit like a factory bell had just gone off”. They entered and exited at their own special scheduled times – 4:00am and 2:15pm – so as to spare the white-(employee), green-(intern) and red-(contractor) badged Googlers an awkward confrontation with that particular internal hierarchy” [Page 515 – you can also a longer description of Google from where this excerpt is coming from in The Artist Leaving the Googleplex by Andrew Norman Wilson]. Malcolm Harris emphasizes the harsh, not to say sometimes inhumane, working conditions (as seems to be the case in Amazon warehouses). The fact that this was also the case for Apple, or is the case for Google in the United States, is somewhat surprising, given the emphasis placed on an original and appealing approach to engineers’ working conditions. A significant discrepancy indeed.

Of course this globalization decentered the world towards Asia and China in particular. Foxconn would be its most visible illustration and not really for good. Suicides would happen there and Harris quotes a chinese poet and Foxconn employee, Xu Lizhi, who would commit suicide later [Page 540]. So I quote him too:

Xu Lizhi, Chinese poet (1990-2014)

“I Fall Asleep, Just Standing Like That” from libcom.com

拒绝旷工,拒绝病假,拒绝事假

Refuse to skip work, refuse sick leave, refuse leave for private reasons

拒绝迟到,拒绝早退

Refuse to be late, refuse to leave early

流水线旁我站立如铁,双手如飞

By the assembly line I stood straight like iron, hands like flight,

多少白天,多少黑夜

How many days, how many nights

我就那样,站着入睡

Did I – just like that – standing fall asleep?

“A Screw Fell to the Ground” again from libcom.com

一颗螺丝掉在地上

A screw fell to the ground

在这个加班的夜晚

In this dark night of overtime

垂直降落,轻轻一响

Plunging vertically, lightly clinking

不会引起任何人的注意

It won’t attract anyone’s attention

就像在此之前

Just like last time

某个相同的夜晚

On a night like this

有个人掉在地上

When someone plunged to the ground

Bifurcations

Continental divide, digital divide, educational divide. One may not view the world the way Malcolm Harris does. Politics seem to be closer and closer to religious faith. People do not look at facts to see some truth. What a strange world. But it is worth reading Palo Alto until the end. The high school created in East Palo Alto has finally been closed and replaced by a shopping mall with low wages employees. The mall “inaugural plaque acknowledges Bank of America and the David and Lucile Packard Foundation. At the very bottom: ORIGINAL SITE OF RAVENSWOOD HIGH SCHOOL.” [Page 551]

If China has mainly invested locally, Russia has a different fate with oligarchs investing their money abroad. But again Harris claims these are two faces of the same coin. Yuri Milner and Alisher Usmanov invested big time in Silicon Valley through Digital Sky Technologies (DST): $200m for 2% in Facebook and more later to reach 8-10% of the startup, $380M in Twitter, some in Groupon, Zynga and Spotify and something I did not know, were major investors in Paul Graham’s YCombinator. “If tech companies – along with expensive art and luxury housing – were a bet on further bifurcation and inequality, then they gave the world’s oligarch community a chance to double down on its own prosperity. And it works – for Russian billionaires, for American billionaires, for Taiwanese billionaires, and even for most mainland Chinese billionaires. The value chain links ex-Soviet extractionists like Usmanov – convicted of and imprisoned for “theft of socialist property” in the 80s – with Foxconn’s company towns and their mandatory overtime, corporate dorms, and loathsome security patrols.” [Page 548]

In 2009, 42 people were arrested in East Palo Alto (EPA), dismantling the Taliban drug dealing gang on Sacremento St, “a cul-de-sac off University Avenue. The struggle for drug territory drove EPA’s violence in the period, giving it the country’s highest per capita murder rate in 1992”. (This is not new, the interested reader could watch French Documenary the Last Town on Arte or read here The Capital Sins of Silicon Valley). In another bifurcation well described by Harris by mentioninig My Posse Don’t Do Homework by LouAnne Johnson as well as Unforgetting: A Memoir of Family, Migration, Gangs, and Revolution in the Americas by Roberto Lovato, the author describes the No Child Left Behind as a “soft bigotry of low expectations”, a brilliantly phrased subtle attack on affirmative action. Whether they [kids] would be in better classes in better schools a separate question. […] Capitalists needed low-wage employees because that’s where the growth was. If all the kids in East Palo Alto became engineeers and doctors and lawyers, who would fill the hundreds of jobs at the new IKEA by the freeway [Page 557-8].

At the other end, a few entrepreneurs would create new teaching tools such as SCORE! and the Education Program for Gifted Youth (an online school at $28,610 tuition). “The schools are good because the houses are expensive, which makes the houses more expensive and the schools better, which makes the houses more expensive and the schools better, which makes the houses more expensive and the schools better“. [Page 562] When the Stanford student startup Instagram sold for $1B to Facebook, it only had 13 employees. “Beneath the mounting valuations are a relatively small number of hyper-competitive employees. The super-coders are the most notorious, having cultivated a professional mystique, but the non-technical managers are just as important for rapid growth. The coders certainly don’t work as fast without them. Bolstered by armies of unseen contractors, Silicon Valley’s high-IQ workers, the veterans of SCORE! fulfilled Lewis Terman’s wilded dreams.” […] It’s not behaviorism, it’s neobehaviorism. To heighten productivity, the paradigm of disciplination is replaced by the paradigm of achievement. Stanford’s horses were the original achievement subjects and they were proned to burn out as well. Society produces “depressives and loosers” as its human exhaust. Even the killers are nerds. [Page 562-5] Palo Alto is becoming the place that produces Baby Einsteins, but one of these students says: “We are lifeless bodies in a system that breeds competition, hatred, and discourages teamwork and genuine learning. We lack sincere passion. We are sick… It is time to realize that we work our students to death” (See below the article by Carolyn Walworth). Following the many suicides in Palo Alto’s high schools, With no smoking gun in the report, local leaders could adopt the same line Steve Jobs used with regard to the Foxconn suicides: “It’s sad, but sometimes people kill themselves”. Still, in both these environments, there was only so far anyone could spread the blame. In January of 2010, a Foxconn worker jumped to his death the day after a teenager in Palo Alto died on the tracks. In January of 2011, it happened again. The second time they were both nineteen years old. [Page 567] “The beauty of the design is that the rewards call forth the winners, and the winners create losers. It’s impersonal: forces not men.” [Page 568]

Harris published his book in 2022, there was no ChatGPT yet, there was no Trump II yet, but Harris mentions the PayPal mafia, including Musk and Thiel who employed JD Vance and sponsored Curtis Jarvin. He also mentions Theranos, Snowden, the Google buses, Uber and Palantir. “Compared to the past cohorts of successful Silicon Valley tech founders, the crab platform leaders made Steve Jobs look like Steve Wozniak” [page 580]. “Capital’s ever-accumulating need for profitable sinks is incompatible with the kind of democratic control over modern technology that the Black Panther Party put on its program. […] It may be that Silicon Valley is best understood as a particular expression of this impersonal drive: geographic, historical and imaginary. It represents the gold rush and the next gold rush and the one after that, from produce to real estate to radios to transistors to microchips to missiles to PCs to routers to browsers to web portals to iPods to gig platforms to… If California is Americas’s America, then Palo Alto is Americas’s Americas’s America” [Page 616].

I am not sure if the reader will follow Harris in his conclusion, which reminds me of the end of Fahrenheit 451. Let me add a final extract : “If the intergalactic capitalists win, if they do exhaust the earth and humanity then for the sake of my historical reputation and that of everyone I’ve ever loved, I hope the post-humans judge that we were already too late, that we never had a chance. Maybe that is the case – as I’ve argued, the general state of things is increasingly dire for many people – but I don’t believe it. Even if I could be made to believe it, I would choose not to. I am committed to this planet, which means I have to hold on the possibility of an alternative to capitalist exhaustion” [Page 619]. These words, his words are also mine.

PS: I’m including here an excerpt from another book review by the excellent Olivier Alexandre, his “optimistic” conclusion to the current crisis: “In a highly competitive world, where nothing lasts, starting with tech companies (the tragic fate of Kodak, Nokia, BlackBerry, and Yahoo reminds us of this), this notion conveys the idea that a homogeneous category of actors has long since seized control of history, and will continue to do so for a long time. This overlooks, as the book reminds us, that this domination is entirely conditioned by the interplay of actors and a constantly evolving institutional framework. Moreover, the narrative is constantly being traversed, interrupted, pulled in one direction and then another by individuals and groups, companies, but also government agencies, hackers, whistleblowers, academics, and activists. Perhaps this is enough to offer a glimmer of hope to all those who feel trapped in the web.” It could have been a conclusion of Malcolm Harris book too!

PS2: I mentioned in the beginning an NPR account of the book. I found more critics worth mentioning :

The Children of California Shall Be Our Children: On Malcolm Harris’s “Palo Alto” by Ben Beitler, February 14, 2023 https://lareviewofbooks.org/article/the-children-of-california-shall-be-our-children-on-malcolm-harriss-palo-alto/

Greed, eugenics and giant gambles: author Malcolm Harris on the deadly toll of Silicon Valley capitalism by Lois Beckett, The Guardian, May, 11 2023

https://www.theguardian.com/books/2023/may/10/palo-alto-book-malcom-harris-interview

The Marvellous Boys of Palo Alto: From Silicon Valley Bank to Sam Bankman-Fried, the recent scandals upending the tech industry are rooted in a longer tradition of innovation and impunity by David Leavitt, The New Yorker March 20, 2023

https://www.newyorker.com/books/under-review/the-marvellous-boys-of-palo-alto

About the Silicon Valley Suicides

In Palo Alto’s High-Pressure Schools, Suicides Lead To Soul-Searching by Arun Rath, NPR, May 11, 2015

https://www.kqed.org/news/10521875/in-palo-altos-high-pressure-schools-suicides-lead-to-soul-searching

Why are so many kids with bright prospects killing themselves in Palo Alto? By Hanna Rosin, The Atlantic, December 2015 Issue

https://www.theatlantic.com/magazine/archive/2015/12/the-silicon-valley-suicides/413140/

Paly school board rep: ‘The sorrows of young Palo Altans’ by Carolyn Walworth, March 25, 2015

https://www.paloaltoonline.com/news/2015/03/25/guest-opinion-the-sorrows-of-young-palo-altans/

and a short text : The Price of Perfection: The Silicon Valley Suicides, Dec 16, 2015

https://thekimfoundation.org/the-price-of-perfection-the-silicon-valley-suicides/

The Atlantic published an article by Hanna Rosin entitled “The Silicon Valley Suicides: Why are so many kids with bright futures killing themselves in Palo Alto?” Rosin paints a picture of a place of affluence, success, and high expectations. However, at Gunn High School in Palo Alto, California, the 10 year suicide rate is four to five times the national average. By March of 2014, 42 Gunn students had already been hospitalized or treated for “significant suicidal ideation,” since the start of the school year. In a survey conducted in the same year, 12 percent of Palo Alto high-school students reported having seriously contemplated suicide in the past 12 months.

What is happening that is pushing kids to their breaking point? While we can’t pin point the exact reason why anyone ends their own life because of the complexity of suicide, there have been theories surrounding the high-pressure academic atmosphere that Palo Alto exudes.

Carolyn Walworth, a junior at Palo Alto High School and a school district student board member, wrote an article about her experiences as a student. She explains that as young as elementary school, children are either deemed “early” or “late” readers. While the “early” readers are labeled smart, the “late” readers are left feeling inadequate, and this constant cataloging follows them into high school.

“I like to think of this as the reason I lost my enthusiasm and confidence for math so early,” says Walworth. “How could I possibly feel intelligent when the class I was in was considered dumb?”

She describes the constant pressure to be in the advanced classes, participate in sports, school clubs, attend weekend SAT prep courses, obtain internships, and complete excessive amounts of homework, all while enduring the typical pressures of being a teenager. It is indeed exhausting and stressful. Walworth explains that this isn’t an issue of lack of coping skill, but merely an issue of too much to cope with.

In the late 1990’s, Suniya Luthar was an assistant professor in Yale’s psychiatry department. Luthar was doing research at a low-income, inner-city school in Connecticut. She wanted to find out whether misbehavior correlated more with poverty or with a stage of adolescents. Luthar needed a second school to use as a comparison and was connected with as upscale suburban school. What she found was shocking. The proportion of kids who smoked, drank, or used hard drugs was significantly higher in the suburban school, as was the rate of serious anxiety and depression. This anomaly started Luthar down a career-long track studying the vulnerabilities of students within what she calls “a culture of affluence.”

“We assume that because these kids have money and a good education, everything is fine,” Luthar says. “And in the long run, money and education will protect them, but in adolescence, the dangers posed by the culture of affluence can be quite potent.” However, that doesn’t mean kids who come from an affluent backgrounds are more likely to kill themselves. Studies on youth suicide have generally turned up few differences among social and economic classes. This finding simply means that there are a lot of youth from all walks of life suffering.

In the United States, there are about five youth suicide clusters a year and Palo Alto is well into its second. Whatever the reasons are, something must be done to change the culture of perfection among this community. Reaching out for help must begin to be viewed as strength, not as a weakness.

{kind=link}