Yesterday I published data in Tesla, Google and Facebook do not suffer from the crisis. and after linking my post to the usual Twitter, LinkedIn and Facebook, one of my readers (thanks Manuel!) told me it would be fun to add Uber as a comparison. I said I would if/when I find the time and then thought why not AirBnB, Apple, Amazon, Microsoft?

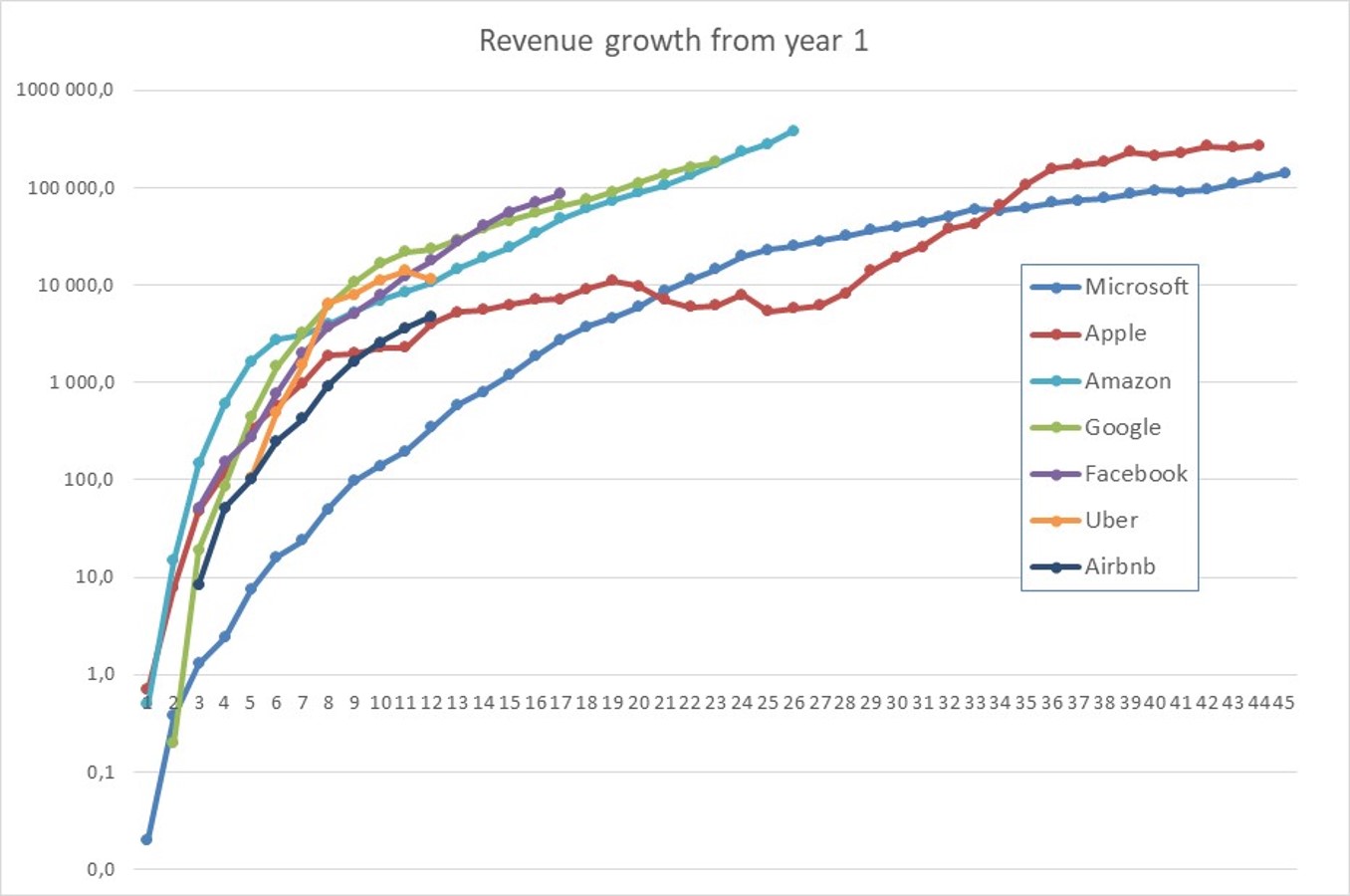

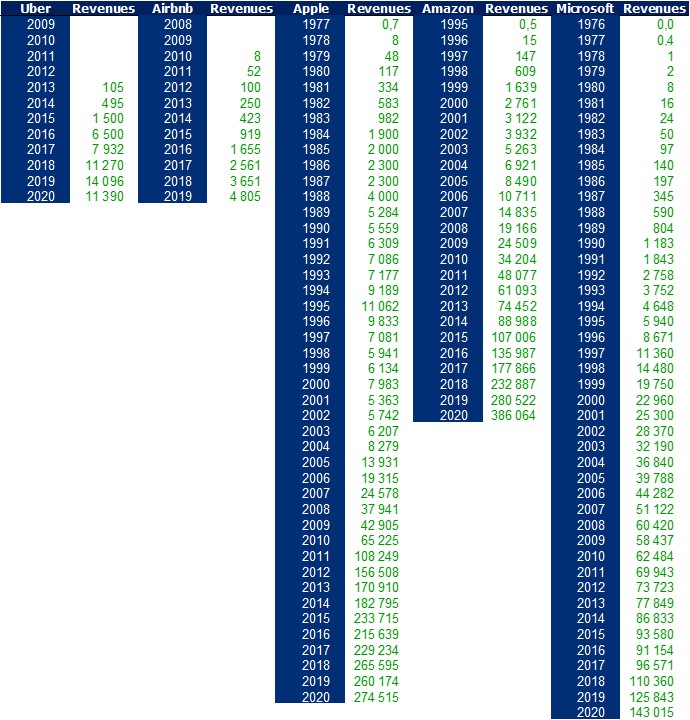

I could only compile data about revenues of these firms and I think it is striking enough:

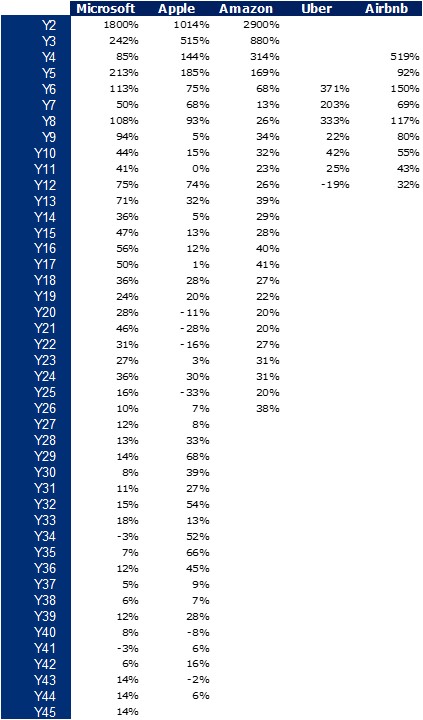

I wrote yerterday the growth rate was above 100% (doubling every year) in the early years declining to around 40% (doubling every other year) then to 15% (doubling evry five-year). Here are the growth rates of these old and new Titans. It begins again with 100+% for all of them. Too early to say about the future of Uber and AirBnB.

The three others of the GAFAM.

– Microsoft even had a 50% growth in its second decade, Amazon was closer to 30% and Apple struggled with 20%.

– In their 4th decade, Microsoft had an average grwoth of 10% and Apple 30%.

This may not be surprising and it has been said in the media. The GAFAs have generally benefited from the Covid crisis. So, as I was independantly doing in the recent years, I looked again at the growth of Google and Facebook as well as Tesla.

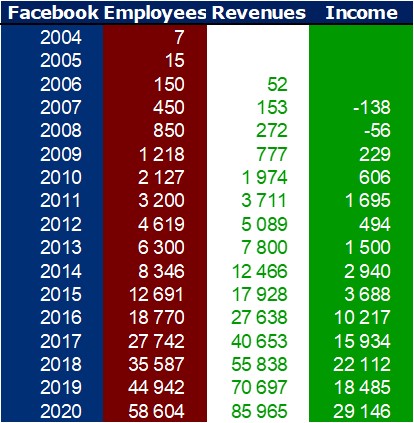

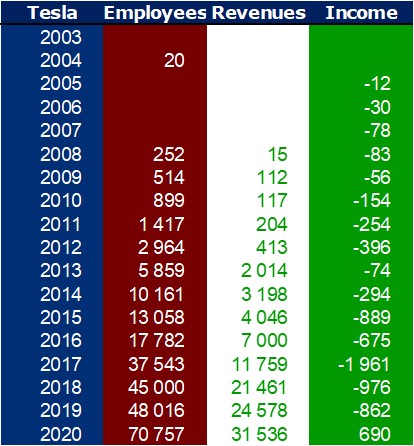

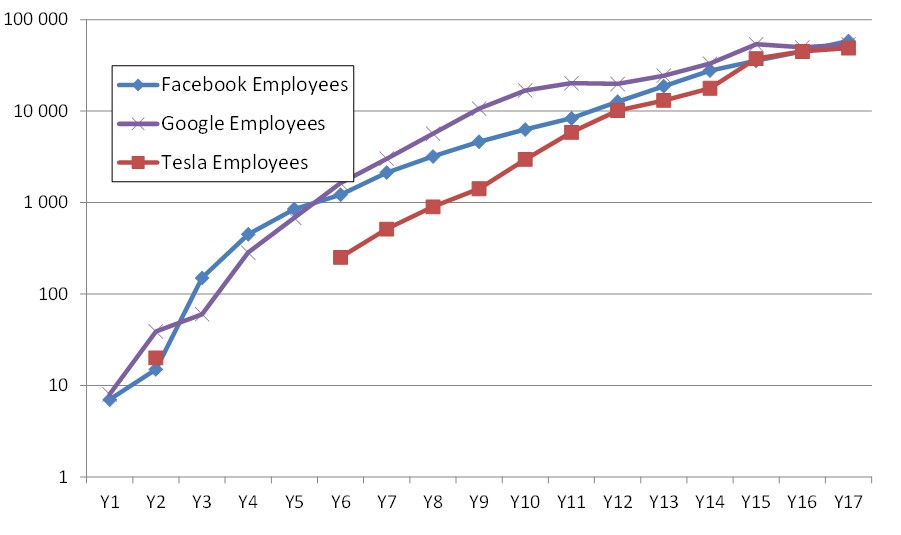

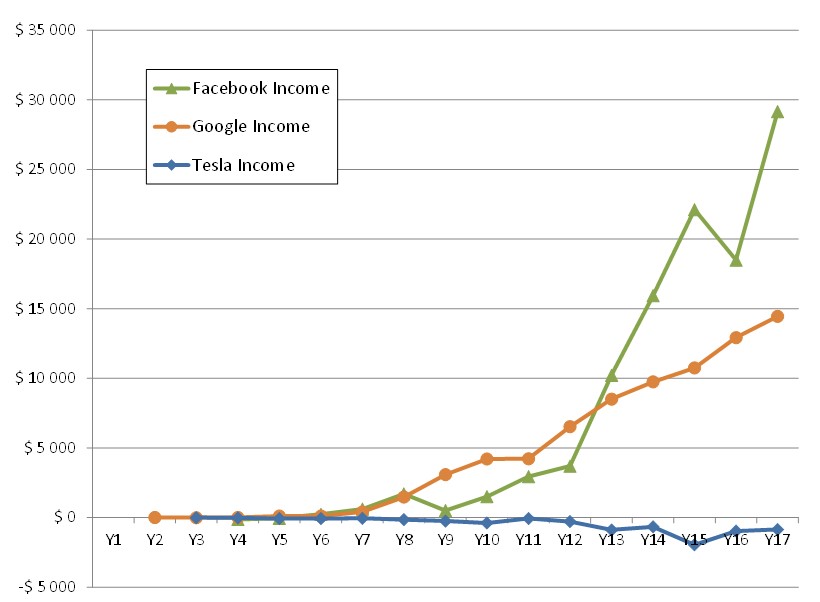

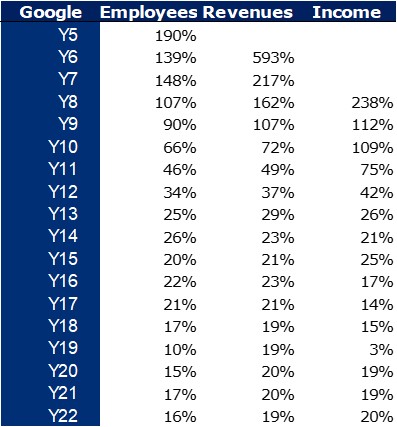

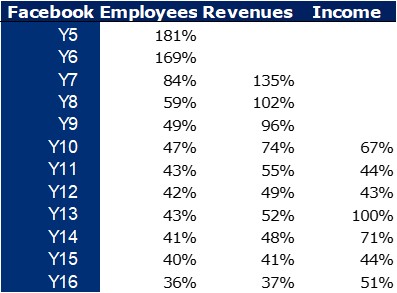

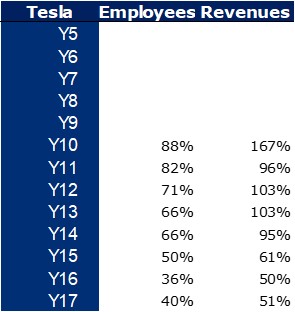

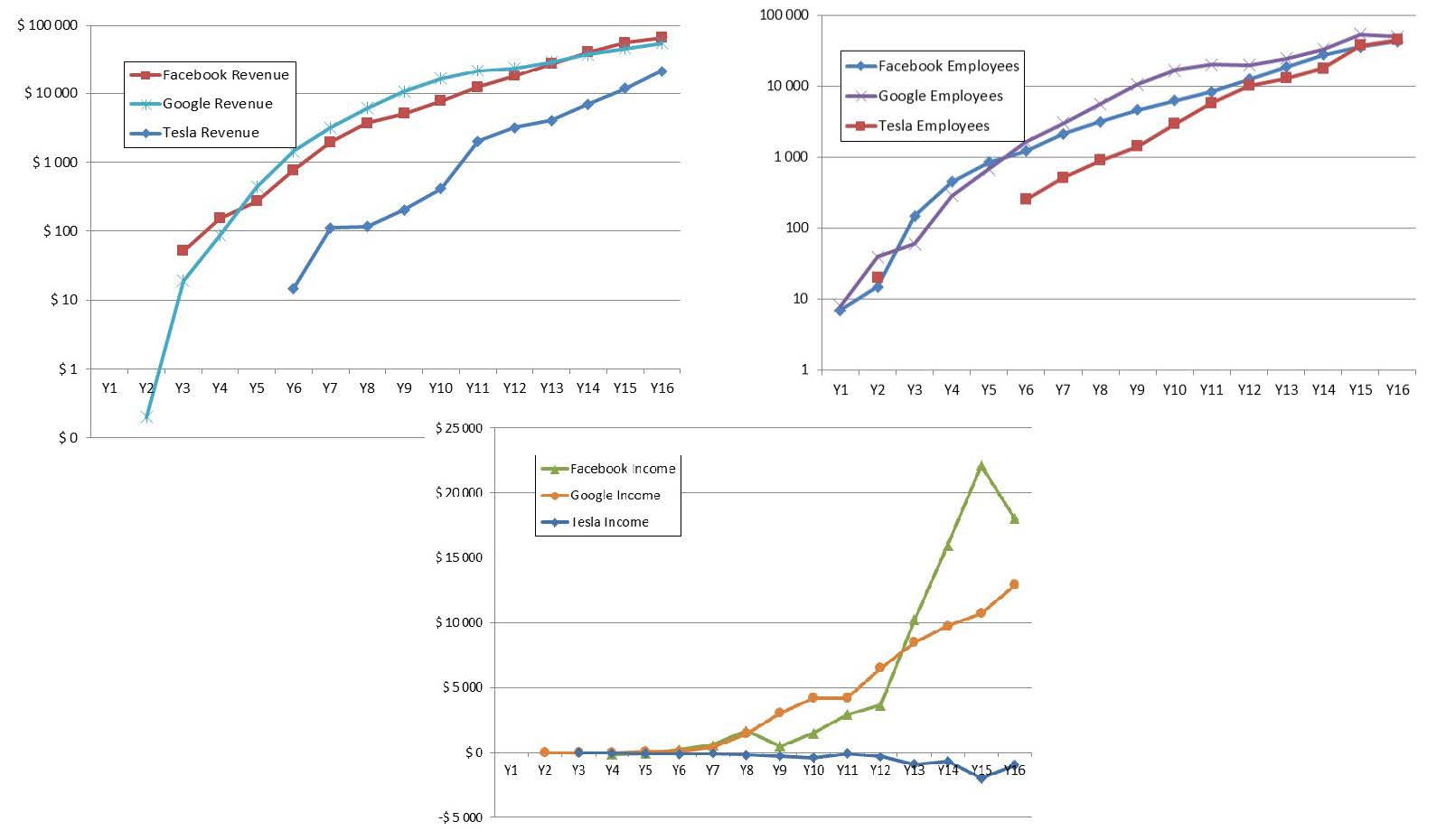

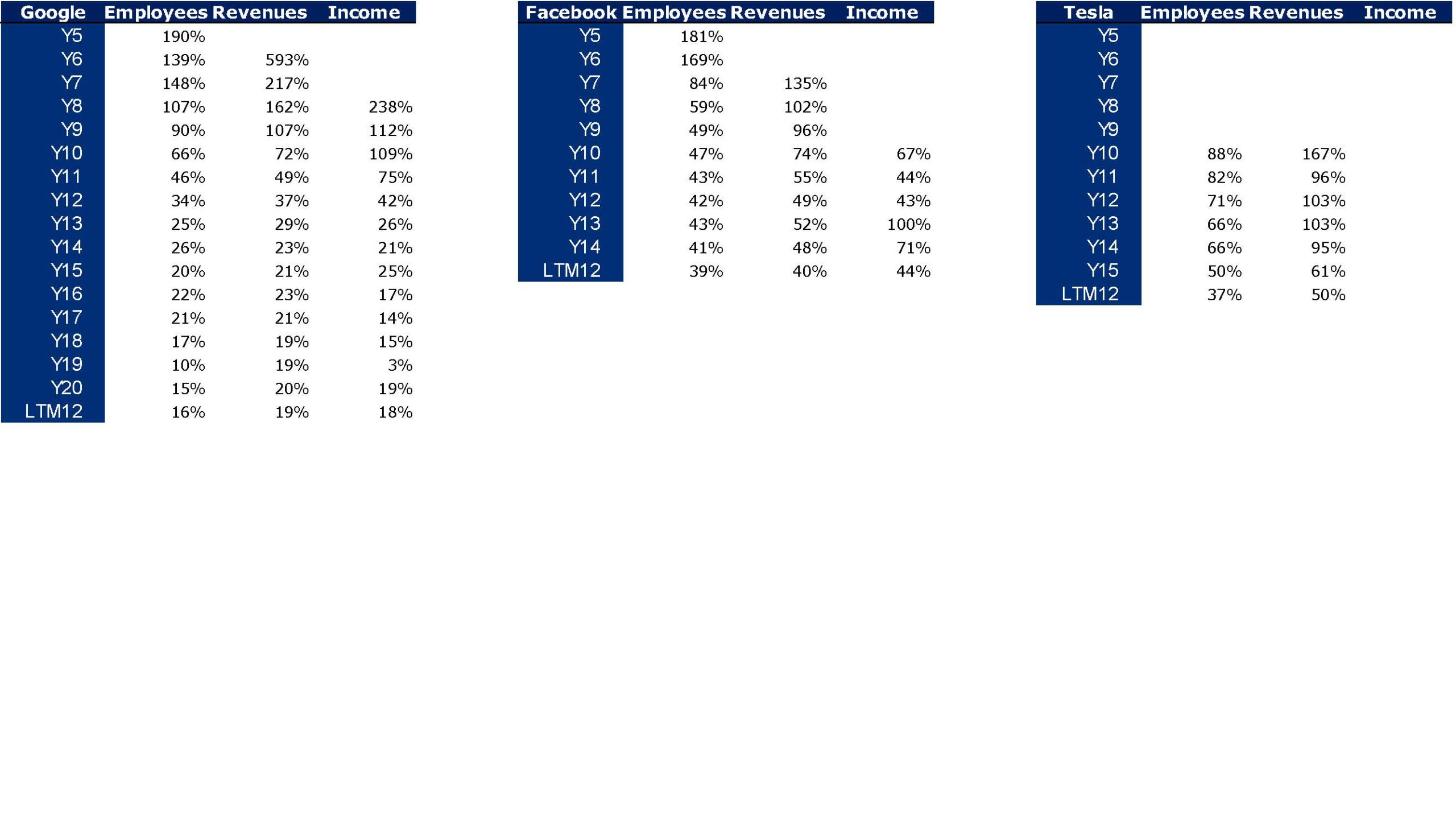

And here are my udpates abour revenue, income and employee growth of Google, Facebook and Tesla:

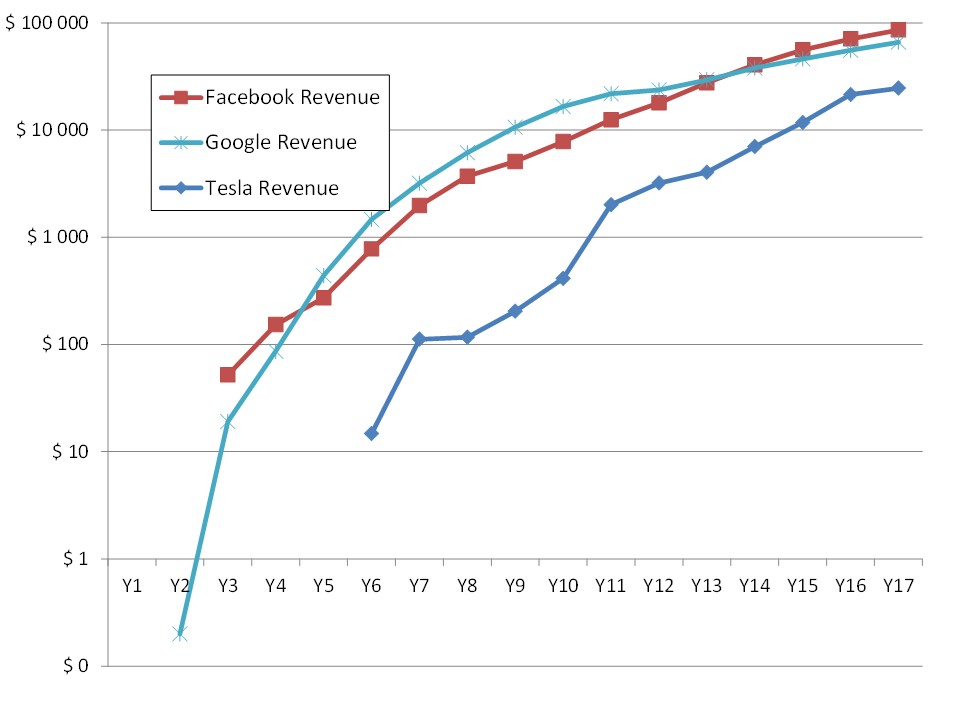

Revenues and profits are in millions of $. What is undoubtedly the most striking is the similarity of the growths of the three actors and of course the fact that all these numbers are considerable, not to say extraordinary.

Typical of Silicon Valley startups, the growth is often above 100% in the early years decreasing to about 40% after a few years and still above 15% after 20 years. This means respectively doubling the numbers every year, every two years and every five years.

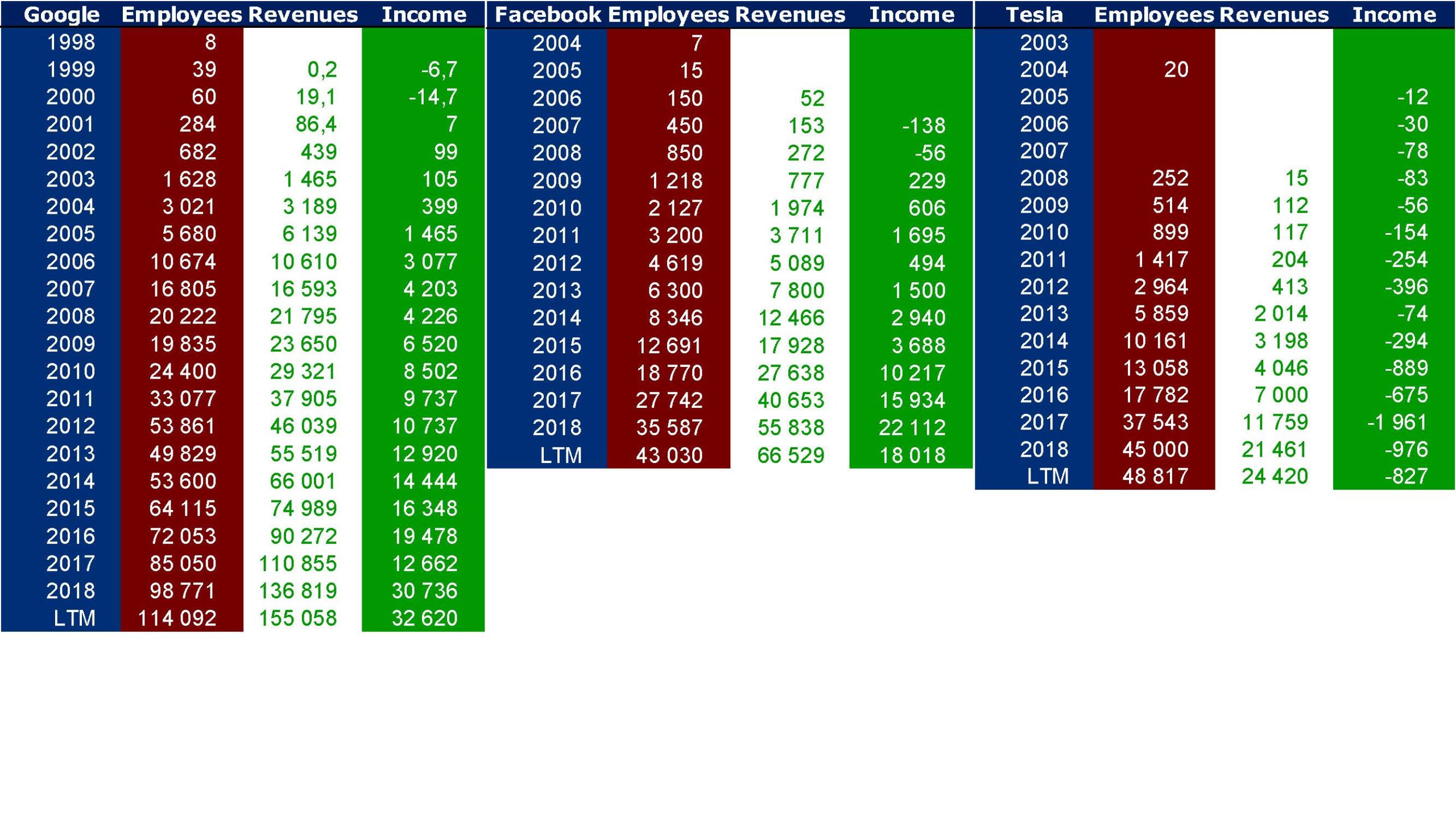

It’s by reading Nicolas Colin’s always interesting newsletter, European Straits #149, 10 Tech Giants That Are (Almost All) in Bad Shape that I decided to revisit quickly the growth of 3 tech giants that I have been following for many years now: Google, Facebook and Tesla. And here are their numbers in terms of thousands of employees, revenue and profit in $M.

If you really love numbers, here is a little more: their average growth of 5 years is about 20% for Google, 40% for Facebook and about the same for Tesla (except that they never made a profit). Google is older so it is not a fair comparison. here is a more precise analysis.

So are the three tech giants threatened? I am not sure given this steady growth.

I had already showed the power of networks when I commented Once you’re lucky, Twice you’re good a book subtitled The Rebirth of Silicon Valley and the Rise of Web 2.0. You can check again the web of people connected ten years ago or so. I had done the same with the older and now mature EDA industry. This new NYT article shows new connections illustrated by the new figure below:

Let me just quote the article: “The history of Silicon Valley has always been one generation of companies gives birth to great companies that follow”…”This is the story line of Silicon Valley, from Apple to Netscape to PayPal and now, to Facebook.” … and finally, “the social fabric of Silicon Valley is a dense set of overlapping spider webs, meaning everyone is connected.”

In my article on the web2.0, I had also shown the value creation. There had been $800M of VC money invested for a $17B value creation (mostly paper value). The new table below adds another $100M of VC money, and the value creation is now… $113B!!

Instagram co-founders Kevin Systrom, chief executive (right), and Mike Krieger at the company offices in San Francisco. Photo: New York Times / Redux / eyevine

– Who’s getting rich from Facebook’s $1bn Instagram deal? shows that it makes 10+ happy people! And using these data, here is my cap. table. I have to admit that the numbers are also speculative but based on the previous article, they kind of make sense.

The long-awaited filing of Facebook was finally published yesterday. Amazing numbers, amazing success. You’ll find below the capitalization table and revenue numbers I (approximately) built form the S-1 document and you can compare it to the exercise I had done in 2010.

According to my analysis (I tried to take into account existing shares as well as options and restricted shares differently), Zuckerberg owns 20% of the company, the investors (preferred stock) about the same. IPO shares could be 5%. You can also have a look at the different rounds. And the difference is common shares (which may include investors) and employee options. Finally, I cannot comment on founders’ shares and you may have a look at the old table again.

click on table to enlarge Facebook 2012 cap. table

Revenues of $3.7B, a profit of $1B and 3’200 employees in 2011. A possible market value of $100B and an additional $5B in the bank. Google did not have such numbers. (Google had $1.4B in revenues, 2’500 employees and raised $1.2B at the IPO. It was only 6 years old though whereas Facebook is one year older. In 2005, Google had $5B in sales, $1.5B profit and 6k employees!) I had already compared both in a post in 2010: Google vs. Facebook and I have update the curves below.

click on table to enlarge

In the last 4 years, the yearly growth of Facebook has been over 80% for revenues and over 50% for the number of employees. I might be over-optimistic by saying that the average employee stock value is $4M (because of investor ownership of these shares too). The cap. table which follows shows numbers as guessed in 2010 and published in a post entitled The Social Network, when the movie was released.

click on table to enlarge Facebook 2012 cap. table click on table to enlarge

The funny thing is that when I had lunch last week with a Swiss entrepreneur who needed contacts in Silicon Valley, I discovered that one my eBay contact was now at Facebook, one of my Microsoft contact was now at LinkedIn, so at the micro or macro level, there is something going on.

You know Google is one of my favorite topics. I regularly look at their growth for example. So here is it again. Too early to say if they are in the slowing part of the S-curve…

Facebook numbers? it’s rumors mostly so the graph below should be treated cautiously!

The funny thing is that I had noticed there was a relation at Google between employees and revenues, basically $1M per employee. Facebook looks slightly less efficient.

Silicon Valley has always been a war for talents. In the 90s, the electronics industry lost people to the Internet companies (you should remember that Yang and Filo, the founders of Yahoo! were studying in the field of electronic design automation) then Google was doing the same in the early 2000s, now it is about social networking. I would not worry too much for Google though. Not yet! As as Richard Newton was saying in EDA Cafe : “Silicon Valley and the Bay Area are cradles of innovation.” And he further added, stating a colleague of his: “The Bay Area is the Corporation. […When people change jobs here in the Bay Area], they’re actually just moving among the various divisions of the Bay Area Corporation.”

The new movie about Facebook’s founder, Mark Zuckerberg, is a great movie. It does not matter so much if it is a description of reality. You may watch it as a piece of fiction, and it would remain a great movie thanks to the actors and screenplay.

It is also great because it describes the start-up world in a very accurate manner. It is not a movie about start-ups really, but there are details which reminds me a lot of real-life stories.

The first lesson is that money and friendship seldom work together. The stories of Eduardo Saverin, the founder soon to be diluted, Sean Parker, the exhuberant founder of Napster and Plaxo and mentor of Zuckenberg and the short appearance of Peter Thiel are such examples.

It also shows the old world of Boston where people think ideas are crucial and the new world of Silicon Valley where what matters is implementation. It’s why Silicon Valley is the Triumph of the Nerds. It shows how right Paul Graham is when he says Silicon Valley is about nerds and money. You see the crazy, sad, exciting, depressing life of these hard-working people. You may like it or not, but it is mostly what start-ups are about.

I just looked for what some key people thought of the movie. So, for example, Eduardo Saverin said here: “The Social Network” was bigger and more important than whether the scenes and details included in the script were accurate. After all, the movie was clearly intended to be entertainment and not a fact-based documentary. What struck me most was not what happened – and what did not – and who said what to whom and why. The true takeaway for me was that entrepreneurship and creativity, however complicated, difficult or tortured to execute, are perhaps the most important drivers of business today and the growth of our economy.”

And Dustin Moskovitz said there: It is interesting to see my past rewritten in a way that emphasizes things that didn’t matter (like the Winklevosses, who I’ve still never even met and had no part in the work we did to create the site over the past 6 years) and leaves out things that really did (like the many other people in our lives at the time, who supported us in innumerable ways). Other than that, it’s just cool to see a dramatization of history. A lot of exciting things happened in 2004, but mostly we just worked a lot and stressed out about things; the version in the trailer seems a lot more exciting, so I’m just going to choose to remember that we drank ourselves silly and had a lot of sex with coeds. […] I’m very curious to see how Mark turns out in the end – the plot of the book/script unabashedly attack him, but I actually felt like a lot of his positive qualities come out truthfully in the trailer (soundtrack aside). At the end of the day, they cannot help but portray him as the driven, forward-thinking genius that he is. And the Ad Board *does* owe him some recognition, dammit.

Of course, this looks like corporate language, we should remember these guys have FaceBook shares! Talking about shares, there was another thing I did not like recently, the fact that according to Forbes, Zuckerberg would be richer than Steve Jobs. I had a discussion with a friend over the week end and he agreed with the statement whereas I disagreed. It may be a detail: but as long as Facebook is not quoted, Zuckerberg’s wealth is mostly paper value he can not really trade. I am sure he is already rich, he probably has already monetized some of his shares but not all of them whereas Jobs owns shares which are liquid. It may not be a big difference given the success of Facebook, but I have seen to many stories of start-ups where people thought the paper value of the stock was real wealth and the next day worth nothing…

When my daughter told me yesterday, she might at least explain her friends what her dad was doing. i.e. working in the world of start-ups, I thought the movie had at least reached that goal of reaching a large audience towards this important topic!

Final point, a recurrent topic in my blog: Facebook cap. table and shareholder structure. As Facebook is private, it is a challenge to know what’s true and what’s myth. I have still tried the exercice from what the Internet gives. One interesting feature is Saverin’s dilution from 30% to 5% whereas Zuckerberg went from 65% to 24%, not really pro-rata! We shall see when Facebook goes public, who wrong I was!

This is the third book I report on this blog about entrepreneurs. In fact it is the fourth if I include Inside Steve’s Brain (but this one is about a single entrepreneur). The two previous ones were interviews of many, i.e. Betting it all and Founders at Work. The beauty (and at same time weakness) of Once you’re lucky, Twice you’re good is that is is about web2.0. Is this new step in the Internet development a speculative bubble or a speculative revolution. It is probably too early to say even if author Tracy Lacy (appearing in another post) is quite convinced it is a revolution.

It is a beautiful book because it shows once again the richness of individual connections. I have done below my illustration of it. Paypal and its founders appear to be at the center of this network. Fairchild had such a similar situation at the beginning of Silicon Valley in the sixties, Apple, Sun, Cisco thereafter.

Another interesting element is about investors. There has been a popular idea that web2.0 was not funded by venture capitalists anymore because the web2.0 business angels who were web1.0 entrepreneurs had learnt their lesson. The situation is more complex as the web2.0 financing shows. Greylock, CRV, Accel but also Benchmark and Sequoia are vey active. Finally, it shows again and again what entrepreneurs are: passionate, driven individuals and I can only advise reading the epilogue about Levchin’s childhood. Quite fascinating…