Sometimes I publish posts which may be unreadable, they might be more for myself, not for other readers. In a way, this blog is my second memory… so I am not sure this post is worth reading…

There have been two major venture capital firms in history. So important, I have created hashtags for them: Sequoia and Kleiner Perkins. So not surprisingly Mallaby covers them both in his great book, but in different manners. According to him, Kleiner Perkins (KP) has lost its leadership. Both Sequoia and KP were #1 and #2 from 1980 to 2005, but since, Sequoia has kept its ranking and KP is not even in the top 10 partnerships (see page 413). KP is covered in the last part of Chapter 11, with subtitle The decline of Kleiner Perkins. The full chapter 13 is entitled Sequoia’s strength in numbers.

Mallaby has a lot of convincing arguments, from the team strategy to the diversification of the firm activity: Sequoia has now large growth funds, a hedge fund, even an endowment, and a presence overseas in Israel, China, India and even recently in Europe. And Sequoia’s performance looks impressive: Taking all its U.S. venture investments between 2000 and 2014, the partnership generated an extraordinary multiple of 11.5x “net” – that is, after subtracting management fees and its share of the investment profits. In contrast the weighted average for venture funds in this period was less than 2x net. (Data from Burgiss). Nor was Sequoia’s achievement driven by a couple of outlandish flukes: if you took the top three performers out of the sample, Sequoia U.S. venture multiple still weighed in at a formidable 6.1x net. Deploying the capital it raised in 2003, 2007 and 2010, Sequoia placed a grand total of 155 U.S. venture bets. Of these a remarkable 20 generated a net multiple of more than 10x and a profit of least $100M. (Proving it was not afraid of risks, Sequoia lost money on nearly half of these 155 venture bets.) The consistency across time, sectors, and investing was striking. “We’ve hired more than 200 outside money managers since I came here in 1989”, marveled the investment chief at a major university endowment. “Sequoia has been our number one performer by far”. [Page 320]

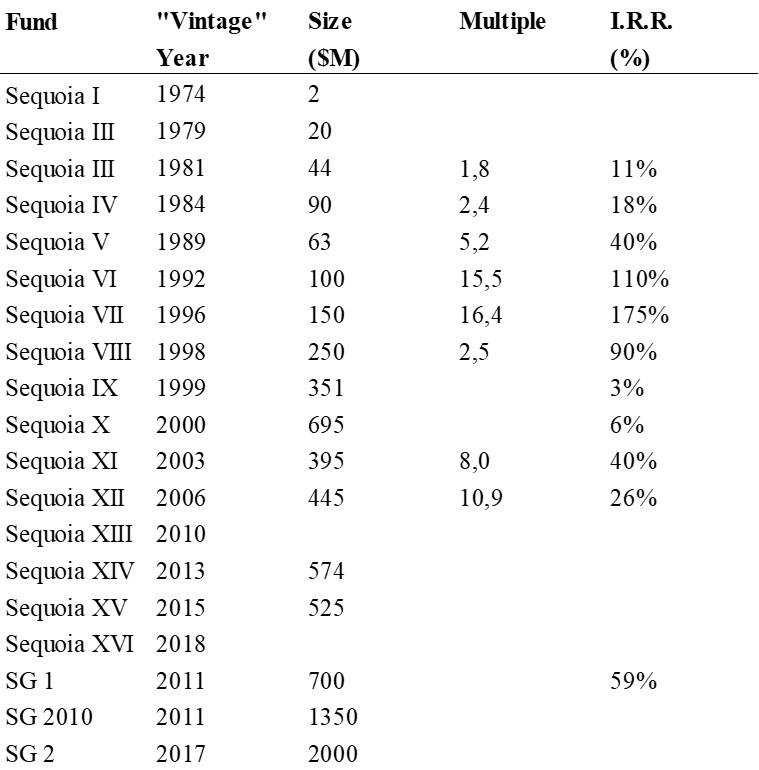

So I had a look at my own data. Here what I found about their fund history.

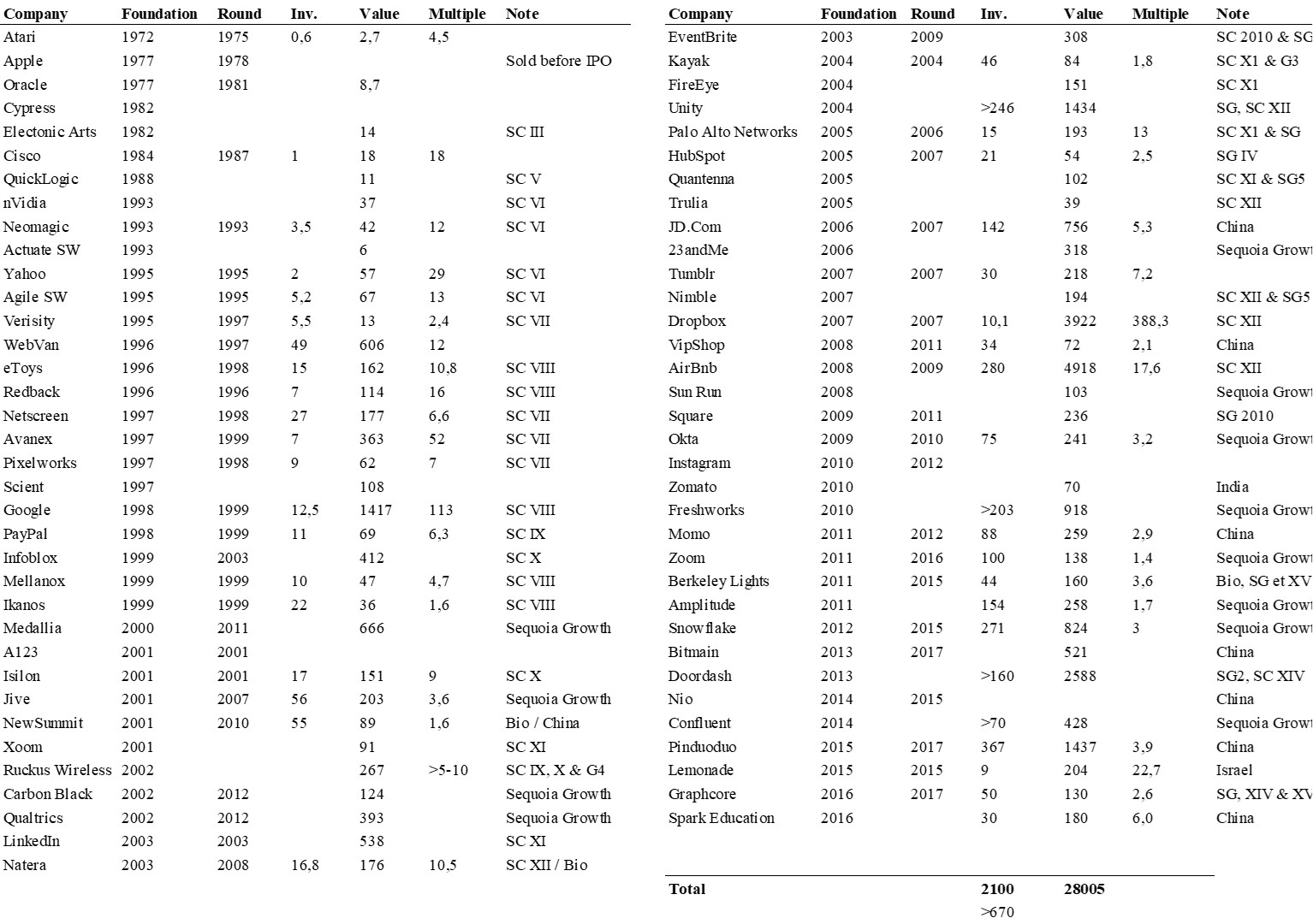

I also looked at my cap. table and found where Sequoia was an investor. When the data was available, I looked at how much the firm invested and what was the stake value at the IPO or acquisition. Indeed impressive.

PS (May 3rd, 2022): I just read a very interesting account of Mallaby’s book by Bill Janeway : The Forgotten Origins of Silicon Valley. Janeway likes the book and adds interesting criticism. Two points are not new, that is

– the role of government would be underestimated by Mallaby,

– East Coast VCs and the field of biotechnology are not analyzed well enough.

But a third point was newer to me: technology became open in the 70s and 80s (the PC, the operating systems, the networks including the internet) and this created huge opportunities for new companies. I have never been fully convinced by the first two points, motsly because the funding of research brings no guarantee to great innovations. But the third point is more intriging.

I just learnt the death of Don Valentine, the founder of Sequoia. For those of you who may not know him, you could visit my previous posts that mentions him, either through tag #sequoia or even better search Valentine. Just be aware he invested in Atari, Apple, Oracle, Cisco, Electronic Arts…

Or you may just read some of my favorite quotes of him:

“There are only two true visionaries in the history of Silicon Valley. Jobs and Noyce. Their vision was to build great companies … Steve was twenty, un-degreed, some people said unwashed, and he looked like Ho Chi Minh. But he was a bright person then, and is a brighter man now … Phenomenal achievement done by somebody in his very early twenties … Bob was one of those people who could maintain perspective because he was inordinately bright. Steve could not. He was very, very passionate, highly competitive.”

“Well, look, we’ll put up all the money, you put up all the blood, sweat and tears and we’ll split the company”, this with the founders. Then if we have to hire more people, we’ll all come down evenly, it will be kind of a 50/50 arrangement. Well, as this bubble got bigger and bigger, you know, they were coming and saying, “Well, you know, we’ll give you, for all the money, 5 percent, 10 percent of the deal.” And, you know, that it’s a supply and demand thing. It’s gone back the other way now. But, in starting with a team, it’s a typical thing to say, well, somewhere 40 to 60 percent, to divide it now. If they’ve got the best thing since sliced bread and you think they have it and they think they have it, you know, then you’ll probably lose the deal because one of these guys will grab it.”

In my regular work of compiling equity structures of start-ups, I fell twice in a row on Chinese start-ups. And twice, Sequoia was a large investor. And twice, they were incorporated in the Cayman islands. I do not know much about China, but this simple “discovery” is of interest. One start-up is in the Internet field, VIPShop, and the other one in biotechnology, NewSummit.

Click on table to enlarge

Here is the rather complex holding structure, which probably made possible a Sequoia investment in a Chinese start-up.

I tried to find some common features among the founders: none seemed to have studied or worked outside of China, which I think is interesting and somehow unusal with high-tech entrepreneurs. Their age: 32, 33, 36 and 37, which makes an average of 34.5. My overall average (see my analysis) over 257 founders is 34.9. I could not find any picture of them but this could be linked to the fact that the sites are usually in Chinese.

I just watched Something Ventured and I loved it. Loved it so much I plan to have it shown to as many EPFL students as possible in the spring! It is a movie about passion, enthusiasm, energy, changing the world and yes… about money. When asked about their hope about the movie, producers Molly Davis Paul Holland said: Our high hope for this film is that every student that wants to be an entrepreneur—at every level, high school, business school, on corporate campuses—sees it. We want to see more young people fall in love with entrepreneurship… And if we have a quieter, more serious goal, it’s that I want policymakers to look at this and say ‘What can we do to make it easier, not harder, for people in this country to start those kinds of businesses?’

I would have said I hope that every student — at every level — sees it. And the producers added we were trying to explain our vision for the movie and said, ‘What we are envisioning is a movie like Reds [Warren Beatty’s 1981 film about the original Bolsheviks], where you go back in time to talk about an exciting period — in that case 1917 Russia — and ask people in the present day what it was like back then. Dan said ‘Ok, so you want to make Reds but without the Communists.’ That is ultimately what came about: A really beautiful dialogue with really interesting men and the people they financed.

“A Film About Capitalism, and (Surprise) It’s a Love Story.”

This is the title of another article about the movie, where the journalist says “moviegoers can see what might be the rarest bird in the documentary world: a genuine love story about capitalism.” Somewhere else, the moviemaker, Dayna Goldfine explains: “I think what compelled us to take this one on, even though it is a positive view of business, was, one, it’s a chance to do this kind of alternative view. But also, what these guys were doing – both the entrepreneurs and the venture capitalists – was creating real products. So much of what has come down in terms of the financial tragedy of the last few years has been caused by the investment bankers –people who were really just creating financial instruments, as opposed to changing the world with technology by creating or funding an Apple Computer, or a Cisco Systems, or a Genentech”. Co-moviemaker Dan Geller adds: “I wouldn’t say that money was incidental – money was important – but the overwhelming enthusiasm was for taking these brilliant ideas and these inchoate technologies and making something earth-shattering with them. That’s the energy, I think, that comes through in these stories.”

Yes it is a movie about capitalism, about business. But it is also a movie about enthusiasm, happiness, failure also. It begins in 1957 with Fairchild and Arthur Rock. It could have begun with French expatriate Georges Doriot. A professor at Harvard who supposedly taught manufacturing (in fact it was about how many glasses to drink at a cocktail party and how to read newspapers – go to obituaries), Doriot did not create venture capital with ARD (even if he funded Digital Equipment – DEC) – Rock created the term later, but Doriot inspired most of the heroes of the movie: Tom Perkins, Bill Draper, Pitch Johnson, Dick Kramlich. And these guys funded Intel, Atari, Apple, Tandem, Genentech, Cisco. (The movie tells stories from the 60s to the 80s, but Google, Yahoo, Amazon, Facebook could have been added). Indeed with the movie, the Social Network, it’s the best movie I have seen about high-tech entrepreneurship. What I had nearly forgotten in The Social Network is the closed Boston society (Zuckerberg desperate efforts to enter high-end social clubs). Here also, the Wild West explains its success through openness and risk taking.

And the authors did not cheat. It is also about painful memories, how Powerpoint ended up in Microsoft hands, maybe because the entrepreneur had found it too tough before or how one of the rare women in this world, Sandy Lerner, the co-founder of Cisco, may have not forgiven her firing from the company she had created: “you gotta understand the game that you’re in. […] Look, there wasn’t a box for me.” So yes, it is also about failures, “living deads”, but there is a “feel good” attitude, funny moments, such as when Valentine visiting the Atari factory does not recognize the cigarette brands he smokes!! Or when Gordon Moore (the famous Moore law) remembers that Intel went public the same day as PlayBoy.

So if you do not know much (or even if you do know a lot) about Fairchild, Intel, Atari, Tandem, Genentech, Apple, Cisco, and even if you do not care about entrepreneurship, run and watch Something Ventured. Hopefully you will care!

I end 2012 with two posts related to my beloved Silicon Valley. This one is about the two great Venture Capital firms Sequoia Capital and Kleiner, Perkins, Caufield and Byers. The next one will be about Palo Alto-based author of thrillers, Keith Raffel.

The recent IPO of Jive is the motivation for this new post because Jive has both funds as co-investors. I am obviously providing my now-usual cap. table and what you can discover here is the huge amounts of money both funds have poured in the start-up ($57M for Sequoia and $40M for KP) … is this still venture capital? I am not sure.

Click on picture to enlarge

I am not writing an article on Jive here but let me add that we have again here two founders who had each 50% of the start-up at creation and end up with 8%, the investors have 30%. What is really unusual is that the company raised money in 2007, six years after inception. A sign of a new trend in high-tech?

Now back to Sequoia and KP. When they co-invested in Google in 1999, I thought it had been a very unusual event. David Vise in his Google Story (pages 66-68; I also have mine!) explains how the start-up founders desired to have both funds to “divide and conquer”, hoping no single fund would control them. When I met Pierre Lamond, then at Sequoia, in 2006, I was surprised to learn from him that in fact the two funds has regularly co-invested together. As often in Silicon Valley, it is about co-opetition, not just competition.

So I did my short analysis. A first Internet search got me the following:

– The question on Quora “How unusual is it for both Kleiner Perkins and Sequoia to co-invest in a company?” (August 2010) gives 11 recent investments, including Jive and Google.

– Russ Garland in the Wall Street Journal adresses the topic in “Kleiner Perkins, Sequoia Combo Has Solid Track Record” (July 2010). He says: “But the two Menlo Park, Calif.-based firms have done plenty of other deals together – at least 53, according to VentureWire records. It’s been a fruitful relationship: 29 of them have gone public. They include Cypress Semiconductor Corp., Electronic Arts Inc., Flextronics International and Symantec Corp. That track record lends credibility to the excitement generated by the Jive investment. But most of those 53 deals were done prior to 2000; the two firms have been less collaborative since then. Of the handful of companies that both Kleiner Perkins and Sequoia have backed since 2000, at least one is out of business. That would be Abeona Networks, a developer of technology for Internet-based services.”

– Now in my own Equity List, I have 4 (Tandem, Cypress, EA, google) plus Jive.

So I did a more systematic analysis and found 55 companies. More than the WSJ! I will not put the full list here, but let me give more data: Kleiner has invested a total of $267M whereas Sequoia put $268M [this is strangely similar!], i.e. about $5M per start-up. On average, KP invested in round #2.07 and Sequoia in round #2.63, so a little later. Time to exit from foundation is 6.5 years. I found 27 IPOs (I miss two compared to the WSJ)

Is Garland right when he claims “But most of those 53 deals were done prior to 2000; the two firms have been less collaborative since then”? Here is my analysis:

Number of co-investments related to the start-up foundation year

If I look at the decades, it gives,

70s: 6,

80s: 30,

90s: 11,

00s: 7.

Clearly KP and Sequoia co-invested a lot in the 80s, much less in the 90s and 00s. Whereas the fields are

So what? I am not sure 🙂 . KP and Sequoia are clearly two impressive funds and as a conclusion, I’d like to thank Fredrik who pointed me to Business Week’s The Venture Capital Winners of 2011.

Sequoia and KP may not be #1 and #2, but their track record remains more than impressive. Here is a bad picture taken on an iPad!

I am surprised not to have published this before. It was one of my first work before I even wrote my book. It became its chapter 4. Venture capital is about 50 years old and it has changed a lot in parallel to innovation and high-tech. I hope you will enjoy these very visual slides!

Another fo my recent reading from old Red gerring magazines. The analysis and predictions are great and provide good lessons for our days… In the same feature, October 98, I found small articles about companies we backed at Index. These three companies went public later on… so a small additional piece for nostalgia.

Prepare for dramatic Internet company wreckage.

By Anthony B. Perkins

ONE 0F THE surest reality checks in the technology business is a visit with Don Valentine of Sequoia Capital. Mr. Valentine’s seed money and sound advice have been instrumental in many of Silicon Valley’s greatest success stories, including Apple, 3Com, Cisco, and Yahoo. He, along with Netscape founder Jim Clark, was the first to proclaim in our pages, back in 1994, that Internet was indeed the information highway, and not just a “TV with a pizza box sitting on top” (see “Don Valentine’s Next Big Bet Is on C-Cube Microsystems,” May 1994 page 58). We recently prodded the curmudgeonly Mr. Valentine to tell us how he thinks the Internet market will play out. His insights are instructive.

First he notes that, like the microchip and PC markets, the Internet market grew organically rather than because it solved any obvious problem that was important to a large group of people who had a lot of money. Mr. Valentine recounts being at Fairchild Semiconductor when he and future Intel founder Bob Noyce marveled at the invention of the microchip but at the same time wondered what it was good for. The early days at Apple were much the same. “I remember wondering what people were going to do with the Apple II. There was no answer!” Mr. Valentine declares. In contrast, the networking boom was about solving big, important problems for corporations. “When Cisco came along, it was addressing an environment desperately in need of a solution,” he explains.

From a venture capital perspective, Mr. Valentine believes that it is better to invest in markets clamoring for new products than in creating new markets. “In the two previous eras—microchips and PCs—lots of companies went over a cliff,” he says. “Uniquely in the networking world, there are almost no busts.” Extending his logic, Mr. Valentine foresees what we have been predicting for a couple of years now that the Internet space will suffer dramatic company wreckage as well. Another veteran VC, Jim Breyer of Accel Partners, concurs with this analysis: “Ninety percent of the Internet companies that exist today will eventually go out of business.” And Mary Meeker of Morgan Stanley Dean Witter says that roughly 75 percent of the Internet companies that went public in the past four years are now trading below their initial public offering prices.

According to Mr. Valentine, part of the overfunding of these markets-in-creation can be attributed to the infamous herd mentality within the VC community. “We financed 6o disk drive companies because each venture firm wanted to have a disk drive investment in its portfolio,” he tells us. “The reason we have so many search engines is that Yahoo got visible. Lots of VCs didn’t have one of those. So they created an Infoseek or an Excite or whatever, and jumped on the back of the train. We are making the same mistake in the Internet era that we made in the PC era. Just think about the environment. There is no application in which the Internet solves a problem. What does the Interne do so far? It sort of reminds me of the Apple computer in 1978. It doesn’t do anything.”

Mr. Valentine feels certain about one aspect of the Internet: that it represents the most efficient marketplace for goods and services on the planet. “Never before has the consumer had all the cards dealt face up where he can make choices and decisions knowing all the facts,” he says. “In traditional marketplaces, consumers have always had to deal with confusion, arcane language, and obfuscation. Buying something is often a hassle. Insurance is a great example of this; dealing with car salesmen is another. Now consumers are being put in a position in which they have phenomenal access to whatever they want.” This may seem of obvious value to businesses—especially when you look at the revenue trajectory of an Amazon.com or contemplate the 10 million’s worth of computer equipment that Michael Dell is selling online every day— but the only thing that is really obvious is the value to the consumer. We ask the same question that the salty Mr. Valentine does: “How do you make money in this perfect marketplace?” Our problem with Arnazon.com has never been its sales potential; rather, we wonder whether it will make technology-industry-level margins.

I threw Mr. Valentine’s comments out for discussion at dinner last night with Broadview CEO Paul Deninger and Red Herring editor Jason Pontin, inciting a lively debate. From Mr. Deninger’s perspective, Amazon.com may well be the exception, not the rule. “Look, Jeff Bezos at the right place at the right time with the right product,” he said. “But for every Amazon.com, there will be 20 flameouts.” His main point was that “e-commerce is a new way of conducting commerce electronically, but not necessarily a new industry.” Jason piped in with his theory that the disaggregation effect of the Internet “creates room for re-aggregation.” (By this time we had gone through our fourth bottle of wine.) And I believe Jason is quite right. Now that portals have better organized the Web, and Amazon.com has shown everyone how to conduct Internet commerce successfully, it’s time for the rest of the world to jump into the game. Instead of relying on Yahoo and the major portals to organize your experience, you will build your home page with links into the “miniportals” representing your specific interests. Eventually, all major product and service distributors will go online and fend off startups like Arnazon.com that are eyeing their lunch.

One defender of the miniportal revolution is Jim Moloshok, senior vice president of Warner Brothers Online. At our recent Herring on Hollywood conference in Santa Monica, California, Mr. Moloshok au but declared war on Sillcon Valley’s search-engine geeks. He warned Hollywood’s studio producers and new-media types that they are in danger of losing control of their online destinies if they don’t stop giving away their valuable television-, film-, and music-related content to Internet companies starved for programming, and that they should start demanding better licensing terms. “Entertainment companies are mortgaging their online future,” said Mr. Moloshok. “They’re giving away their content in exchange for exposure. But the entertainment companies are basically underwriting these Internet companies by throwing away their intellectual currency.” All this debate left me agreeing with Mr. Valentine’s basic premise: the Internet is still a market-in-creation. Although we have our arms around the idea that it represents a vast and efficient distribution channel and will provide a stream for investment news and entertainment content, its real value has yet to come into focus. And as we grope along this trail, we will continue to see fledgling companies like Broadcast.com and GeoCities go public. But we’ll have to wait a while to sec which cars stay on the road and which ones fly off the cliff.

[For Tony Perkins’s free weekly newsletter, send an email with subscribe in the suhject line to tonynet@redherring.com.]

I have a short memory for things but when I focus on one point, I stick to it for a few days. After finding a few things on Valentine, I digged a little more and found again the interview I used in my book when he compares Steve Jobs to Ho Chi Min (“We financed Steve in 1977 at Apple. Steve was twenty, un-degreed, some people said unwashed, and he looked like Ho Chi Min. But he was a bright person then, and is a brighter man now”).

There he also explains why Silicon Valley can not be replicated. Here it is:

“There is no question. It’s very difficult. And over the years we’ve been visited by hundreds of people from every country in the world, almost all of the states in the country. They all want to figure out and clone what causes Silicon Valley to exist and thrive. Many or most of the visitors are interested in the underlying employment creation. But if you look at venture capital, it only works two places in the world. It doesn’t work outside the U.S., and it only works in Boston, or the greater Boston area, and in Silicon Valley. Basically, almost no other major financial center in the world has ever generated companies of consequence and providence that is so large and visibly successful.

And you can blame it on the weather. You can give credit to the great universities. You can explain that the venture community here is stronger and more experienced than other parts of the world. But the mystique of why it works is still very hard to narrow down to six or seven simple declarative sentences. And it – it is a local bit of magic that – works at this particular point and time. The duration of the venture industry is probably only from something like 1960 through the present, so you talk about not even half a century. [The interview is dated 2004…] It – it’s still a new and – and sort of closet-like form of financial engineering. We don’t think of it as investing at all. We think of it as building companies, often times building industries. And it’s an entirely different mentality and attitude than in the traditional idea of buying and selling things. And this is not a place where you buy things; this is a place where you build things. And you participate in the founding team that creates an entirely new company and sometimes a new industry. And now there are far more practitioners.

But if you go around the world, the Research Triangle in North Carolina was going to be another magic spot. Well, you can’t name a great company, it’s never been started there. You can look at other centers. Seattle – well, there is a great company there. Maybe there are two great companies there – they include Nike. And – has anything happened in the last twenty-five years in that community other than Microsoft and Nike? And the answer is not a lot. [Well he forgets Amazon!] Lot’s of companies have started. Lots of things going on, but not a lot of monumental success. I mean it’s unbelievable the number of companies that have gained prominence, have revenues of a billion dollars in this tiny, little valley. So it is a bit of enigma what all the ingredients are that everybody would like to clone and take away.

I once tried to explain to the Deputy Prime Minister of Singapore who was here trying to take back the magic, and I said it’s a state of mind. You can’t take it back. Somehow or other you’d have to move your people here and they would have to have their DNA changed so that when they went back to Singapore, there was a DNA adjustment in the way they thought, the way they were willing to take risks. I mean in a place like Japan, if you start a company and it fails you’re disgraced. Some people would commit suicide – if that happened.”

“And here – you – you start a company and you fail, some of the best people are better after their failure than before their failure. So you don’t have the stigma of failure. In Ireland, I can’t imagine with jobs so hard to come by, somebody would leave a good job in a country like Ireland to – to run the risk of their company failing. And a place like Germany, it’s so rigid you’d be socially ostracized, I suspect, if you started a company and – and it didn’t work.

Environmentally here – the other ingredient I forgot to mention and it’s more true now than it ever was, the – the community is built up of emigrants and immigrants. So almost all of the people who have started or participated in starting these great companies have come from some other state. Noyce was from Iowa. Went to Grinnell College. And there’s a – Gordon Moore might be an exception of somebody who was born in California. So we have a whole history of emigrants coming from all over the country, and in the last ten years more than ever, we have a huge population coming from Southeast Asia. It – a month doesn’t go by where Sequoia doesn’t start a new company populated by Indians. Fabulously educated, brilliant entrepreneurs, they come from an economic system that is so different from ours it’s hard for me to understand it, although about once every two months I get a lecture from some entrepreneur who says that you don’t even understand your own system.

You don’t understand how unique it is and – and then the fact that it doesn’t exist anywhere else in the world. So there is something here that is – that is different as perceived by the people who purposely immigrate here.”

Those who follow my blog know I am interested in the history of Silicon Valley, start-ups and venture capital. I had published a while ago data about Kleiner Perkins’ first fund. I’ve been trying ( and I still do) to find data on Sequoia’s first fund (Atari, Apple, Tandem, Altos) without much success [anyone with data on Sequoia I is welcome to contact me!) but today I found an interview fo Sequoia’s founder, Don Valentine, given to Inc. magazine in May 1985. What he told about start-ups, entrepreneurs, investors and big corporations could be said again today. I put in bold characters what stroke me. Enjoy, even if the interview is rather long.

Now I just found a recent interview of Valentine (dated October 2010). Though given 25 years later at Stanford Graduate School of Business, it does not seem valentine has changed much his values and beliefs.

Peaks And Valleys

Venture capitalist Don Valentine scaled the entrepreneurial heights as a key investor in Apple Computer, Altos Computer Systems, and Tandem. Now, amidst uncertainty in Silicon Valley, he talks of opportunity, company building, investor madness, and the failings of the business press.

He speaks like the New York street kid he used to be, but Don Valentine understands the challenges facing California‘s high-technology entrepreneurs better than most Californians. At 47, the feisty venture capitalist ranks high among the deans of Silicon Valley‘s much ballyhood investment community.

Not that this reputation has made him universally beloved. Gruff sometimes to the point of rudeness, he can be a formidable for of foolishness. As the marketing manager of the then fledgling National Semiconductor Co., Valentine is to have scolded a subordinate so severely on one occasion that the poor fellow fainted dead away. Other victims have also felt the lash of his wit: entrepreneurs and journalists, to name a few.

Despite his prickly manner, Valentine is widely admired among those entrepreneurs who have taken his money, and, more importantly, benefited from his intimate knowledge of building companies in emerging growth industries. The son of a New York City Teamster official and a graduate of Fordham University, Valentine won his spurs in the infant integrated circuit business — at Fairchild Camera and Instrument Corp.‘s semiconductor division from 1960 to 1967, then at National Semiconductor Corp. until 1971.

He then formed his own venture capital firm, Capital Management Services Inc. (now called Sequoia Capital), which was a key early investor in more than 100 California high-technology companies, including Atari, Apple Computer, Tandem, Altos Computer Systems, LSI Logic, and Cypress Semiconductor. With these and other successes, Sequoia Capital over the past 10 years has earned its limited partners returns in excess of 60%.

For all his triumphs, Valentine insists that he doesn’t back in the media’s glorification of his trade. Indeed, he deplores it. And now that the press has decided to deflate the industry’s once-buoyant image, he professes to be relieved. He knew failure, too, in the midst of his successes: Pizza Time Theatre was a Capital Management-launched company.

At the same time, Valentine has not lost faith in the future of U.S. entrepreneurism. Looking out of his office window at the rolling hills above Stanford University, sipping a mug of tea, he reflects that entrepreneurs need only remember the key qualities that have made for their success in the past — the courage to be different, to create markets where none existed before, and to invent radically new ways of doing business. With such weapons, he argues, entrepreneurs can continue to enjoy surprising triumphs against their larger, more entrenched competitors.

INC.: What’s going on in the venture capital business these days? Do you still have people pounding on your doors with new Apple Computers, or new add-ons for the IBM?

VALENTINE: Amazingly to me, yes.

INC.: What do you say?

VALENTINE: Well, the first thing I ask is, “Why, in 1985, do you want to do this? What do you see happening in the world that leads you to believe that you can make a real company, achieve whatever you want to do as an entrepreneur, and at the same time allow us to make a consequential return on the risk we take?”

INC.: And what do they reply?

VALENTINE: Unfortunately, many of them start talking about the installed base, how many are being produced — that sort of thing. They often don’t seem to have any sense that the race has been run, that there’s no longer an opportunity for the modest technical contribution to the evolving family of Apple or IBM boxes.

INC.: Does that mean there’s no more room for anybody in the microcomputer industry, apart from those two?

VALENTINE: Oh, I think Radio Shack is probably a well-entrenched company. They have their own distribution channel, which kind of helps them. And Commodore has staked out a very strong position in Europe and at the very low end. But I wonder if that’s not it.

INC.: What about the IBM-compatibles, the Coronas or the Compaqs?

VALENTINE: I have never believed it was possible to invest and make substantial returns by being compatible with IBM — anywhere, at any time. Not in mainframes, not in disk drives, and certainly not in personal computers.

INC.: The conventional wisdom says you have to be compatible with IBM.

VALENTINE: I think the conventional wisdom must be comprised of what goes on in people’s heads who have no sense of history. There are no historical examples where IBM compatibility has produced anything except annihilation.

INC.: OK. But if computers are not, where do you see any new fields of opportunity?

VALENTINE: Right where they have always been. One of our theories is to seek out opportunities where there is major change going on, a major dislocation in the way things are done. Wherever there’s turmoil, there’s indecision; and wherever there’s indecision, there’s opportunity.When it becomes obvious to anybody who reads Time magazine that it’s useful to have a disk drive on a computer, then it’s already way too late in the cycle to invest in disk drives. So we look for the confusion phase, when the big companies are confused, when other venture groups are confused. That’s the time to start companies. The opportunities are there, if you’re early and have good ideas.

INC.: Can you be more specific?

VALENTINE: Sure, the telecommunications industry is a good example. The regulations are unclear, the interpretations are unclear. So the big companies don’t know what they’re allowed to do and what they’re not allowed to do; and neither do the regional companies. They don’t know what they can sell and what they can’t sell. The venture business has never been a business of taking the big companies head-on; in fact, it is always a business of avoiding taking them head-on.

INC.: So the success of venture capital depends to some extent on there being a lot of confusion in the market-place, or at least in the minds of big companies. Is that right?

VALENTINE: Well, I don’t want to leave you with the impression that we’re so much more clever than the people who run big companies — that only we, the venture people, can see through the murkiness. On the other hand, big companies do suffer from certain disadvantages — implementation, for instance. Oftentimes, a big company will develop something, but then it will languish around and never get into production, or get into production too late. Take everyone’s favorite example, the personal computer. Long ago it was too late to be in that business. So what did the big computer companies do? They launched their own personal computers: Wang, NCR, HP, and I don’t mean to leave out Data General and DEC. Now some of those companies might be buying the product from someone; they might get it on an OEM basis, or a license basis, or coventuring it. But it’s all an example of a time when we should be moving in another direction.

INC.: Still, we’re hearing a lot about big corporate types beginning to see the value of “intrapreneurship,” small niche marketing, and so forth.

VALENTINE: I don’t know about all that. Big corporations flap their lips a lot about all the great things they’re going to do, but basically they’re obedient people. When you run a big company, it’s like running anything else that’s big, a church or an army: The key ingredient is obedience. Anything big requires people performing and acting in conventional, predictable ways — within the rules. Entrepreneurism is by comparison the role of the nonconventional person who’s going to do it differently. And in the big corporation, he’s just a flat-out pain in the ass. He doesn’t get through the industrial relations department, because that’s why you have an industrial relations department: to make sure the oddballs don’t get in and create confusion in the obedient world.

What you’re hearing is a fashionable reaction to a currently overreported event. Entrepreneurism is “in”; therefore corporate cultures have to embrace it in order to appear contemporary. I think that after the fad has passed, the big corporations will discontinue it, like affirmative action and the employment of women and all the other bullshit things they do for public appeal. This, too, will pass; and in another two years they’ll be on to something else.

INC.: Yes, but affirmative action accomplished something. Women and blacks were hired. They’re still working. Won’t this intrapreneur faddism, as you call it, leave some of its spirit behind, even after it has passed?

VALENTINE: I would be surprised. The progress of minority groups, the progress of women, is because fundamentally, as individuals, they are contributors, of sex and color. There’s no fundamental reason why intrapreneurship is going to be useful to a multibillion-dollar company.

INC.: You think it’s all public relations, nothing that’s deeply felt?

VALENTINE: Yes. Big corporations are made up of several ingredients.One part is public relations. But another part is accounting. Big companies are run by accountants, whose mentality is to control things, to homogenize things. That’s what control is: sameness, predictability. Look at what happens to an entrepreneurial company when it’s acquired by a giant. The giant comes in and says: “We have to change a few of the rules. Don’t worry; we’re not going to change the company. We just want you to think about a few things. You’ve got to have a compatible health plan. Ours is better than yours, so we’ll fix that. And this accounting firm is really better than your accounting firm, so we’ll fix that, too.” It’s death by a thousand cuts. A little nick here, a little cut there, a little change here — nothing significant. But at the end of a short period of time the people are so driven by controlling and accounting that the environment of nonconventional solutions is lost.

INC.: So you’re saying that big companies are doomed in their efforts to coopt the entrepreneurial spirit.

VALENTINE: Yes, but not the entre-preneurial product. The bioengineering world may be a good example. The bioengineering product is a technique, more a manufacturing process than a freestanding product. And the logical people to be in the biolengineering business are the pharmaceutical and drug companies, right? So why, then, do you have all there bioengineering firms starting up since 1978 or so? I think what happened was that the big pharmaceutical companies had other fish to fry. They had their scientists grinding away on other products. But meanwhile they saw all these little companies getting venture financing, and what they did, cleverly, was to point some money at this one, then at that one, knowing that later they would catch up with them. They knew that the venture companies couldn’t walk the new interferon drug, or whatever, through the Federal Drug Administration cycle, into production, and into the marketplace. That’s a very expensive process and requires a lot of know-how. They knew that the little companies didn’t have that kind of wherewithal. But the big companies did; so that when the time came they knew that they could come in and pick up the marketing rights from the little companies.

INC.: You seem to have a lot of ideas about big companies. Have you ever worked at one?

VALENTINE: That depends on what you mean by “big.” I worked at Fairchild, where I joined an already existing sales force and sales concept, and I managed it up to $150 million from the mid-20s. Then, at National Semiconductor, I got the opportunity to design a sales concept and sales force from scratch. They were losing about $2 million when I got there, and by the time I left they were earning about $40 million. I enjoyed that. I like taking the proverbial blank piece of paper and designing another approach to doing things. It matched my personal goals. But then I found myself no longer challenged. More important, I found that I didn’t like companies when they got to $40 million or $150 million. I hated them.

INC.: What was it you couldn’t stand?

VALENTINE: Success, I think, is what I couldn’t stand. When a company succeeds, the founders no longer have a personal impact on strategy, no longer have a direct contact with the customers. They become managers and superiors, while all the other guys who work with them have the fun. And if you don’t let them have the fun, you can’t keep them. I like doing things personally. I like seeing the customers, the applications of a product. I don’t like seeing them through a sales force. By the same token, I like planning products and strategies, personally, not through three layers of people. So I opted for venture capital, where I could act personally and permanently in a small-company, fast-track, growth environment — somewhat as a dilettante rather than a full-time manager. Managing a company that was growing at 10% or 20% a year wasn’t even an option for me. I wanted an environment where I could invest in small companies and enjoy their success, modestly contributing at the strategic level. Venture capital is where I can do that, and in a multitude of companies at the same time.

INC.: Let’s talk about how that works. When an entrepreneur walks into this room, looking for money presumably, how do you size him up?

VALENTINE: The characteristic we’re concerned with every time is whether the person knows what he doesn’t know — whether he’s mature enough to recognize it, talk about it, and do something about it. That’s one of our critical tests. Many entrepreneurs have incredible blind spots. For instance, they are often, correctly, said to be insensitive to the importance of sales, or manufacturing, or how to get good gross margins. They’re not deliberately blind; they just haven’t thought about those things.

INC.: How do you test for blind spots?

VALENTINE: We discuss it. We ask them about their products, their approach, and what skills they think are crucial to the company’s growth. Then we want to know whether those skills are resident in the team; and if so, who has them; and if not, why not, and where they’re going to come from. Our world is one of constant Socratic questioning. We spend a small part of our time trying to find out which questions are relevant, and the rest of it we spend listening.

INC.: How important to you is the business plan?

VALENTINE: Most important, but for a not very obvious reason. We must have something that will tell us how people think. We get one or two of these plans every day and we can’t possibly understand the nuances of every business. So the business plan to us is where we begin to learn about the people. We can’t tell whether the numbers are right, therefore we concentrate on how they reached the numbers, the thought processes that led them to conclude that their project was possible.

INC.: Where do most entrepreneurs fail in their thinking?

VALENTINE: Well, that’s one of the great ironies of my career. It’s the computer. The prevalence of the computer and the spreadsheet has caused entrepreneurs in the last two or three years to develop pro forma projections of their businesses. They’re no longer written out by hand and really thought about, with the result that many people have no personal understanding of the numbers they’re projecting. Sometimes you find incredible market shares being achieved in just four years, simply because the numbers suggest it; or sometimes you find sales expenses projected at numbers far below what you’ll probably need to get the orders. Things like that fall out because the numbers are generated impersonally, and nobody thinks about the relationship between them and the structures that have to be in place before the numbers start coming in.

So for us the business plan is a bridge to communication. We’ve never invested in a company that achieved more than 70% of its plan. But that’s not such a great failing, in our view. We’re dealing with people who are supreme optimists. If they weren’t, they wouldn’t be starting companies, they’d be working in some nice, comfortable haven. They would not be doing the hardest thing in the world. So we’ve become less concerned about the completeness of the plan than we are about how the founders reached their conclusions — what factors they considered relevant, what assumptions they made, how realistically they viewed the competition, and so forth. These are things which, from our point of view, you can learn only by listening, not by reading.

INC.: What do you look for in terms of growth — the company that gets up and running at $25 million to $50 million a year, or one that goes to $200 million?

VALENTINE: I wish your question had more alternatives. But if I have to choose, my interest is always in people who can get the company from zero to $25 million or $50 million as quickly as possible.

INC.: Why is that?

VALENTINE: Well, the thing you have to keep in mind is that we invest in partnerships that last from 8 to 10 years, at the end of which time they terminate. This means that the real time frame of our growth expectations is about 5 years. How much can you legitimately expect a company to grow in 5 years? Not to $200 million or $300 million. Of course there are exceptions — Apple, for one — but their principal effect has been to confuse people about the real history of venture capital. Historically, the probability of a venture investor having even one Apple to his credit in 7 or 8 years is very low. If he were really good, out of 30 or 40 investments, he might make 2 or 3 Apples, but never 10. It’s absolutely unrealistic, in my opinion, to expect $200 million to $300 million in 5 years. On the other hand, it is perfectly reasonable to expect $25 million, $35 million, $50 million in that time, and that’s what we look for.

INC.: That certainly seems a lot more modest than what you were saying not long ago. It sounds as though you’ve radically scaled down your expectations from what they were a few years ago.

VALENTINE: Let me suggest that it’s you, the press, who have had to scale down your expectations, and you want to impute your disappointments to me. The fact that a company goes from zero to $50 million counts for a lot to me. Now it is true that during much of 1982 and all of 1983 there was a real pricing insanity in the venture field. Investment bankers, pension fund managers, a good many new players were racing around frantically to get their money employed in start-ups or mezzanine financing. This drastically shortened the amount of time available to study investment opportunities. We saw companies being funded very rapidly, so rapidly that we didn’t get a chance to participate. We were too slow. Recently, as a matter of fact, we were talking about one such company, wondering why we hadn’t made an investment in it. Well, the other investors were more agile. They moved before we could, in our iceberg fashion. As it happened, this company didn’t succeed. We had dodged the bullet. But the point is that the reason we were able to dodge the bullet is that we didn’t adjust our approach during that period of insanity. You know the old saw — keeping your head while all around you people are losing theirs. Well, I don’t want to suggest that all the companies we ducked in that period of frenzy were properly ducked. I suspect some were successful. But I don’t believe the venture investment community was ever conceptualized or designed to produce a dozen $500-million companies per year. History, at any rate, shows that it works best at delivering lots of small-niche companies, employing hundreds of people, doing brilliantly on $25 million to $50 million a year in revenues.

INC.: But isn’t there a danger in that sort of thinking? Aren’t you doing these companies a disservice by focusing on relatively short-term growth? Don’t you have some responsibility to make sure they have management capable of taking them past the $50-million mark?

VALENTINE: If you’re going to talk about responsibility, the real question is, to whom and to what constituency am I primarily responsible? I would say that our first responsibility is to our limited partners, who are mainly members of various pension plans in the United States. They’re the ones who own our companies, and when I think of responsibility, I think about those people, and the returns that they have signed up for and expect to be delivered.

INC.: Yes, but even so, we’ve seen loads of companies go to $30 million or $40 million in sales and then collapse, sometimes before going public. Don’t you at least have a responsibility to get managers who can keep companies solid over the 5-to-10-year period of your involvement?

VALENTINE: Of course. And after having made investments in perhaps 150 companies, we are inclined to believe that there is one set of management skills needed to start a company and another set needed to manage a bigger company. They are rarely resident in the same person.

INC.: So, even within a 5- or 10-year time frame, it’s almost inevitable that you’re going to have to make significant management changes.

VALENTINE: I’d say “management additions.” Sometimes the man who starts as president of a company is replaced by another member of the team when the company reaches a later stage of development. But with the exception of someone like [Tandem Computers Inc. president] Jim Treybig, it’s rare that a successful, driving entrepreneur becomes a successful executive capable of managing the assets and people of a $100-million or $500-million company. A great many entrepreneurs just cannot make that transition.

INC.: Of course, to listen to the entrepreneurs these days, the problem they’re having is getting people to invest at all. They refer to the venture capital community as “the valley of the maybes.” That certainly wasn’t the situation a year or two ago. Have you changed with the times, too?

VALENTINE: I don’t know. We don’t keep data; we don’t want our investment process dictated by the numbers. But looking back over the past 15 years, I would guess we’ve made substantially the same number of investments every year, with only a small range of differences. It’s not that we planned it that way; it just turned out that way. But the other key point is that we almost always invest in the early stages. We reconsider this virtually every time we meet to discuss strategy, but we’ve always found that for our purposes it made sense to continue to invest in the early phases of a company.

INC.: Why is that?

VALENTINE: Because in the company-building business, which is the business we perceive ourselves to be in, it’s easier to have an impact on the concept and personality of the company. This is difficult to do after the first financing. By then other people are influencing the company; its personality has been determined. We’ve seen companies that have been very badly influenced: for example, encouraged or tolerated in habits of irresponsible spending. We just find it easier — as in child-care — to form company attitudes toward spending and growth early on.

INC.: What’s your “letting go” point? When does it seem you can no longer impose your will on them?

VALENTINE: May I quibble with the question?

INC.: Quibble all you want.

VALENTINE: Thank you. We don’t view ourselves as “imposing our will” on a team starting a company. We don’t see ourselves as relating to companies in an adversarial way. We see ourselves as encouraging them, as a stimulator. The important thing we have to maintain in perspective is that other people are running the company. It is their company.On the tactical level we are at best a partner, but mostly a cheerleader. For example, during the wooing process — when the decisions are made whether to invest or not — we try to avoid having any of our ideas taken up as part of the concept of the company, lest we distort the entrepreneur’s or management’s view of what’s supposed to happen. We don’t make an investment decision based on our ability to enforce our will. That’s a repugnant concept. We want to make sure that the company is one where the entrepreneurs are having their ideas financed, and that they are passionately committed to those ideas.

INC.: So what exactly do you bring to the table — besides capital, I mean?

VALENTINE: I would say the main thing is what we call “intelligence equity” — experience the companies don’t have, contacts they don’t have, perspectives they don’t have. Basically, we give them the opportunity to move from the entrepreneurial stage to that of a larger, more stable company. Altos, for example, is now a company with around $103 million in annual sales. When we invested in it, it was comfortably successful, doing something like $12 million to $15 million a year. Altos was profitable, had money in the bank, had no debt, and was developing a fair amount of momentum. They really didn’t need our money, but they realized that they were entering a risky period, with a lot of unanswered questions — the more so because they didn’t know what the relevant questions were. So they were clever enough to want to associate with other people who could help them identify the questions as well as the answers — not just us, but lawyers, accounting firms, and so on.

INC.: All right, but let’s face it. Your experiences are heavily oriented toward the computer industry. How valuable are they in, say, a restaurant chain, not to mention any names?

VALENTINE: Well, it’s true that most of our expertise is in the computer area, and we probably have less to offer to companies outside the wide embrace of technology, especially companies in slower-growing industries. There are leverage skills we don’t have. We are probably better off staying out of those businesses.

INC.: But doesn’t the same reasoning apply in a technology-based industry like biotech? Don’t you think that microbiology demands profoundly different skills and perspectives than micro-electronics?

VALENTINE: A lot of fundamentally different skills and a lot of fundamentally similar skills.

INC.: For instance?

VALENTINE: Well, it’s true that many of us understand the world of bits and bytes, and relatively few have much experience in the world of microbiology, partly because this hasn’t been a business before. So, from one perspective, we’re operating at a disadvantage.

But it’s also true that microbiology is basically a tool for solving problems, just as a computer is a tool for solving problems. The challenge in both cases is to identify the problem and the best tool with which to solve it. From that perspective, we still have something to contribute to these companies, not so different from what we’ve contributed to computer companies. After all, we’ve seldom contributed anything to, say, the electronic architecture of a computer, or the kind of circuitry needed, or the speed or packaging. It’s rare for investors to get involved in that kind of detail.

INC.: Can you give us an example of the kind of “intelligence equity” you might provide to a biotech company, or a telecommunications company, for that matter?

VALENTINE: Sure. One thing about both those industries is that they tend to be very capital-intensive, so you have to find creative ways to raise money. We try to help companies do just that.

One example is a company called Equatorial Communications, which had to acquire $16 million worth of transponders on satellites in order to be operative as a communications company. That’s a lot of money, and the situation required a solution that would not be an equity disaster to the founders and early investors. I mean, if the company went to the market and tried to raise the money, they would have no equity left. They needed a way to finance assets that had never been financed before — the worth of which were therefore unknown — and they had to do this before the satellite was launched.

Well, through a combination of leasing and guarantees, modest amounts of equity were sold in order to control two transponders on Westar 4.The solution involved corporations, insurance companies, and banks — nontraditional financiers for a company like Equatorial. Frankly, nothing like it had ever been tried before because nothing like it had ever been needed. Since then, this kind of solution has also been used in many of the modestly successful bioengineering companies.

INC.: I suppose another solution would be to form one of these so called alliances, or corporate partnerships, with a larger company.

VALENTINE: Absolutely. That’s something we’ve done in the semiconductor industry — so that, for example, a company like LSI Logic can go into business and, through Johnson Controls, have the ability to purchase equipment worth $20 million for very little in the way of equity.

INC.: Do you think that this sort of alliance will become more common in the future, that people will be looking less to the equity market?

VALENTINE: I think corporate investors are a necessity in a capital-intensive business, where the equity leverage in a model venture deal can be easily lost. Obviously, straightforward debt doesn’t work. These companies don’t have the underlying equity from which to borrow from traditional sources. So corporate America has been one of the solutions. Insurance companies have been interested participants in these things, and some of the pharmaceutical companies as well.

INC.: Does this mean that small companies and large companies have more in common now than before?

VALENTINE: I view the small company as a vehicle for the individuals involved, but large companies can also benefit from their activities. Entrepreneurial companies are a stir to get big companies moving. What’s more, the people who work in big companies often own the small companies through their pension plans. One of our largest partners is General Electric, so the employees of GE benefit from our companies’ successes.

INC.: Let me change the subject and ask how all this affects you personally. You’ve had a string of spectacular successes as an investor, beginning with Apple. You’ve noted how unusual that is. Isn’t there a risk that they might go to your head? Don’t you ever get a slight Deity Complex?

VALENTINE: I suppose the correct way to answer that, in a magazine interview, is to say yes. It makes one appear humble. But the answer is no. I think I always understood why Apple worked, and that there was a great amount of luck involved, both for Apple and for our being investors in it. The publicity, if anything, reinforced this sense of perspective. Also, I have a teenage daughter whose role in life seems to be keeping my ego in check. At every opportunity she reminds me of my mortality.

INC.: Speaking of mortality, I take it that you don’t think we’re coming to the end of the Age of the Entrepreneur — despite all these stories of “Doom in Silicon Valley.”

VALENTINE: I think the thing that’s coming to an end is the reporting of it. Newspapers and magazines — and let’s throw in TV — are usually interested in short-term fads and “trends,” and since there are many more media than there are fads, the latter tend to get overreported. The fact that the media are now writing about “Doom in Silicon Valley” means to me only that they are getting tired of writing about “Boom in Silicon Valley.” For the public, maybe things will come back into some sort of historical perspective. Entrepreneurism is not the solution to all the economic problems of the country or the world. No one ever conceived it to be — except the press.

INC.: So in a way the doom-talk might be good.

VALENTINE: It might be good if fewer company presidents and venture capitalists have to talk with reporters. More time will be spent in creating new companies.

Venture Capital returns remain very difficult to analyze mostly because access to data is tough. There are some web sites such as venturereturns but more interesting are the official reports of endowment funds such as the University of California, Washington State or Castle in Europe. Most venture capital firms do not publish any data.

In chapter 5 of “Start-Up”, I have published the following table:

Now let me publish them for some specific funds:

I had not mentioned before KP and Sequoia first funds which is something I plan to work on in the next weeks. Anyone with data would interest me! Late last year I was lucky enough to “see” KP first fund’s portfolio performance in more details which I will describe in my next post…