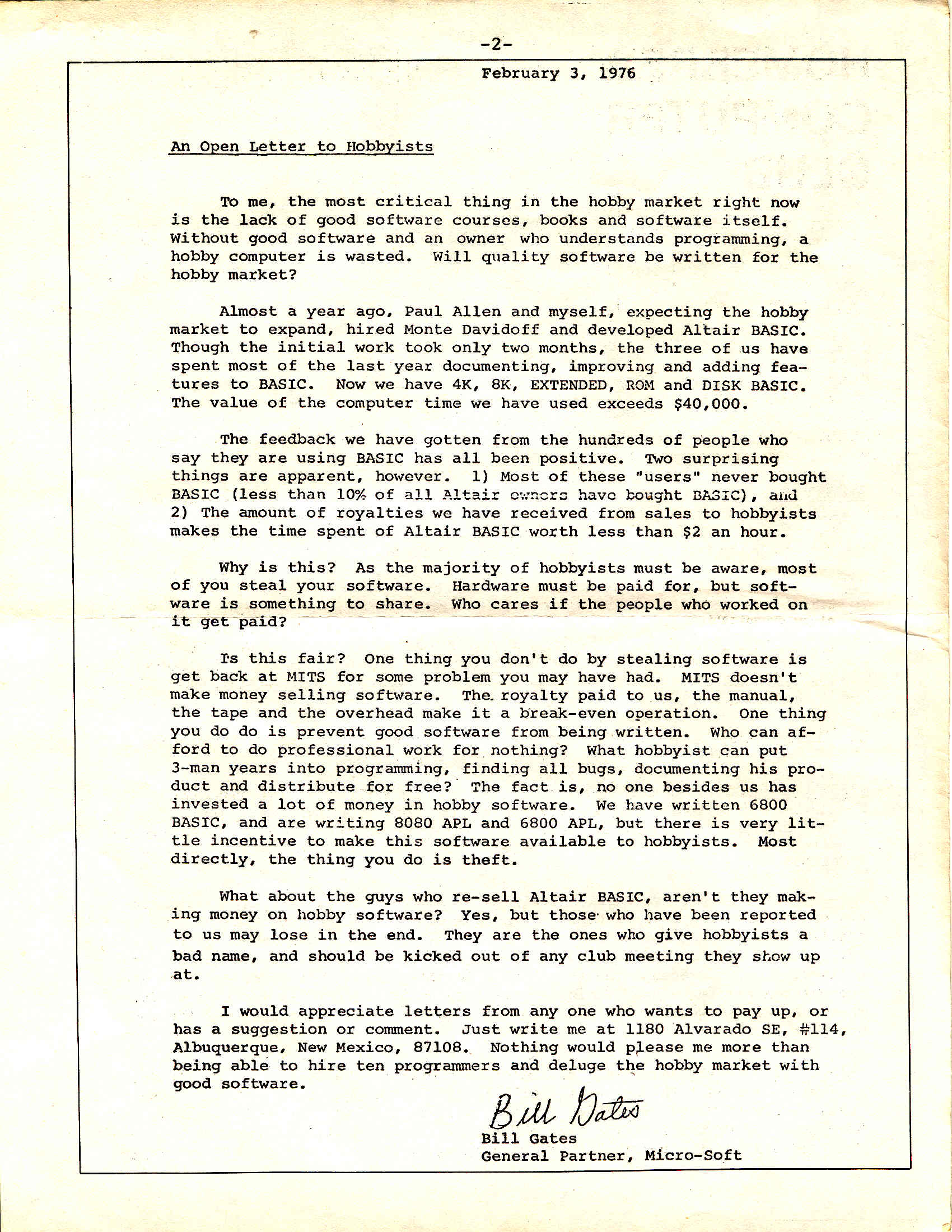

Gates complained to the members of the Homebrew Computer Club about this: “Two surprising things are apparent, however, 1) Most of these “users” never bought BASIC (less than 10% of all Altair owners have bought BASIC), and 2) The amount of royalties we have received from sales to hobbyists makes the time spent on Altair BASIC worth less than $2 an hour. Why is this? As the majority of hobbyists must be aware, most of you steal your software. Hardware must be paid for, but software is something to share. Who cares if the people who worked on it get paid? Is this fair? One thing you don’t do by stealing software is get back at MITS for some problem you may have had. MITS doesn’t make money selling software. […] The thing you do is theft. I would appreciate anyone who wants to pay.” [Page 342 and http://www.digibarn.com/collections/newsletters/homebrew/V2_01/gatesletter.html]

But Isaacson nuances : “Still there was a certain audacity to the letter. Gates was, after all, a serial stealer of computer time, and he had manipulated passwords to hack into accounts from eighth grade through his sophomore year at Harvard. Indeed, when he claimed in his letter that he and Allen had used more than $40,000 worth of computer time to make BASIC, he omitted the fact he had never actually paid for that time. […] Also, though Gates did not appreciate it at the time, the widespread pirating of Microsoft BASIC helped his fledgling company in the long run. By spending so fast, Microsoft BASIC became a standard, and other computer makers had to license it.” [Page 343]

And what about Jobs and Wozniak? Everyone knows about how phone phreaks had created a device that emitted just the right tone chirps to fool the Bell System and cadge free long-distance calls. […] “I have never designed a circuit I was prouder of. I still think it was incredible”. They tested it by calling the Vatican, with Wozniak pretending to be Henry Kissinger needing to speak to the pope, it took a while but the officials at the Vatican finally realized it was a prank before they woke up the pontiff. [Page 346]

Gates, Jobs and the GUI

And the greatest robbery may have been the GUI – Graphical User Interface. But who stole? Later when he was challenged about pilfering Xerox’s ideas, Jobs quoted Picasso: “Good artists copy, great artists steal. And we have been always shameless about stealing great ideas. They were copier-heads who had no clue about what a computer could do.” [Page 365]

However when Microsoft copied Apple for Windows, it was a different story… “In the early 1980s, before the introduction of the Macintosh, Microsoft had a good relationship with Apple. In fact on the day that IBM launched its PC in August 1981, Gates was visiting Jobs at Apple, which was a regular occurrence since Microsoft was making most of its revenue writing software for the Apple II. Gates was still the supplicant in the relationship. In 1981, Apple had $334 million in revenue, compared to Microsoft’s $15 million. […] Jobs had one major worry about Microsoft: he didn’t want it to copy the graphical user interface. […] His fear that Gates would steal the idea was somewhat ironic, since Jobs himself had filched the concept from Xerox.” [Pages 366-67]

Things would go worse… “Well, Steve, I think there’s more than one way of looking at it. I think it’s more like we both had this rich neighbor named Xerox and I broke into his house to steal the TV set and I found out that you had already stolen it”. [Page 368]

Stallman, Torvalds, free- and open-source

There would be other oppositions. The hacker corps that grew up around GNU [Stallman’s free software] and Linux [Torvalds’ open software] showed that emotional incentives, beyond financial rewards, can motivate voluntary collaboration. “Money is not the greatest of motivations,” Torvalds said. “Folks do their best work when they are driven by passion. When they are having fun. This is as true for playwrights and sculptors and entrepreneurs as it is for software engineers.” There is also, intended or not, some self-interest involved. “Hackers are also motivated, in large part, by the esteem they can gain in the eyes of their peers, improve their reputation, elevate their social status. Open source development gives programmers the chance.” Gates “Letter to Hobbysts”, complaining about the unauthorized sharing of Microsoft BASIC, asked in a chiding way, “who can afford to do professional work for nothing?”. Torvalds found that an odd outlook. He and Gates were from two very different cultures, the communist-tinged radical academia of Helsinki versus the corporate elite of Seattle. Gates may have ended up with the bigger house, but Torvalds reaped anti-establishment adulation. “Journalists seemed to love the fact that, while Gates lived a high-tech lakeside mansion, I was tripping over my daughter’s playthings in a three-bedroom ranch house with bad plumbing in boring Santa Clara,” he said with ironic self-awareness. “And that I drove a boring Pontiac. And answered my own phone. Who wouldn’t love me?” [Pages 378-79]

Which does not make open a friend of free. The disputes went beyond mere substance and became, in some ways, ideological. Stallman was possessed by a moral clarity and unyielding aura, and he lamented that “anyone encouraging idealism today faces a great obstacle: the prevailing ideology encourages people to dismiss idealism as ‘impractical'”. Torvalds, on the contrary, was unabashedly practical, like an engineer. “I led the pragmatists,” he said. “I have always thought that idealistic people are interesting, but kind of boring and scary.” “Torvalds admitted to “not exactly being a huge fan” of Stallman, explaining, “I don’t like single-issue people, nor do I think that people who turn the world into black and white are very nice or ultimately very useful. The fact is, there aren’t just two sides to any issue, there’s almost always a range of responses, and ‘it depends’ is almost always the right answer to any big question. He also believed it should be permissible to make money from open-source software. “Open-source is about letting everybody play. Why should business, which fuels so much of society’s technological advancement, be excluded?”. Software may want to be free, but the people who write it may want to feed their kids and reward their investors. [Page 380]

Innovation is about business models – the Atari case

Innovation in (Silicon) Valley: after the chip, innovation saw the arrival of games, software and the Internet “As they were working on the first Computer Space consoles, Bushnell heard that he had competition. A Stanford grad named Bill Pitts and his buddy Hugh Tuck from California polytechnic had become addicted to Spacewar, and they decided to use a PDP-11 minicomputer to turn it into an arcade game. […] Bushnell was contemptuous of their plan to spend $20,000 on equipment, including a PDP-11 that would be in another room and connected by yards of cable to the console, and then charge ten cents a game. “I was surprised at how clueless they were about the business model,” he said. “Surprised and relieved. As soon as I saw what they were doing, I knew they’d be no competition”.

Galaxy Game by Pitts and Tuck debuted at Stanford’s Tresidder student union coffeehouse in the fall of 1971. Students gathered around each night like cultists in front of a shrine. But no matter how many lined up their coins to play, there was no way the machine could pay for itself, and the venture eventually folded. “Hugh and I were both engineers and we didn’t pay attention to business issues at all,” conceded Pitts. Innovation can be sparked by engineering talent, but it must be combined with business skills to set the world afire.

Bushnell was able to produce his game, Computer Space, for only $1,000. It made its debut a few weeks after Galaxy Game at the Dutch Goose bar in Menlo Park near Palo Alto and went on to sell a respectful 1,500 unites. Bushnell was the consummate entrepreneur: inventive, good at engineering, and savvy about business and consumer demand. He was also a great salesman. […] When he arrived back at Atari’s little rented office in Santa Clara, he described the game to Alcorn [Atari’s co-founder], sketched out some circuits, and asked him to build the arcade version of it. He told Acorn he had signed a contract with GE to make the game, which was untrue. Like many entrepreneurs, Bushnell had no shame about distorting reality in order to motivate people.” [Pages 209-211]

“Innovation requires having three things: a great idea, the engineering talent to execute it, and the business savvy (plus deal-making moxie) to turn it into a successful product. Nolan Bushnell scored a trifecta when he was twenty-nine, which is why he, rather than Bill Pitts, Hugh Truck, Bill Nutting, or Ralph Baer, goes down in history as the innovator who launched the video game industry.” [page 215]

You may also so listen to Bushnell directly. This is Something Ventured and the Atari story begins at 30’07” until 36’35” (you may go on Youtube directly for the right timing).

The debate about intelligence of machines

Chapter 7 is about the beginnings of the Internet. Isaacson adddresses a topic which has come back has a hot debate these days: will machines and the computer in particular replace humans, with or despite their intelligence, creativity and innovation capabilities? I feel close to Isaacson whom I quote from page 226: “Licklider sided with Norbert Wiener, whose theory of cybernetics was based on humans and machines working closely together, rather than with their MIT colleagues Marvin Minsky and John mcCarthy, whose quest for artificial intelligence involved creating machines that could learn on their own and replace human cognition. As Licklider explained, the sensible goal was to create an environment in which humans and machines “cooperate in making decisions.” In other words,they would augment each other. “Men will set the goals, formulate the hypotheses, determine the criteria, and perform the evaluations. Computing machines will do the routinizable work that must be done to prepare the way for insights and decisions in technical and scientific thinking.”

The Innovator’s dilemma

In the same chapter which tries to describe who were the inventors (more than the innovators) in the case of the Internet – J.C.R. Licklider, Bob Taylor, Larry Roberts, Paul Baran, Donald Davies, or even Leonard Kleinrock – and why it was invented – an unclear motivation between the military objective of protecting communications in case of a nuclear attack or the civilian one of helping researchers in sharing resources – Isaacson shows once again the challenge of convincing established players.

Baran then collided with one of the realities of innovation, which was that entrenched bureaucracies are resistant to change. […] He tried to convince AT&T to supplement its circuit-switched voice network with a packet-switched data network. “they fought it tooth and nail,” he recalled. “They tried all sorts of things to stop it.” [AT&T would go as far as organizing a series of seminars that would involve 94 speakers] “Now do you see why packet switching wouldn’t work?” Baran simply replied, “No”. Once again, AT&T was stymied by the innovator’s dilemma. It balked at considering a whole new type of data network because it was so invested in traditional circuits. [Pages 240-41]

[Davies] came up with a good old English word for them: packets. In trying to convince the general Post office to adopt the system, Davies ran into the same problem that Baran had knocking at the door of AT&T. But they both found a fan in Washington. Larry Roberts not only embraced their ideas; he also adopted the word packet.

The entrepreneur is a rebel (who loves power)

One hard-core hacker, Steve Dompier, told of going down to Alburquerque in person to pry loose a machine from MITS, which was having trouble fulfilling orders. By the time of the third Homebrew meeting in April 1975, he had made an amusing discovery. He had written a program to sort numbers, and while he was running it, he was listening to a weather broadcast on a low-frequency transistor radio. “The radio started going zip-zzziiip-ZZZIIIPP at different pitches », and Dompier said to himself, “Well, what do you know ! My first peripheral device!” So he experimented. “I tried some other programs to see what they sounded like, and after about eight hours of messing around, I had a program that could produce musical tones and actually make music”. [Page 310]

“Dompier published his musical program in the next issue of the People’s Computer Company, which led to a historically noteworthy response from a mystified reader. “Steven Dompier has an article about the musical program that he wrote for the Altair in the People’s Computer Company,” Bill Gates, a Harvard student on leave writing software for MITS in Albuquerque, wrote in the Altair newsletter. “The article gives a listing of his program and the musical data for ‘The Fool on the Hill’ and ‘Daisy.’ He doesn’t explain why it works and I don’t see why. Does anyone know?” the simple answer was that the computer , as it ran the programs, produced frequency interference that could be controlled by the timing loops and picked up as tone pulses by an AM radio.

By the time his query was published, Gates had been thrown into a more fundamental dispute with the Homebrew Computer Club. It became archetypal of the clash between the commercial ethic that believed in keeping information proprietary, represented by Gates [and Jobs], and the hacker ethic of sharing information freely, represented by the Homebrew crowd [and Wozniak].” [Page 311]

Isaacson, through his description of Gates and Jobs, explains what is an entrepreneur.

“Yes, Mom, I’m thinking,” he replied. “Have you ever tried thinking?” [P.314] Gates was a serial obsessor. […] he had a confrontational style [… and he] would escalate the insult to be “the stupidest thing I’ve ever heard.” [P.317] Gates pulled a power play that would define his future relationship with Allen. As Gates describes it, “That’s when I say ‘Okay, but I’m going to be in charge. And I’ll get used to being in charge, and it’ll be hard to deal with me from now on unless I’m in charge. If you put me in charge, I’m in charge of this and anything else we do.’ ” [P.323] Like many innovators, Gates was rebellious just for the hell of it. [P.331] “An innovator is probably a fanatic, somebody who loves what they do, works day and night, may ignore normal things to some degree and therefore be viewed as a bit imbalanced. […] Gates was also a rebel with little respect for authority, another trait of innovators. [P.338]

Allen assumed that his partnership with Gates would be fifty-fifty. […] but Gates had insisted on being in charge. “It’s not right for you to get half. […] I think it should be sixty-forty.” […] Worse yet, Gates insisted on revisiting the split two years later. “I deserve more than 60 percent.” His new demand was that the split be 64-36. Born with a risk-taking gene, Gates would cut loose late at night by driving at terrifying speeds up the mountain roads. “I decided it was his way of letting off steam.” Allen said. [P.339]

Gates arrested for speeding, 1977. [P.312]

“There is something indefinable in an entrepreneur, and I saw that in Steve,“ Bushnell recalled. “He was interested not just in engineering, but also in the business aspects. I taught him that if you act like you can do something, then it will work. I told him, pretend to be completely in control and people will assume that you are.” [P.348]

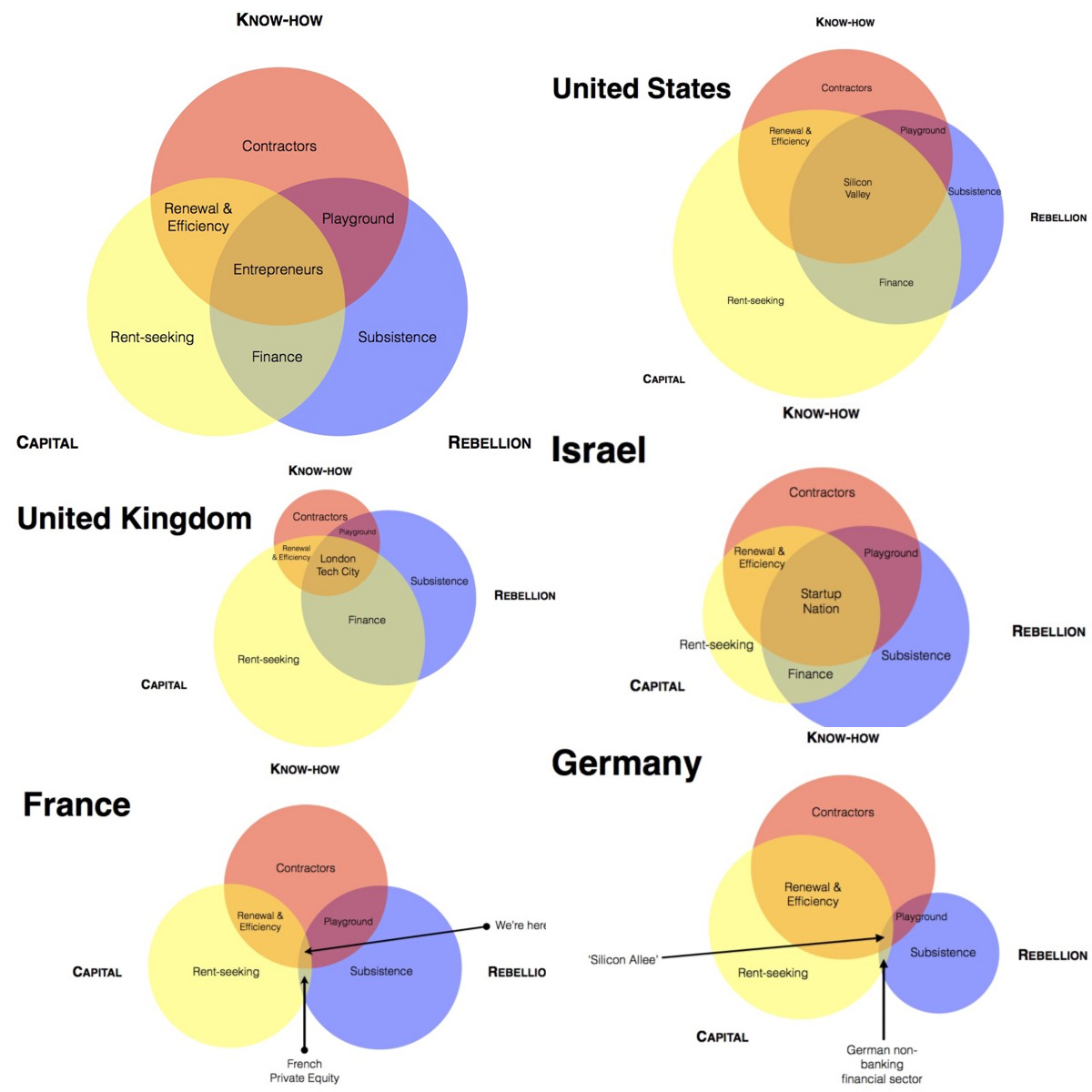

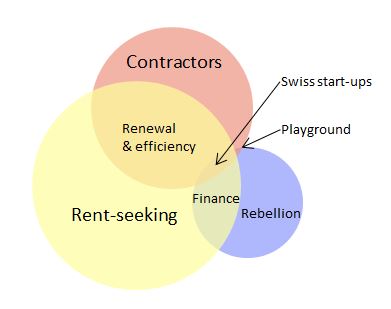

The concept of the entrepreneur as a rebel is not new. In 2004, Pitch Johnson, one of the earliest VC in Silicon Valley claimed “Entrepreneurs are the revolutionaries of our time.” Freeman Dyson has written “The Scientist as a Rebel“. And you should read Nicolas Colin’s analysis of entrepreneurial ecosystems: Capital + know-how + rebellion = entrepreneurial economy. Yes rebels who loves power…

in a nutshell, the entrepreneurial ecosystems need 3 ingredients – I quote: – capital: by definition, no new business can be launched without money and relevant infrastructures (which consist of capital tied up in tangible assets); – know-how: you need engineers, developers, designers, salespeople: all those whose skills are necessary for launching and growing innovative businesses; – rebellion: an entrepreneur always challenges the status quo. If they wanted to play by the book, they would innovate within big, established companies, where they would be better paid and would have access to more resources.

This reminds me of two “recipes” I often mention. First the “5 needed ingredients of tech. clusters”

1. Universities and research centers of a very high caliber;

2. An industry of venture capital (i.e. financial institutions and private investors);

3. Experienced professionals in high tech;

4. Service providers such as lawyers, head hunters, public relations and marketing specialists, auditors, etc.

5. Last but not least, an intangible yet critical component: a pioneering spirit which encourages an entrepreneurial culture.

in “Understanding Silicon Valley, the Anatomy of an Entrepreneurial Region”, by M. Kenney, more precisely in chapter: “A Flexible Recycling” by S. Evans and H. Bahrami

Second, Paul Graham in How to be Silicon Valley?“Few startups happen in Miami, for example, because although it’s full of rich people, it has few nerds. It’s not the kind of place nerds like. Whereas Pittsburgh has the opposite problem: plenty of nerds, but no rich people.” He also added about failed ecosystems: “I read occasionally about attempts to set up “technology parks” in other places, as if the active ingredient of Silicon Valley were the office space. An article about Sophia Antipolis bragged that companies there included Cisco, Compaq, IBM, NCR, and Nortel. Don’t the French realize these aren’t startups?”

Many toxic friends of entrepreneurial ecosystems have not understood this. But for those who have understood, building lively ecosystems remains a real challenge: bringing the rebellion, the culture, diminishing the fear of risk taking without stigmatizing (not rewarding– here I disagree with Colin) failure remains highly challenging whereas finding know-how and capital is not easy but feasible with some hard work…

Finally, I copy his diagrams which show ideal and less ideal combinations of capital, know-how and rebellion, adding my exercise for Switzerland.

Switzerland is probably 80% Germany and 20% France…

(A short addition on Oct 29, 2015) – The best description of Switzerland was given by Orson Welles. It explains a lot of things…

“In Italy, for thirty years under the Borgias, they had warfare, terror, murder and bloodshed, but they produced Michelangelo, Leonardo da Vinci and the Renaissance. In Switzerland, they had brotherly love, they had five hundred years of democracy and peace – and what did that produce? The cuckoo clock.” in The Third Man, said by Holly Martins to Harry Lime.

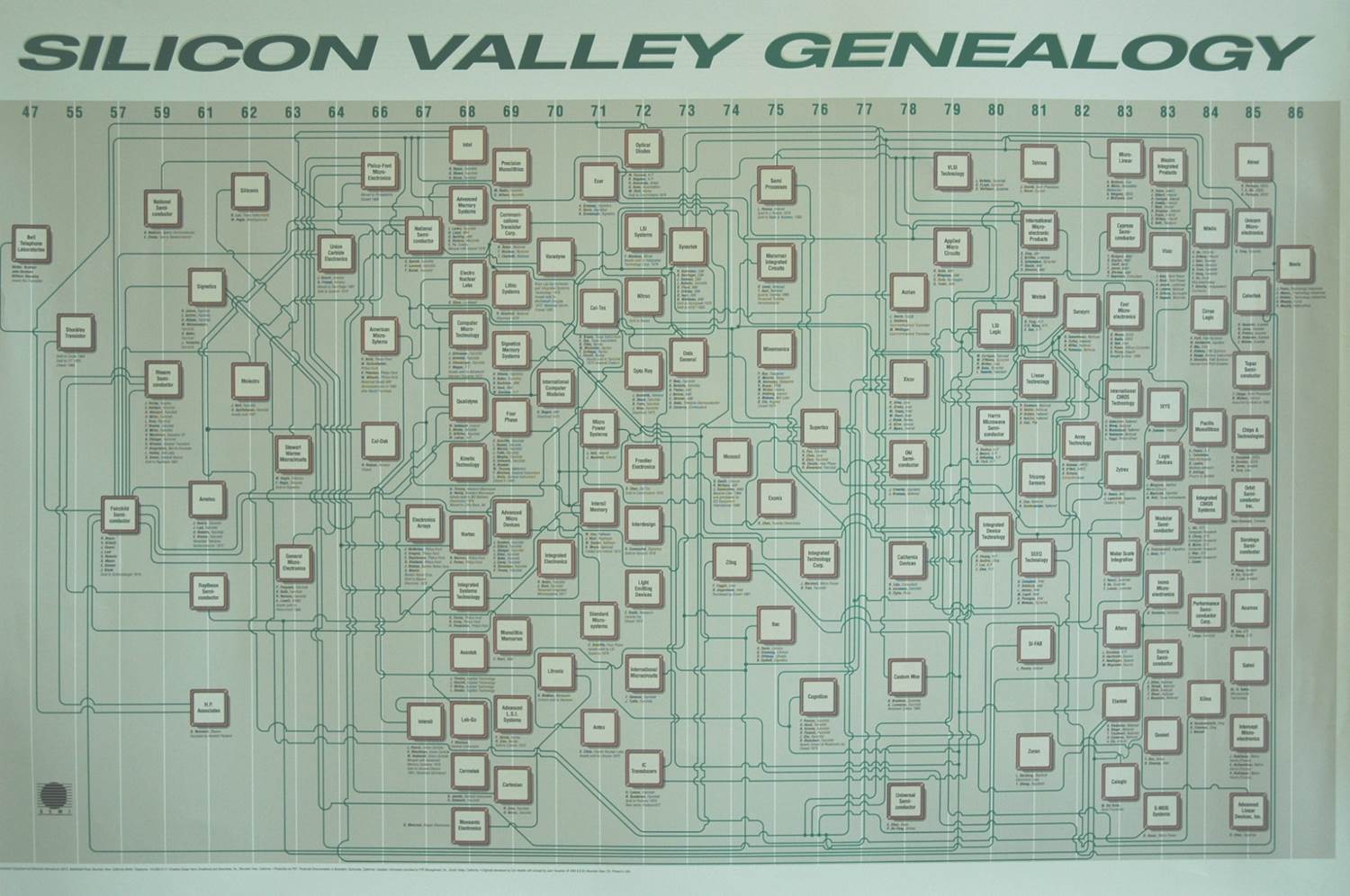

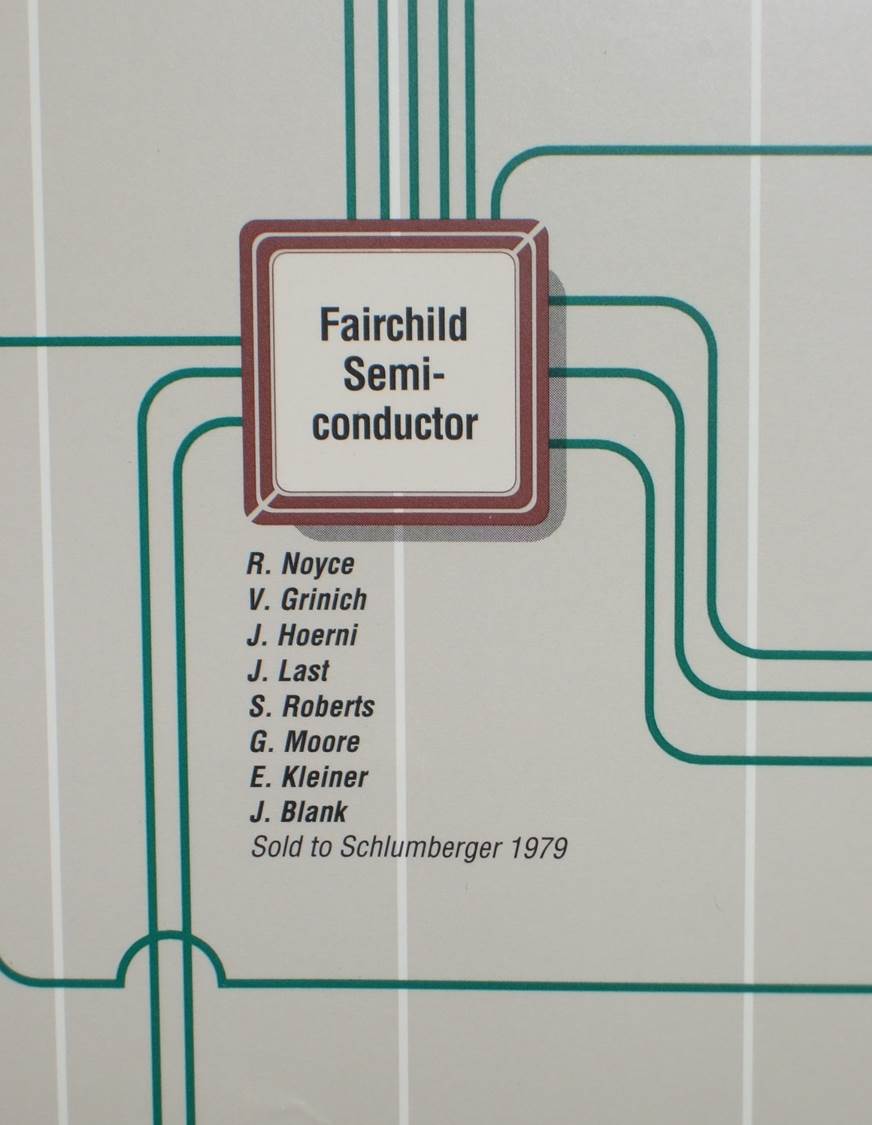

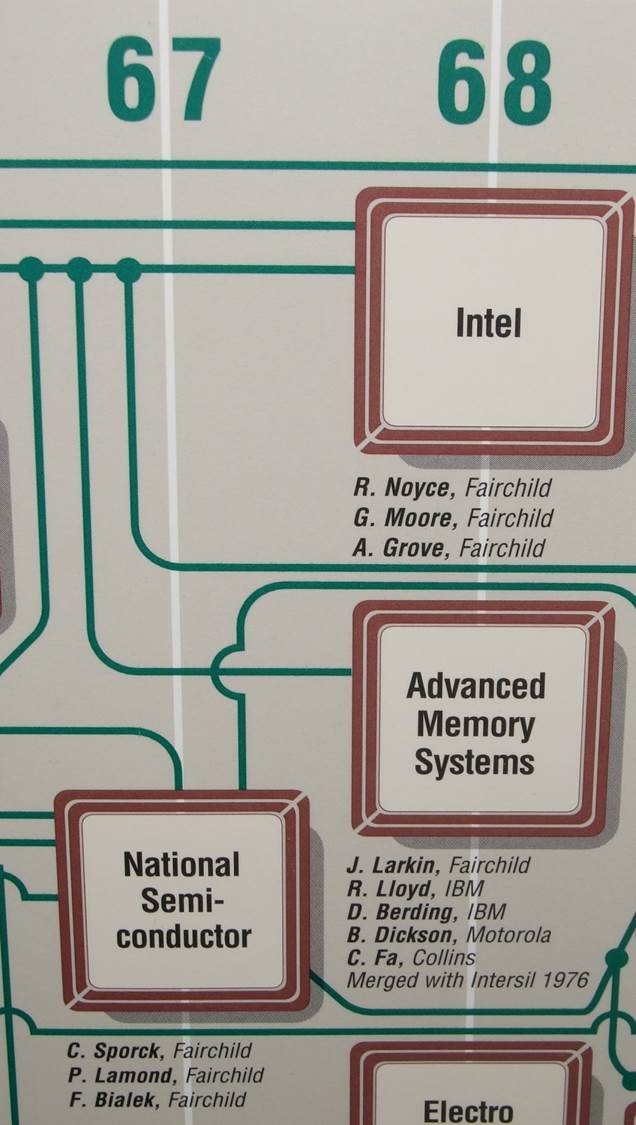

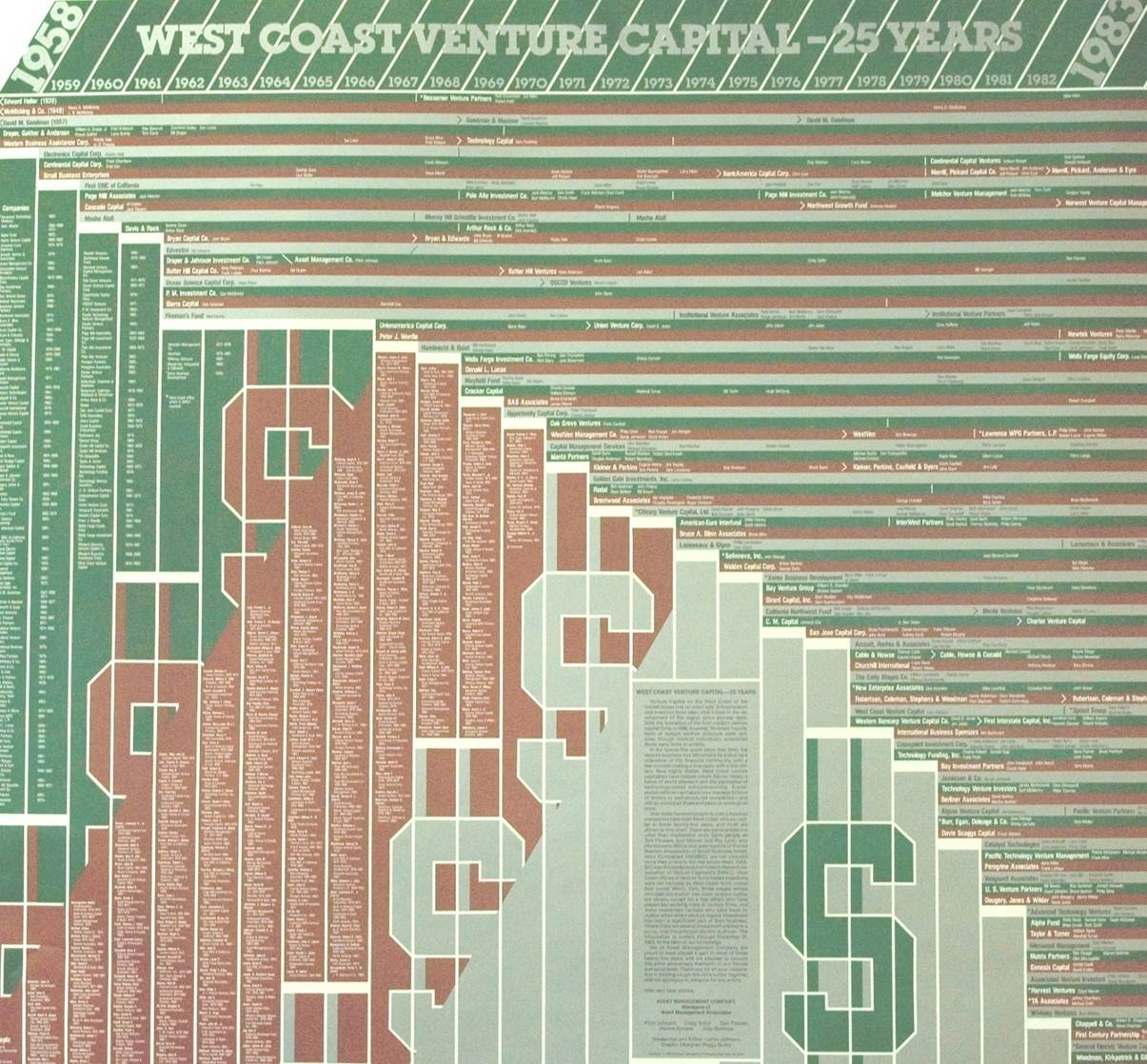

What I am reading now following my recent post The Complexity and Beauty of Innovation according to Walter Isaacson is probably much better known: Innovation in Silicon Valley at the time of Silicon – Fairchild, Intel and the other Fairchildren. I have my own archive, nice posters from those days, one about the start-up / entrepreneur genealogy, with a zoom on Fairchild and one on Intel and one about the investor genealogy

Entrepreneurs…

“There were internal problems in Palo Alto. Engineers began defecting, thus seeding the valley with what became known as Fairchildren: companies that sprouted from spores emanating from Fairchild.” [Page 184] “The valley’s main artery, a bustling highway named El Camino Real, was once the royal road that connected California’s twenty-one mission churches. By the early 1970s – thanks to Hewlett-Packard, Fred Terman’s Stanford Industrial Park, William Shockley, Fairchild and its Fairchildren – it connected a bustling corridor of tech companies. In 1971, the region got a new moniker. Don Hoefler, a columnist for the weekly trade paper Electronic News, began writing s series of columns entitled “Silicon Valley USA,” and the name stuck.” [Page 198]

… and Investors

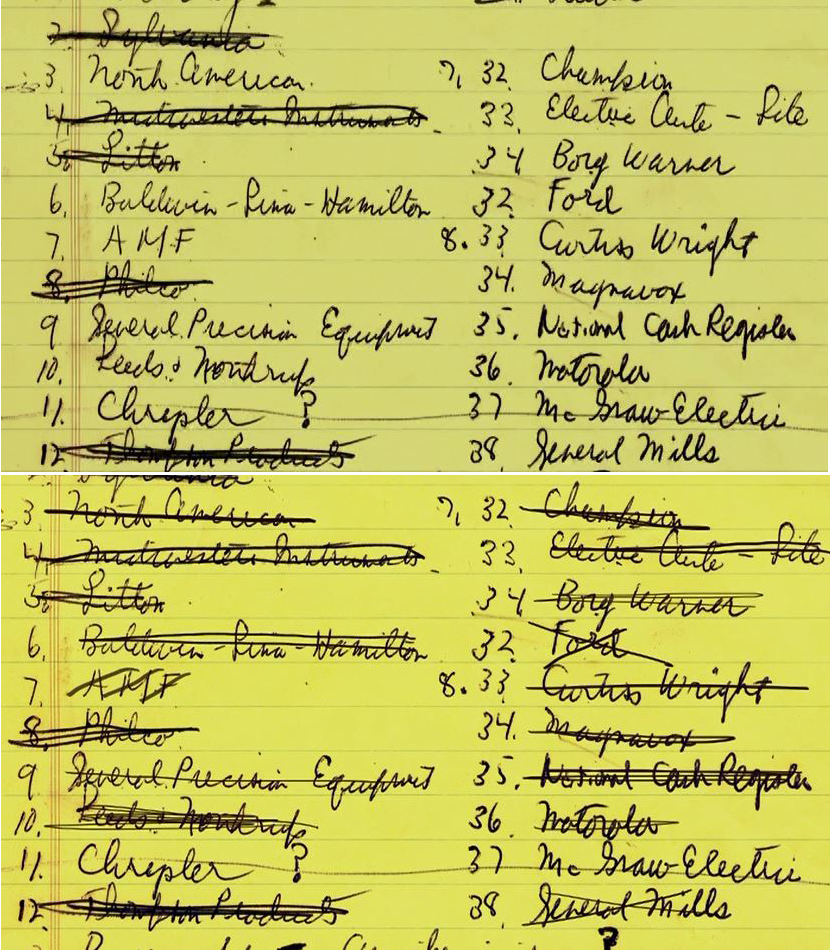

“In the eleven years since he had assembled the deal for the traitorous eight to form Fairchild Semiconductors, Arthur Rock had helped to build something that was destined to be almost as important to the digital age as the microchip: venture capital.” [Page 185] “When he had sought a home for the traitorous eight in 1957, he pulled out a single piece of legal-pad paper, wrote a numbered list of names, and methodically phoned each one, crossing off the names as he went down the list. Eleven years later, he took another sheet of paper and listed people who would be invited to invest and how many of the 500’000 shares available at $5 apiece he would offer to each. […] It took them less than two days to raise the money. […] All I had to tell people was that it was Noyce and Moore. They didn’t need to know much else.” [Pages 187-88]

The Intel culture

“There arose at Intel an innovation that had almost as much of an impact on the digital age as any [other]. It was the invention of a corporate culture and management style that was the antithesis of the hierarchical organization of East Coast companies.” [[Page 189] “The Intel culture, which would permeate the culture of Silicon Valley, was a product of all three men. [Noyce, Moore and Grove]. […] It was devoid of the trappings of hierarchy. There were no reserved parking places. Everyone including Noyce and Moore, worked in similar cubicles. […] “There were no privileges anywhere” recalled Ann Bowers, who was the personnel director and later married Noyce, [she would then become Steve Jobs’ first director of human resources] “we started a form of company culture that was completely different than anything that had been before. It was a culture of meritocracy.

It was also a culture of innovation. Noyce had a theory that he developed after bridling the rigid hierarchy at Philco. The more open and unstructured a workplace, he believed, the faster new ideas would be sparked, disseminated, refined and applied.” [Pages 192-193]

In his introductory article about the course he is giving at Stanford, Reid Hoffman convincingly explains why Silicon Valley still leads in high-tech innovation: Silicon Valley is no longer unique in its ability to launch startups. Today, many parts of the world are rich in all of the necessary ingredients. There are bright young technical graduates from universities around the world. Venture capital has gone global. And, technology companies have R&D centers in many areas of the world. There has even been a global expansion of some of the more subtle elements such as a culture acceptance of the potential failure of bold ventures. And, the belief in entrepreneurship is spreading everywhere in the world — creating a receptive culture in many cities. So, why does Silicon Valley continue to produce so many industry-transforming companies? The secret has moved past startups to scaleups.

The Innovators by Walter Isaacson is a great book because of its balanced description of the role of geniuses or disruptive innovators as much as of teamwork in incremental innovation. “The tale of their teamwork is important because we don’t often focus on how central their skill is to innovation. […] But we have far fewer tales of collaborative creativity, which is actually more important in understanding how today’s technology evolution was fashioned.” [Page 1] He also goes deeper: “I also explore the social and cultural forces that provide the atmosphere for innovation. For the birth of the digital age, this included a research ecosystem that was nurtured by the government spending and managed by a military-industrial collaboration. Intersecting with that was a loose alliance of community organizers, communal-minded hippies, do-it yourself hobbyists, and homebrew hackers, most of whom were suspicious of centralized authority.” [Page 2] ”Finally, I was struck by how the truest creativity of the digital age came from those who were able to connect the arts and sciences.” [Page 5]

The computer

I was a little more cautious with chapter 2 as I have the feeling that the story of Ada Lovelace and Charles Babbage is well known. I may be wrong. But chapter 3 about the early days of the computer was mostly unknown to me. Who invented the computer? Probably many different people in different locations in the US, the UK and Germany, around WWII. “How did they develop this idea at the same time when war kept their two teams isolated? The answer is partly that advances in technology and theory made the moment ripe. Along with many innovators, Zuse and Stibitz were familiar with the use of relays in phone circuits, and it made sense to tie that to binary operations of math and logic. Likewise, Shannon, who was also very familiar with phone circuits, would be able to perform the logical tasks of Boolean algebra. The idea that digital circuits would be the key to computing was quickly becoming clear to researchers almost everywhere, even in isolated places like central Iowa.” [Page 54]

There would be a patent fight I did not know about. Read pages 82-84. You can also read the following on Wikipedia: “On June 26, 1947, J. Presper Eckert and John Mauchly were the first to file for patent on a digital computing device (ENIAC), much to the surprise of Atanasoff. The ABC [Atanasoff–Berry Computer] had been examined by John Mauchly in June 1941, and Isaac Auerbach, a former student of Mauchly’s, alleged that it influenced his later work on ENIAC, although Mauchly denied this. The ENIAC patent did not issue until 1964, and by 1967 Honeywell sued Sperry Rand in an attempt to break the ENIAC patents, arguing the ABC constituted prior art. The United States District Court for the District of Minnesota released its judgement on October 19, 1973, finding in Honeywell v. Sperry Rand that the ENIAC patent was a derivative of John Atanasoff’s invention.” [The trial had begun in June 1971 and the ENIAC patent was therefore made invalid]

I also liked his short comment about complementary skills. “Eckert and Mauchly served as counterbalances for each other, which made them typical of so many digital-age leadership duos. Eckert drove people with a passion for precision; Mauchly tended to calm them and make them feel loved.” [Pages 74-75]

Women in Technology and Science

It is in chapter 4 about Programming that Isaacson addresses the role of women. “[Grace Hopper] education wasn’t as unusual as you might think. She was the eleventh woman to get a math doctorate from Yale, the first being in 1895. It was not at all uncommon for a woman, especially from a successful family, to get a doctorate in math in the 1930s. In fact, it was more common than it would be a generation later. The number of American women who got doctorates in math during the 1930s was 133, which was 15 percent of the total number of American math doctorates. During the decade of the 1950s, only 106 American women got math doctorates, which was a mere 4 percent of the total. (By the first decade of the 2000 things had more than rebounded and there were 1,600 women who got math doctorates, 30 percent of the total.)” [Page 88]

Not surprisingly, in the early days of computer development, men worked more in hardware whereas women would be in software. “All the engineers who built ENIAC’s hardware were men. Less heralded by history was a group of women, six in particular, who turned out to be almost as important in the development of modern computing.” [Page 95] “Shortly before she died in 2011, Jean Jennings Bartik reflected proudly on the fact that all the programmers who created the first general-purpose computer were women. « Despite our coming of age in an era when women’s career opportunities were generally quite confined, we helped initiate the era of the computer. » It happened because a lot of women back then had studied math and their skills were in demand. There was also an irony involved: the boys with their toys thought that assembling the hardware was the most important task, and thus a man’s job. « American science and engineering was even more sexist than it is today, » Jennings said. « If the ENIAC’s administration had known how crucial programming would be to the functioning of the electronic computer and how complex it would prove to be, they might have been more hesitant to give such an important role to women.” [Pages 99-100]

The sources of innovation

“Hopper’s historical sections focused on personalities. In doing so, her book emphasized the role of individuals. In contrast, shortly after Hopper’s book was completed, the executives at IBM commissioned their own history of the Mark I that gave primary credit to the IBM teams in Endicott, New York, who had constructed the machine. “IBM interests were best served by replacing individual history with organizational history,” the historian Kurt Beyer wrote in a study of Hopper. “The locus of technological innovation, according to IBM was the corporation. The myth of the lone radical inventor working in the laboratory or basement was replaced by the reality of teams of faceless organizational engineers contributing incremental advancements.” In the IBM version of history, the Mark I contained a long list of small innovations, such as the ratchet-type counter and the double-checked card feed, that IBM’s book attributed to a bevy of little-known engineers who worked collaboratively in Endicott.

The difference between Hopper’s version of history and IBM’s ran deeper than a dispute over who should get the most credit. It showed fundamentally contrasting outlooks on the history of innovations. Some studies of technology and science emphasize, as Hopper did, the role of creative inventors who make innovative leaps. Other studies emphasize the role of teams and institutions, such as the collaborative work done at Bell Labs and IBM’s Endicott facility. This latter approach tries to show that what may seem like creative leaps – the Eureka moment – are actually the result of an evolutionary process that occurs when ideas, concepts, technologies, and engineering methods ripen together. Neither way of looking at technological advancement is, on its oqn, completely satisfying. Most of the great innovations of the digital age sprang from an interplay of creative individuals (Mauchly, Turing, von Neumann, Aiken) with teams that knew how to implement their ideas.” [Pages 91-92]

Google about Disruptive and Incremental Innovation

This is very similar to what I read about Google and posted recently in The Importance and Difficulty of Culture in Start-ups: Google again…: “To us, innovation entails both the production and implementation of novel and useful ideas. Since “novel” is often just a fancy synonym for “new”, we should also clarify that for something to be innovative, it needs to offer new functionality, but it also has to be surprising. If your customers are asking for it, you aren’t being innovative when you give them what they want; you are just being responsive. That’s a good thing, but it’s not innovative. Finally “useful” is a rather underwhelming adjective to describe that innovation hottie, so let’s add an adverb and make it radically useful, Voilà: For something to be innovative, it needs to be new, surprising, and radically useful.” […] “But Google also releases over five hundred improvements to its search every year. Is that innovative? Or incremental? They are new and surprising, for sure, but while each one of them, by itself is useful, it may be a stretch to call it radically useful. Put them all together, though, and they are. […] This more inclusive definition – innovation isn’t just about the really new, really big things – matters because it affords everyone the opportunity to innovate, rather than keeping it to the exclusive realm of these few people in that off-campus building [Google[x]] whose job is to innovate.” [How Google Works – Page 206]

I was in Eindhoven today for the great EVP program (20 young entrepreneurs from 4 European technical universities spent two weeks on four campuses developing their projects). I had two inspiring moments: 1st the mayor of Eindhoven had a great speech about the importance of innovation and entrepreneurship. 2nd we had a meeting of 20+ people debating about how to foster entrepreneurship in universities.

Eindhoven’s efforts for entrepreneurship and innovation

The mayor of Eindhoven, Rob van Gijzel, explained that Philips had been nearly everything for Eindhoven for decades (jobs of course, schools, hospitals, PSV…) but a lot of the jobs have been delocalized, and Philips has struggled. He mentioned that the life expectancy of Fortune 1000 companies has gone from 70 years to 12 years (these are notes so I may be wrong with my recollection of facts, but the spirit was it) and the life expectancy of a product is 2 years.

So as a mayor, it is his mission to think about the future, not the present only. Eindhoven still strives because it has NXP and ASML (Spin-off from Philips), because they have the largest Samsung R&D center outside of Korea, and an antenna of the Singularity University. Rob van Gijzel unusually knows a lot about technology for a politician! Maybe it’s because it is Eindhoven… and Eindhoven is putting a lot of energy and money in universities, accelerators, start-ups and the unique high-tech campus Eindhoven (www.hightechcampus.com) which hopefully will create a lot of high value jobs. Big established companies, SMES, start-ups and universities seem to work together in the same direction. I am sure it is not perfect, but the effort is impressive!

Eurotech about Entrepreneurship

My second moment of inspiration was during a meeting of Eurotech about entrepreneurship. For once, it was not about the usual start-ups vs. SMEs, fast growth vs. controlled growth, but we had a great discussion about how to really help students interested in start-ups, about what is important, exposure to or teaching of entrepreneurship,

Just a few notes:

“early on you find inspiration, you are interested and you go where the crazy people are” … “it was the thing to do” …“I was an entrepreneur because my mother pushed me to be responsible and independent, then I tried, and failed twice, and then succeeded once”.

It is a long term effort, you teach, you expose, you inspire, and “you infect them with the virus” with possibly a long incubation. But should we do it early or late, compulsory or elective, filter the good entrepreneurs or expose/teach everyone…

“You need to teach entrepreneurship outside of the class…”

So you need a friendly ecosystem, where the university has its role (unclear which exactly, but it has one!) “Young entrepreneurs should know they do not need to pay for lawyers, they need to find friends who are lawyers, or who have a legal expertise.” You need to break the barriers, help people meet and find the people they need, also break the regional barriers because regional support focuses on local development, which is not necessarily the best friend of an entrepreneur who needs to think globally. Ecosystems have to be open, people need to travel, where the talent and money are

So we agreed there was not a general agreement on the strategic way of fostering entrepreneurship…though it is very important…

Occasionally, I write a short post that has nothing to do with the start-up. Well maybe it has… I was listening this morning France Culture which invited the philosopher André Comte-Sponville. At time 8:13 of the video below starts a sequence about transhumanism that the philosopher then comments. I also put it in writing below. I already had the opportunity to discuss the topic thanks to another edition of the same excellent program, on May 9, 2014: Ray Kurzweil has mostly wrong predictions.

To the question “André Comte-Sponville, will you take the bus to immortality”, he answers:

“No thanks! This is obviously excluded. Well more seriously some people predict, I think of Laurent Alexandre, that we will soon live 1’000 years. And his book is called The Death of Death. This is obviously a nonsense. Because, whether you die in 90 years or a thousand years, you would still die. We would live more but we would still die. As for the crazy idea, I would say, of suppressing death, again, it is an impossibility. No body, no living body can resist combustion, can resist drowning. If you spend 15 days under water, I swear that transhumanism or not, you’re dead. No human being survives a bullet in the forehead. In other words, even it happened, and God knows tomorrow is not the day, it is science fiction, but even if it happened that we win over every disease and aging, in other words we would only die by accident, well, sooner or later, because with infinite time, everything possible necessarily happens, we would have an accident and we would end up dying anyway. Simply, what would happen, as we would only die by accident, we would indeed perpetually be scared to death. What allows me to take my car today is that I know anyway that I will die and therefore dying of cancer or of a car accident, basically the difference is not essential. If I can die only by accident or murder, I’ll be perpetually scared to death. In short it will make a society of old human beings who will not have children as it would be terrible overcrowding, a society of old and coward human beings. Well that is not my ideal of a civilization or of humanity.

– So, does transhumanism scare you?

– No, again this is science fiction. That science and technology are becoming more and more present in our lives, that they may one day change human nature, that’s true. It is not there yet, but it can come and so it is legitimate to think about it. I want to say that urgent problems are elsewhere. We will be nine billion and a half, maybe ten billion in 2050, nobody knows how we will feed ten billion people. The issue of freshwater and arable land, the issue of global warming are far more pressing issues that the issue of transhumanism.

I change (slightly) the topic again. Here are books of another French philosopher whose clarity of thought and vision are exceptional. A must read. The world of start-up also needs courage, ethics and moral philosophy. Cynthia Fleury explains beautifully why any individual and any aociety also needs them… The lies of transhumanism and of societies and of individuals too must be fought!

Time to finish my account of In the Plex after already four posts. Chapter 5 is about Google in the mobile and in the video. Chapter 6 is about China, a very interesting chapter about Google’s moral dilemmas. Chapter 7 is about the relationships with government.

These chapters show Google is now a mature and serious company, with exceptions:

The keynote did end on a high note. Page had insisted that there be a question period, almost as if he were running a Google TGIF. This was almost unheard of in CES keynotes. The people at Google in charge of the speech came up with an inspired idea: they spent a bundle to book the comedian Robin Williams (a huge Google fan) as Page’s sidekick for the Q and A. The conceit was that Williams would be a human Google. The comic’s manic improvisations made people instantly forget the awkwardness of Page’s presentation. The funniest moment came when a French reporter began to ask a tough question of Page but could not finish due to Williams’s relentless, politically indefensible, and utterly hilarious mocking of the man’s accent and nationality. The unfortunate Frenchman sputtered with rage. The moment fit Google perfectly: corporate presentation turned as anarchic as a Marx Brothers skit. [pages 246-247]

“Sergey and Larry are not kids anymore,” Eric Schmidt noted in early 2010. “They are in their mid-thirties, accomplished senior executives in our industry. When I showed up, they were founder kids— very, very smart, but without the operating experience they have now. It’s very important to understand that they are learning machines and that ten years after founding the company, they’re much more experienced than you’ll ever imagine.” From Schmidt’s comments, it was reasonable to wonder when the inevitable would occur—when Larry Page, now middle-aged and officially seasoned, might once again become Google’s CEO, a job he had been reluctant to cede and gave up only at the VC’s insistence. When asked directly if he was eager to reassume the role, Page refused to engage. “That’s all speculation,” he said. [Page 254]

And the inevitable brain drain would follow

Google didn’t stop recruiting the best people it could find, especially engineers. In fact, the effort became more urgent because there were vacancies at Google created by valued employees who either joined tech firms that were newer and more nimble than Google or started their own companies. And every so often, an early Googler would simply retire on his or her stock-option fortune. The defections included high-ranking executives and—perhaps scarier to the company—some of its smartest young engineers. The press labeled the phenomenon Google’s “brain drain.” Sheryl Sandberg, who had built up the AdWords organization, left to become the chief operating officer at Facebook. Tim Armstrong left his post as head of national sales to become CEO of AOL. (“We spent all of Monday convincing him to stay,” said the grim Sergey Brin at that next week’s TGIF, expressing well wishes toward its valuable sales manager.) Gmail inventor Paul Buchheit joined with Bret Taylor (who had been product manager for Google Maps) to start a company called FriendFeed. Of the eighteen APMs—Google’s designated future leaders—who had circled the globe with Marissa Mayer in the summer of 2007, fewer than half were still with the company two years later. All of them left with nothing but respect and gratitude for Google—but felt that more exciting opportunities lay elsewhere. Bret Taylor, while specifying that he cherished his time at Google, later explained why he’d left. “When I started at the company, I knew everyone there,” he said. “There’s less of an entrepreneurial feel now. You have less input on the organization as a whole.” When he announced his departure, a procession of executives came to his desk asking him to reconsider. “I didn’t know Google had so many VPs,” he said. But he’d made his mind up. [Page 259]

Really reaching maturity?

Eric turned to him and said, “Okay, Larry, what do you want to do? How fast do you want to grow?” “How many engineers does Microsoft have?” asked Page. About 25,000, Page was told. “We should have a million,” said Page. Eric, accustomed to Page’s hyperbolic responses by then, said, “Come on, Larry, let’s be real.” But Page had a real vision: just as Google’s hardware would be spread around the world in hundreds of thousands of server racks, Google’s brainpower would be similarly dispersed, revolutionizing the spread of information while speaking the local language. [Page 271]

Failure in China

China has been Google deepest failure. Despite efforts and (too much?) compromise, Google has never really succeeded in China. Chapter 6 is another must read. Brin who has always been the most sensitive to human rights “went as far” as abstaining at a shareholder meeting.

During the Google annual shareholders meeting on May 8, 2008, Brin took the rare step of separating himself from Page and Schmidt on the issue. Shareholders unhappy with Google censorship in China had forwarded two proposals to mitigate the misdeed. The first, organized by Amnesty International and submitted by the New York state pension fund, which owned 2 million shares of Google, demanded a number of steps before the company engaged in activities that suppressed freedom. The second would force the board of directors to set up a committee focusing on human rights. Google officially opposed the proposals, and with a voting structure that weighted insider shares ten times as heavily as those owned by outside investors, the proposals were easily defeated. But Brin abstained, sending a signal—though maybe only to himself—that his conscience would no longer permit him to endorse the company’s actions in China unreservedly. When shareholders had a chance to question Google’s leaders, Brin explained himself: “I agree with the spirit of both of these, particularly in human rights, freedom of expression, and freedom to receive information.” He added that he was “pretty proud of what we’ve been able to achieve in China” and that Google’s activities there “honored many of our principles.” But not all.

It was a clear sign that Brin no longer believed in Google’s China strategy. Another signal was the fact that after Google China was established, and despite Kai-Fu Lee’s urging, neither Brin nor Page ever crossed the threshold of their most important engineering center abroad. Even in mid-2009, when the pair decided to fly their private Boeing 767-200 to the remote Eniwetok Atoll in the Pacific Ocean to view a solar eclipse and Brin used the occasion to drop in on Google Tokyo, they skipped China. Still, Google was reluctant to defy the government of China. There was still hope that things would turn around. In addition, its business operations in China were doing well. Though it had far to go to unseat Baidu, Google was clearly in second place and more than holding its own. In maps and mobile Google was a leader. In the world’s biggest Internet market, Google was in a better position than any other American company. [Page 305]

Finally…

“The security incident, because of its political nature, just caused us to say ‘Enough’s enough,’” says Drummond. The next day Drummond wrote a blog item explaining Google’s decision. It was called “A New Approach to China.” He outlined the nature of the attack on Google and explained that it had implications far beyond a security breach; it hit the heart of a global debate about free speech. Then he dropped Google’s bombshell: These attacks and the surveillance they have uncovered— combined with the attempts over the past year to further limit free speech on the web—have led us to conclude that we should review the feasibility of our business operations in China. We have decided we are no longer willing to continue censoring our results on Google.cn, and so over the next few weeks we will be discussing with the Chinese government the basis on which we could operate an unfiltered search engine within the law, if at all. We recognize that this may well mean having to shut down Google.cn, and potentially our offices in China.

On January 12, Google published the Drummond essay on its blog. The news spread through Mountain View like an earthquake. Meetings all over the campus came to a dead stop as people looked at their laptops and read how Google was no longer doing the dirty work of the Chinese dictatorship. “I think a whole generation of Googlers will remember exactly where they were when that blog item appeared,” says one product manager, Rick Klau. [Page 311]

And according to Wikipedia, https://en.wikipedia.org/wiki/Google_China “As of November 2013, its search share has declined to 1.7% from its August 2009 level of 36.2%”.

Google and Politics

By late 2007, Barack Obama already had an impressive Google following. Andrew McLaughlin, Google’s policy chief, was advising the senator on tech issues. The product manager for Blogger, Rick Klau, had lived in Illinois and had operated Obama’s blog when the politician ran for the Senate (he’d even let Obama use his house for a fundraiser). Eric Schmidt was the candidate’s official host. [Page 316]

In an ideal world: “I think of them as Internet values. They’re values of openness, they’re values of participation, they’re values of speed and efficiency. Bringing those tools and techniques into government is vital.” [Page 322]

But the reality is tougher: “The job was frustrating. Google hadn’t been perfect, but people got things done—because they were engineers. One of the big ideas of Google was that if you gave engineers the freedom to dream big and the power to do it—if you built the whole operation around their mindset and made it clear that they were in charge—the impossible could be accomplished. But in the government, even though Stanton’s job was to build new technologies and programs, “I didn’t meet one engineer,” she says. “Not one software engineer who works for the United States government. I’m sure they exist, but I haven’t met any. At Google I worked with people far smarter and creative than me, and they were engineers, and they always made everyone else look good. They’re doers. We get stuck in the government because we really don’t have a lot of those people.” [Page 323]

Final thought: Is Google evil?

This is a debate I often have with friends and colleagues. You’ve seen my fascination and I love the way Google tries, explores and changes our world. Still, one may see things differently. As an example, here are some quotes about Google Print.

Maybe the care that Google took to hide its activity was an early indicator of trouble to come. If the world would so eagerly welcome the fruits of Ocean [Google Print code name], what was the need for such stealth? The secrecy was yet another expression of the paradox of a company that sometimes embraced transparency and other times seemed to model itself on the NSA. In other areas, Google had put its investments into the public domain, like the open-source Android and Chrome operating systems. And as far as user information was concerned, Google made it easy for people not to become locked into using its products. […] It would seem that book scanning was a good candidate for similar transparency. If Google had a more efficient way to scan books, sharing the improved techniques could benefit the company in the long run—inevitably, much of the output would find its way onto the web, bolstering Google’s indexes. But in this case, paranoia and a focus on short-term gain kept the machines under wraps. “We’ve done a ton of work to try to make those machines an order of magnitude better,” AMac said. “That does give us an advantage in terms of scanning rate and cost, and we actually want to have that advantage for a while.” Page himself dismissed the argument that sharing Google’s scanner technology would help the business in the long run, as well as benefit society. “If you don’t have a reason to talk about it, why talk about it?” he responded. “You’re running a business, and you have to weigh [exposure] against the downside, which can be significant.” [Page 354-55]

But not all of the publishers found Google charming. Jack Romanos, then CEO of Simon & Schuster, later complained to New York’s John Heilemann about Google’s “innocent arrogance” and “holier-than-thou” attitude. “One minute they’re pretending to be all idealistic, talking about how they’re only in this to expand the world’s knowledge, and the next they’re telling you that you’re going to have to do it their way or no way at all.” [Page 357]

[There] was the conviction that in a multimillion-dollar enterprise such as Book Search it was unconscionable for authors and publishers not to be paid. After the debate, Aiken laid out the essence of his group’s rationale to an Authors Guild member who told him that he’d like his books discoverable by Google. “Don’t you understand?” Aiken said. “These people in Silicon Valley are billionaires, and they’re making money off you!” [Page 360]

Google has missed opportunities such as in social networking. Orkut, then Wave, Dodgeball, Buzz replaced by Google + were more beta tests and then a reaction to Facebook. Google often tries things without much effort and checks if traction comes or not. But its ambition has not really slowed down: “Michigan had already begun digitizing some of its work. “It was a project that our librarians predicted would take one thousand years,” Coleman later said in a speech. “Larry said that Google would do it in six.” [Page 352]

Indeed Page had dreamed about digitizing books already at Stanford and in the early days of Google, he began playing with scanners, helped by Marissa Meyer: “The first few times around were kind of sloppy, because Marissa’s thumb kept getting in the way. Larry would say, “Don’t go too fast … don’t go too slow.” It had to be a rate that someone could maintain for a long time—this was going to scale, remember, to every book ever written. They finally used a metronome to synchronize their actions. After some practice, they found that they could capture a 300- page book such as Startup in about forty-two minutes, faster than they expected. Then they ran optical character recognition (OCR) software on the images and began searching inside the book. Page would open the book to a random page and say, “This word—can you find it?” Mayer would do a search to see if she could. It worked. Presumably, a dedicated machine could work faster, and that would make it possible to capture millions of books. How many books were ever printed? Around 30 million? Even if the cost was $10 a book, the price tag would only be $300 million. That didn’t sound like too much money for the world’s most valuable font of knowledge.” [Page 360] (Google Print is now Google Books – https://en.wikipedia.org/wiki/Google_Books)

In 2011, Page ambition is still there. He is now the CEO. In late 2010, “Sergey Brin had repeated the sentiment: ‘We want Google to be the third half of your brain’ “. [Page 386]

“I just feel like people aren’t working enough on impactful things,” Page said. “People are really afraid of failure on things, and so it’s hard for them to do ambitious stuff. And also, they don’t realize the power of technological solutions to things, especially computers.” He went on to rhapsodize about big goals like driving down the price of electricity to three cents a watt—it really wouldn’t take all that much in resources to launch a project to do that, he opined. In general, society wasn’t taking on enough big projects, according to Page. At Google, he said, when his engineers undertook a daunting, cutting-edge project, there were huge benefits, even if the stated goal of the project wasn’t accomplished. He implied that even at Google there wasn’t enough of that ambition. “We’re in the really early stages of all of this,” he said. “And we’re not yet doing a good job getting the kinds of things we’re trying to do to happen quickly and at scale.”[Page 387]

I just finished In the Plex and I kind of feel sad. It is a book I wish I would never have finished reading. I have now read four books about Google. In fact, we are far from the end. It may even be just the beginning as Page and Brin seem to believe and I will probably read other books abotu Google in the future. As good as this one? Only the future will tell… but i will finish here with a 2007 post.

I recognized some of my concerns in the foreword of the author, in his frustrations and his hopes. “Our start-ups do not grow in Switzerland. No trace of a Swiss Google. The last major Swiss success was Logitech, thirty years ago. Our start-ups are certainly good. But when it comes to grow rapidly and on a large scale, they leave Switzerland”[Page 9]. And his answer? “[…] If Switzerland wants to remain prosperous, if it wants to be able to anticipate and invent the world of tomorrow, we need two basic ingredients: memory and craziness” [Page 11].

Switzerland is not world champion of innovation

Derder is concerned about the lack of interest of the media and politicians because everything would be fine in the best of Swiss worlds…but: “The rankings are misleading and based on an abuse of language: we are certainly world champions in education, research, science and patents (from the multinational corporattions). But not in innovation. These are two different things. But in terms [of innovation] (the transformation of ideas into products and services that create value), there is much room for improvement” [Page 18-19].

To have the next Google in Switzerland, you need to have to the three “C”, Capital, Cerveaux (brains) and a Culture of failure and risk [page 35].

This certainly reminds me the “How to be Silicon Valley” by Paul Graham: “Within the US, towns have become startup hubs if and only if they have both rich people and nerds. Few startups happen in Miami, for example, because although it’s full of rich people, it has few nerds. It’s not the kind of place nerds like. Whereas Pittsburgh has the opposite problem: plenty of nerds, but no rich people.”

In this book of almost 180 pages are listed the ten conditions:

• Attracting the best talents

• Boosting venture capital (and encourage investment in SMEs)

• Simplifying the lives of entrepreneurs (and of investors)

• Providing resources for basic research

• Bringing universities and businesses together

• Developing thematic centers of excellence

• Establishing a national digital strategy

• Committing the state (and the army) to the ecosystem

• Enhancing data protection (and encouraging citizens to protect them anonymously)

• Valuing the Swiss success stories (and make them popular)

Derder is a super supporter of start-ups and his book is a great addition to understanding why start-ups are unique and essential. I believe however that the challenges are mostly cultural as I wrote recently in Why doesn’t Europe create any Google or Apple? You will not be surprised therefore if I prefer to stop with his 3 “C”s. In a presentation I recently prepared, I gave my ten conditions for innovation, all linked to a culture of innovation:

• Collaborate, even with Competitors

• Be Trustful

• Have a healthy disrespect for authority

• Do not lie (to yourself)

• Believe in your Instinct …

• … and have Courage

• In Innovation, the example comes from above

• Bet on Talent (and Youth)

• Do not fear Failure

• Be passionate