After my initial notes (part I) and the importance of culture (part II) in the Rainforest by Hwang and Horowitt, here are my new notes about their recipe to build efficient ecosystems for entrepreneurial innovation. I will finish with a part IV about venture capital.

Again the authors remind us that “innovation is chaotic, serendipitous and uncontrollable, so processes that are linear and controlled are rarely self-sustaining. In contrast, what we strive for in a Rainforest is a system that yields immense impact, is low-cost, and generates internal sustainability. The only possible way to achieve these goals is to build a community of innovators where transaction costs have been reduced through the creation of trust, social norms, connectivity and diversity.” [Page 183]

So their recipe is not so much a recipe as a cure. In fact they say “rather than thinking like macroeconomists, to change behavior, we must think like psychiatrists […] We build rainforests by shaping the outward behavior of innovators. Over time, those behaviors can create changes in attitude, and eventually, the changes in attitude can lead to change in beliefs”. [Page 200-1]

In the recipe [pages 194-200], there is Hardware made of 4 “P”s: People, Professional, (i.e. institutions), Physical (i.e. infrastructure) and Policy. Hardware is necessary but not sufficient. There is also Software, with 5 pillars, Diversity, Extra-Rational Motivations, Social Trust, Rules (see my previous post) and Interpretation of the Rules. The Keystones will make all this possible.

The Rainforest canvas may be a helpful tool to assess the situation of an ecosystem in its physical and cultural components:

About Role Models, they have the interesting Porsche principle. “This principle holds that one of the greatest motivators for professors or graduate students on campus to start new companies is when one of their colleagues drives up in a new Porsche after selling their startup”. [Page 210] To be honest, today, at EPFL and probably elsewhere, I would call it the Tesla principle… (see my previous post…The University-based Startup Porsche Principle. Or is it the Tesla Principle?)

In their epilogue, the authors explain that “Perhaps, instead of fighting the chaos, we need to become more comfortable with it. Perhaps we just need a better map. The Rules of the Rainforest provide a useful map – one that shows the way to balance the freedom of chaos with the beauty of collaboration. […] It requires a ‘joyful participation’ in the ups and downs, the mistakes and the failures that are inevitable. Thus, love is like a solution to chaos. ” [page 280] They use a magnificent quotation from Richard Feynman to whom a student asked to write a message to his mother so that she would be interested in science. Here it is: “Tell your son to stop trying to fill your head with science – for to fill your hear with love is enough. Richard Feynman (the man you watched on BBC ‘Horizon'”.

Here is a slideshare presentation by the authors, which beautifully summarizes their vision.

After my introductory post about The Rainforest – The Secret to Building the Next Silicon Valley by Victor W. Hwang and Greg Horowitt, which focused on the importance of trust, here is a second piece about culture. The final part will describe how the authors claim they know the recipe to build rainforests. What is remarkable with the Rainforest is the ambition to explain that innovation is mostly cultural so that at the micro-level it cannot really be engineered, but at the macro-level rainforests can be built. I am not sure the authors are right, but the effort is really to be recognized.

One lesson of the Rainforest is that outcomes cannot be engineered. […] Serendipity itself cannot be engineered but an environment that is conducive to serendipity can be. [Page 65]

In their chapter 3 about People, they begin with Keystones, not Entrepreneurs. “What defines a Keystone? Over the years, we have observed certain individuals practicing a unique manner of human interaction that is critical to the growth of entrepreneurial innovation. […] These people are usually missing, or at least too scarce, in almost all regions that have failed at generating significant amounts of entrepreneurial innovation.” [Page 71]

These people are integrative, influential and impactful, they are brokers of social trust (by contrast to entrepreneurs who are people who absorb information, learn from practice and seek opportunities). “The San Francisco Bay Area has a vastly higher percentage of people who are involved in multiple firms. 4.5% of the actors counted in the Bay Area were involved in three or more startups, compared to 2.9% in Boston, 2% in San Diego, […] 1.2% in Austin […] 0.7% in Portland. […] The bay Area has a significantly higher share of individuals who are extremely connected and contribute to the growth of multiple startup ventures”. [Page 74]

The authors also show the diversity of psychologies, the diversity of backgrounds in people which are still connected and work together. “We see these unconscious behaviors at work with innovators everywhere in the world. Scientists versus entrepreneurs. Startups versus large corporations. Investors versus investees. These tribal conflicts can be obstacles to the development of Rainforests.” [Page 109] All the more that: “Similarly the process of building a startup company is one in which people must often rely on gut-level decision-making. Entrepreneurial innovation, by its nature, is virtually a never-ending series of educated guesses. Almost every decision is based substantially incomplete information.” [Page 106]

America is the building of a society not burdened by historical tribes. […] They are less chained to the past. Instead Americans tend to be identified by self-reliance. […] People still run to California today. It is commonly regarded as the land of pioneers, nonconformists, artists, and rebels. [Page 116] Culture is critical to the way economic systems function because it provides the rules of engagement between people that hopefully can maximize their collective well-being. [Page 118] The authors are not naïve but claim that all these people need to find the right balance. A venture capitalist is caught between trying to own as much of a company as possible and trying to leave enough equity in the hands of the entrepreneurial team to keep them fully incentivized. […] A VC wants to preserve a reputation. [Page 119] Innovative behavior is not driven by rational maximization. There are in fact other forces, which can be called extra-rational: competition, altruism, adventure, discovery, creativity, meaning, concern.

Here I cannot avoid mentioning the great (counter-)example of Orson Welles about the Scorpio and the Turtle… Hopefully nature is not everything, culture matters.

One mistake of policy makers is to underestimate these extra-rational motivations. “Governments and corporations often try to incentivize innovation by focusing on financial mechanisms, such as tax breaks, subsidies, grants and loans. But overall, this strategy has been poor. They cannot be only the ends in themselves.” [Page 127]

Traditional incentives, benefits and costs: [Page 124] Benefits:

Some possibility of making more money Costs

Sacrifice a stable income and career perhaps forever

Risk social disapproval from family, friends, potential spouses

Difficulty and fear of working with strangers outside conventional circles of trust, culture, ethnicity, language

Difficulty and extra effort in communicating effectively

Huge investment of time, effort, stress

Possibility of losing everything (depending on laws, regarding bankruptcy, partnerships, etc.)

Rainforest incentives, benefits and costs: [Page 126] Benefits:

Perceived and possibly real opportunity of making more money (following role models that have validated the path already)

Joy of discovery, novelty, adventure, creativity, passion

Social approval (as a peer member of a community of innovators)

Joy of friendship, sharing, love working on a team, building new trust, common values and goals

Fulfillment from the possibility of making a difference in society, leaving a legacy for future generations

Thrill of competition

Freedom and independence Costs

Little social punishment, often encouragement, from family and friends for taking a worthwhile risk

Some anxiety from meeting new people, but offset by the joy of making new friendships

Huge investment of time, effort, and stress, but viewed in a neutral or even positive light because pursuing a personal passion

Little risk of losing everything because new opportunities emerge in the process of experimentation

Much lower probability of failure from a broad community of fellow innovators.

And the authors claim what are needed are 7 rules [Page 156]: – Break the rules and dream

– Open doors and listen

– Trust and be trusted

– Experiment and iterate together

– Seek fairness, not advantage.

– Err, fail and persist.

– Pay it forward.

People usually think of Silicon Valley as an anomaly in the otherwise “normal” history of the world, but what if we reversed that proposition? What if we envisioned Silicon Valley as the natural endpoint of a 50,000-year story? Perhaps it could be the latest stage in the evolution of human society, from a culture based on tribes to a culture based on pragmatic individuals. [page 152]

I must thank here first Bogdan Ceobanu from the European Commission. After spending a few hours discussing the challenges (and opportunities) of innovation in Europe, he sent me his copy of The Rainforest – The Secret to Building the Next Silicon Valley by Victor W. Hwang and Greg Horowitt. Bogdan is one of the leading voices behind Startup Europe. Thanks 🙂

There may be nothing really new in this book about ecosystems, but the messages are strong and clear. You may need an infrastructure, but without culture, nothing will happen, no innovation will emerge. I might write a few posts about this book as I just began reading it recently. And as usual, here are my notes / extracts.

Despite hundreds of books and thousands of papers on the subject, real-world innovation is little understood. […] Having the right ingredients will not necessarily result in successful innovation. You need to prepare those raw ingredients, combining them in just the right way. […] We argue that the two pillars of innovation’s conventional wisdom – free markets and clusters – are unable to provide comprehensive answers to the mystery of systemic innovation. [Pages 18-20]

Funnily enough, I gave my own recipe in 2007: “Two main ingredients are needed, rich people and nerds; this has been said already. Do not add any bureaucracy, do not add concrete. In order to attract and keep enough nerds, there is a need for a large and nice plate. A university is a good choice. But it must not be a university like any other; it must be a superb university. There are some; a few are being built from scratch. It needs a unique personality, and it needs to be creative. Not only on its campus, but also in its surroundings, so that the ingredients feel comfortable in the plate. They should be fresh, i.e. they should be young and dynamic. Young and dynamic people are the founders of start-ups. Graham also mentions liberal environments, which, he claims, tolerate strange and brilliant individuals. Then the ingredients have to be put in the oven for a very long time. Silicon Valley began in 1957, Silicon Fen in 1960. It took ten years, maybe even twenty years, to make these two regions successful; it is about the time it takes to grow infants into adults. The oven should not be too hot, so that the desire is not killed, then the temperature should be increased to maintain the enthusiasm. A temperate, pleasant climate is therefore necessary. If all the conditions are in place, the result will probably be interesting”. [Page 176. Start-Up: What We May Still Learn From Silicon Valley]

The world of innovation does not happen at the macro-level. Innovation is a “body contact sport.” It is a micro-level phenomenon. When applied to innovation, rational choice theory might make sense if you’re a theorist thinking abstractly about the way the world should work. It does not accurately describe the way the world actually works. [Page 37] You cannot understand the macro without understanding the micro. […] the world is far more complicated – one must deal with a range of complex social and psychological factors, personal networks, and information flows. [Page 48]

Free market proponents sometimes support investments in scientific research as a way to stimulate new innovation. […] Scientific research, however, does not always lead to economic growth. Each $1 increase in scientific research does not necessarily result in a $1 increase in economic activity in the overall system. The research alone is not sufficient. […] In the real world, the path from discovery to commercial product is so long, tortuous, and serendipitous that the vast majority of world-changing technologies never see the light of day. Society has a surprisingly huge backlog of scientific discoveries that are “stuck in the pipeline”, stalled by the human barriers that prevent them from reaching the marketplace. [Page 40]

For instance, the state of Kansas actively invested in its high-tech entrepreneurs. The University of Kansas provided research grants to develop products for commercial application. The university promoted regional collaboration, entrepreneurial training and even direct assistance. The results of these endeavors, however, were nothing like those of Silicon Valley. And the vast majority of the world looks a lot more like Kansas than California. [Page 41] A cluster is a description of a phenomenon, not a prescription for policy. [Page 42]

Whereas a company is a group of individuals working together, a cluster is a region of individuals or companies working together. In both cases, these relationships result in lower transaction costs. And in both cases, those savings are derived from the fact that people are closer together, can communicate more easily, and trust each other more. [Page 46]

And again let me give you an extract from my book, now quoting Richard Newton: “The Bay Area is the Corporation. […When people change jobs here in the BayArea], they’re actually just moving among the various divisions of the Bay Area Corporation.” [Page 102 – Start-up]

I am not sure anyone has “The Secret to Building the Next Silicon Valley”, but I will post more when I am more advanced in reading the Rainforest!

The recently published The State of the European Tech, co-sponsored by Atomico and Slush is an extremley interesting analysis of the European tech start-up and VC scene. it is a rather long 118-slide document but most (not all) pages provide food for thought.

Here are a couple of comments, in the page order:

– The introduction is too optimistic (slides 5-7). I doubt their title: the future is being invented in Europe. But it has always been Atomico’s founder vision: see Europe and Start-ups : should we worry? Or is there hope? The future will tell us… One interesting point though: London, Berlin and Paris are the 3 hubs main European hubs and Paris was probably underestimated (in the past).

– The entrepreneurial mindset is continuously improving (slides 15-16). Repeat entrepreneurs are more numerous (slide 18). And they mention their importance not so much as future successful entrepreneurs (you may know my doubts – check Serial entrepreneurs: are they better?) but because of the experience and network they bring.

– I love slide 21 with EPFL #4 world wide in Computer Science (though I hate these rankings!). Switzerland is clearly on the map together with the UK. I am honestly less convinced about the impact of business schools in tech (slide 22). Talent exists in Europe but may not be available for tech (slide 23).

– Again the three top hubs are obvious: together London, Paris and Berlin outnumber Silicon Valley. But the ranking from #4 to #20 is mostly linked to city size, not so much any unique positioning. Tech is creating jobs faster than other industries (slide 26). Never too late! But again Europe is fragmented with 153 identified tech hubs (slide 34)

– Migrants (slides 27-29). Again the UK is #1. France and Germany follow. And Switzerland is well-ranked (except for non-Europeans).

– Local entrepreneurs want to stay home (slide 37): 60% prefer home to another place in Euope (17%) or Silicon Valley (12%), even if 25% of founders incorporated outside of their home country (slide 38). Clearly Europe exists! Even if slide 39 shows more local migrations inside Europe, with the exception of London and Berlin again and the links between hubs are weak (slide 41)

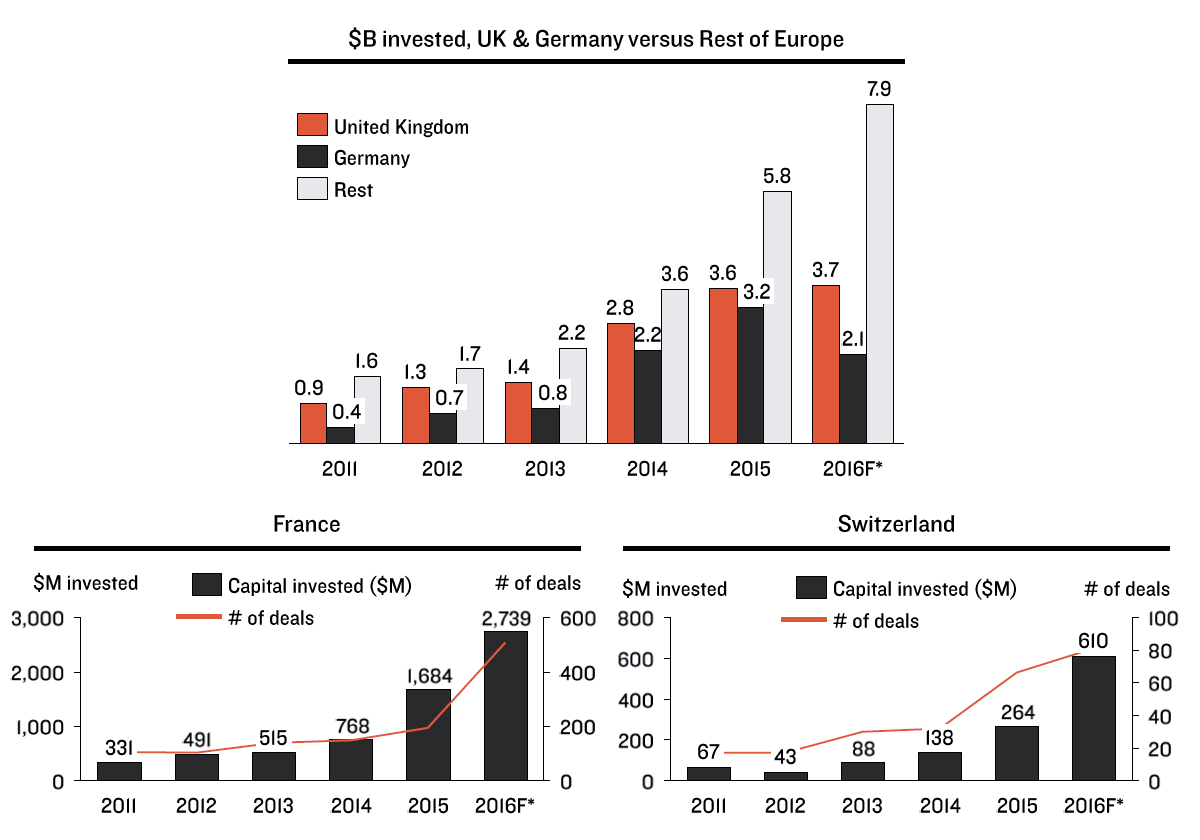

– The slides about venture capital are the most surprising. Slide 46 shows that the European investments have jumped from less than $5B before 2013 to $13B in 2015-16. (In comparison the US is about $30B). And the growth is consistent from early eseed ($0-2M) to early stage ($2-5M) and later stage ($10-50+M). I assemble here their data about the UK, Germany, France and Switzerland (slides 50-52). A new generation of investors is confirmed, those who were entrepreneurs 1st (slide 60). The early such actors were Atomico, Liautaud/Balderton, Niel/Kima. But many emerge. A new generation of funds also emerge (slide 64), and yes, US funds invest in Europe (slide 65)

– Their section about deep tech is less convincing (to me). Probably I did not fully understand what they meant by that and why it would be so special. Slides 78-9 about US tech giants coming to Europe and about their acquisitions in Europe is worth checking though.

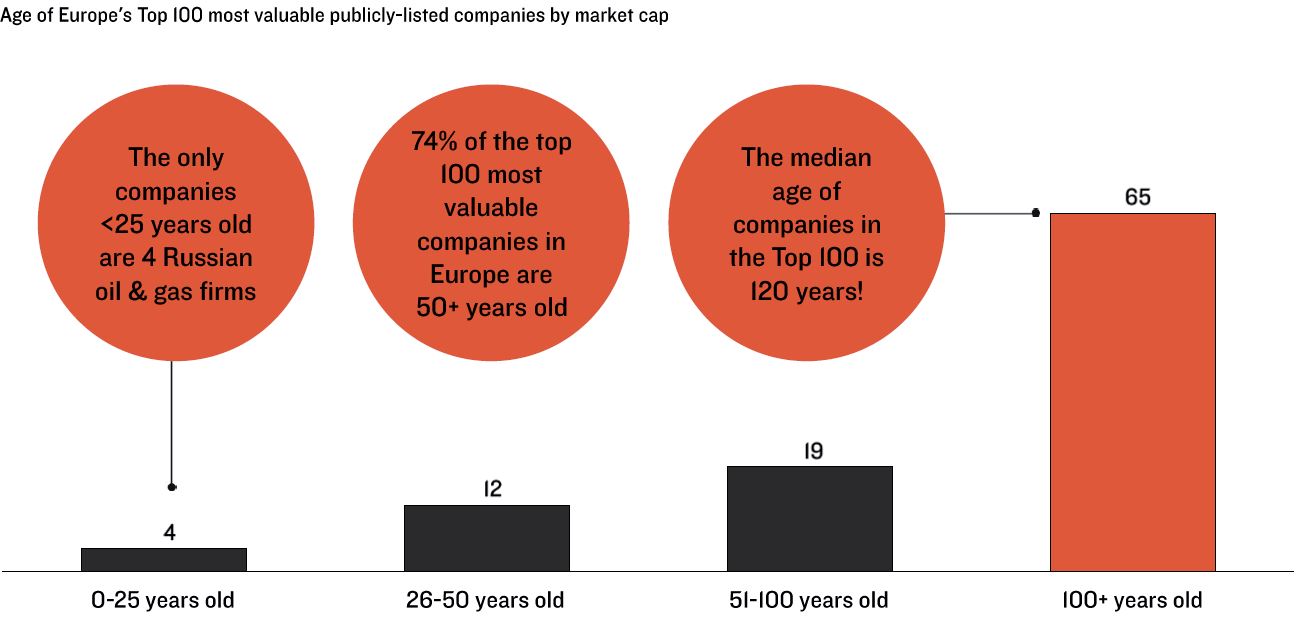

– I was not convinced either about the growing awareness of European corporations of the importance of tech. Their investments and acquisitions are still small compared to their US counterparts (slides 84-86). But slide 83 is the confirmation of a scary situation. This is another illustration of the Darwinian and Lamarckian innovation. Look at next figure.

– The section about scale-ups and exits (slides 89-101) could have been called unicorns & IPOs. I see bubbles and low value creations. Not good enough and not enough tech…

– Finally the lside about perceived risks is worth spending some time. they classify them as Business issues (40%); Economic issues (30%); European issues (22%); International issues (8%). But somehow their classification is subjective. For example if you combine risk aversion (4%), fear (2%), ambition (2%), that is 8%. And talent (4%), innovation (3%) and education (2%) would be another 9%. These elements which I consider as cultural could be considered as quite high…

All these notes were taken while reading so don’t see them as a deep analysis and you should build your own views about this really interesting analysis.

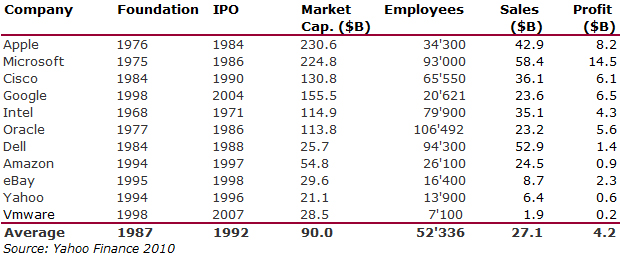

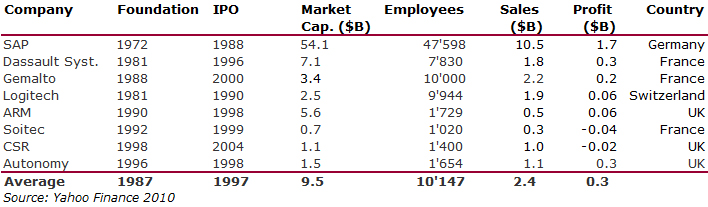

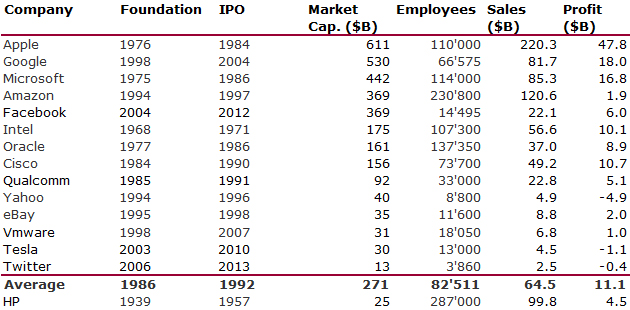

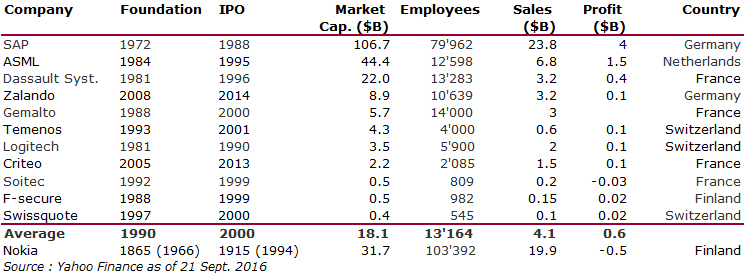

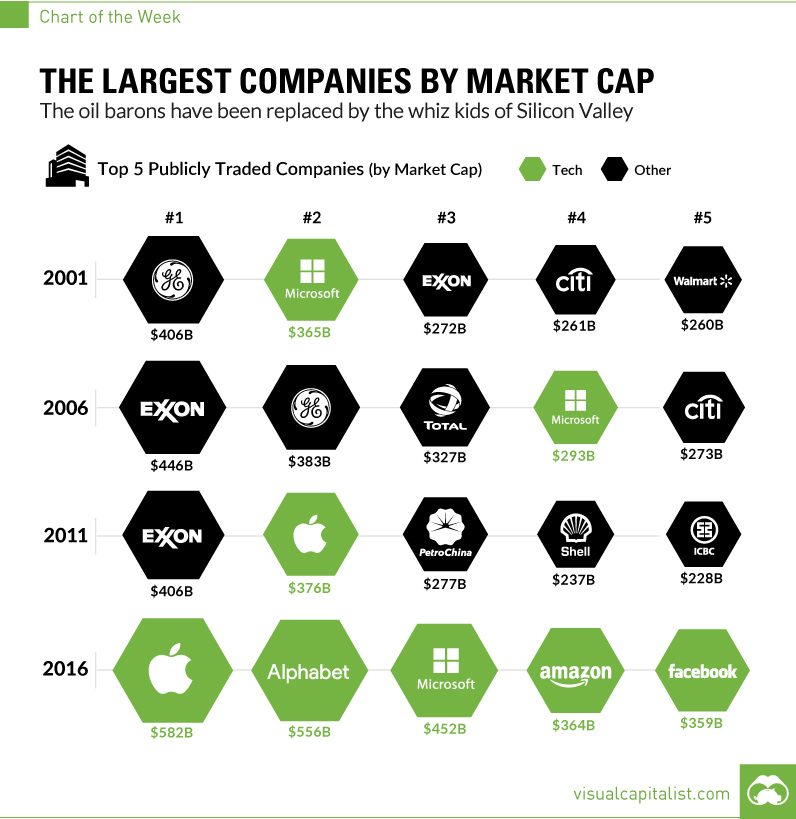

Since I published my book in 2007, I have regularly been doing the exercise of comparing the largest US (former) start-ups and their European counterparts. In 2010, I had the following tables:

What I call former start-ups are public high-tech companies which did not exist 50 years ago. Of course Europe is struggling; this has been (and still is) my concern and the reason of my book. Now here is my latest exercise.

I will let you make your own opinion about how things have evolved. I see quite striking elements. The main one comes from a presentation I saw a few days ago about the evolution of the American biggest market capitalizations. Here it is… quite impressive…

I did not know much of the background of the Samwer brothers beyond the names associated with them: Alando, Jamba, the European Founders Fund, Zalando and Rocket Internet. So I was surprised to be mentioned (thanks Kevin!) a book by Oliver, one of three brothers, America’s Most Successful Startups.

Even if now more than 15 years old, it is a good book at least from the first 30 pages I have read so far. It reminds me the advice from Steve Blank. Just one example about founders: “The first thing you have to make sure when you put tagether a team of founders is that all founders share the same vision and the same values. The group can be heterogeneous, but the founders cannot have a different vision or a different set of values, because they will probably be partners for many, many years. You absolutely need to make sure that the goals of the founders are all aligned. Each of the founder has to be very sensitive what each of the other founders’ objectives are. You have to recognize these and try to incorporate them, because otherwise you will have people from day one heading in fundamentally different directions. Only if you get a team of really great people together, who share the same vision, and work together well as a team, you will create a very strong foundation for the company. Because everything in the company originates from the founding team and will grow out of that”. [Page 30]

Additionnally, concerning their roles: “Fourthly, depending on the business model, a high-tech company should typically have at least three key people: It should have a market visionary, someone who understands the market, the customer and the problem the customer has. It also has to have a product or technology visionary, who understands the product and technology and how it might be applied, but does not necessarily understand all the problems that the market has. And it needs a business execution person, because the idea itself if worth zero. It is the execution of the idea.” [Page 31]

Another interesting comment about Equity sharing: “Last but not least, the founders should hold equal stakes in the company so that they are in every respect equal partners. No matter who the idea bad and who contributed what in the founding process, the founders should split the company equally among them. Otherwise some founders will feellike second-rate founders, which produces a flaw from the very beginning and which might have a strong negative effect on the way.” [Page 31]

Marc, Oliver and Alexander Samwer

Finally, I also liked their point of view on what you should do when at school: “Also, you need to try actively to get an educational background and experience that supports the venture. This really has to be an active approach. You have to put yourself in a position where you get involved in startups, you have to go to the places where entrepreneurs are, you have to go to places where you can get inspired, you have to meet people of similar spirits and build a network. In school you might participate in the business plan competition, take the classes where you will write a business plan, and take the entrepreneurial track at business school. That is where the people who want to do it are. […] Through such activities you will be meeting partners and ideas incidentally.”

I heard so many times that Silicon Valley is not any more the place where to be or where to go, that when I read again the emails I had recently with a student, I asked to let me publish some of his words.

April 2 – Dear Hervé,

I just wanted to update you on my achievements so far in the Silicon Valley. First of all, this place is amazing! It is the first time in my life where I feel so accepted. The events and style of those events is just incredible. This is so much fun!

I met so many inspiring people there. I spent the weekend getting to know the people I am living with. I guess I did not tell you exactly that I live in an entrepreneurs’ house. It’s like a long term hostel for entrepreneurs and by entrepreneurs. I am so inspired by all of the stories!

I also visited a European institution on Thursday. And talking just between you and me I was really disappointed. People were very nice on the surface, but did not help me very much. Just the night before we were talking with some entrepreneurs that a lot of entrepreneurial problems arise in Europe because of lack of cooperation and common goals between the governments.

April 8 – Hervé,

I definitely want to return to Silicon Valley later. Another update of nearly a week’s progress: I visited another amazing conference! Feel so inspired. I also visited one Meetup on the topic of big data. It was really good. I also had an opportunity to participate in an event organized by the Scottish government – it was a very high level event. This is what I love about the Silicon Valley – I would have to try very hard to get into something like that in Europe.

Best,

April 18

I really love this place! 🙂 […] I can also give a short summary of what I did during my 3rd week here. I am so proud of the fact that I have visited Google twice! It’s an amazing place! I have also driven past some famous Silicon Valley giants like Cisco, Intel, IBM, Oracle (I loved the Oracle style!). I also went to the place of Shockley Semiconductors and Fairchild Semiconductors.

I went to some events at Plug and Play – very nice place. People have good connections there. Visited an event at Rocketspace accelerator. Completely different atmosphere. Attended another event by IESE (European business school) at Runway accelerator. Saw some Germans, liked the style. Had another event at SRI. Such a protected space, looks like the military future is in there. The event was about robotics – I felt stupid there because I know nothing about robots, but learnt a lot of stuff.

Lastly, as I have mentioned earlier – had the chance to meet […]. I love his speeches. However, it was a bit disappointing because the material was not really new. He just spoke about the same stuff which is on youtube. In general, I just love my time here. I have almost no time to respond to emails (as you can see), but I meet so many people and visit so many places!

May 6

Regarding the last two weeks of my stay – boy were they crazy. I have visited a lot of events. I have met some Europeans who live in San Francisco area. Actually it was a bit disappointing because they were not really entrepreneurial, more like benefiting from the local atmosphere.

I have been to another pitching session in San Francisco – totally secured my opinion that everyone has a chance to pitch and so many people use the opportunity even though the technologies are not really exceptional. I have spent the Easter at Stanford. There was the demo day and final pitches from participants of E-Bootcamp. Stanford left a very good impression – the quality of pitches and organization is different from the rest of Silicon Valley. The next week I went to Entrepreneurial thought leaders event at Stanford – an interview with Morris Chang. Very nice idea to have such events.

To shortly summarize my trip to the Valley it was truly a revolutionizing experience! I have learnt and saw so much. I feel like I have done another semester at EPFL! I think that entrepreneurship around the globe is very different. It is always possible to make something different than Silicon Valley and tailor it to the local atmosphere but in many cases some traits of the culture need to be changed. And that is probably the hardest thing to change. It requires much more than money injections. I am very happy about my choice to go to SV and I think this has made a huge impact to me as a future entrepreneur.

A few years ago, I had participated to a roundtable in Grenoble. I was trying to explain my views about the differences between here, Europe, and there, SV. It was criticized a lot for that “biased, one-sided view” of things when a young entrepreneur reacted. She had just come back from a trip to SV and it was a first time there. “I met more people and learnt more things in 10 days than I would have in in 6 months in Grenoble.” This was in 2011. I believe it is still true in 2014. I still believe SV is the place where to be or at least to go if you want to accelerate your learning about innovation and high-tech entrepreneurship.

This is my translation (well Google translation) of a very good article I read in newspapers La Tribune de Genève (pdf here) and 24 heures (pdf here). I am not sure I have the rights to do such a transaltion. I will do it the Google was and hopefully the news papers will not complain…

If you do not want to read it all, here are just two short quotes: “Some explain the excitement that prevails here because of a feeling of urgency, says Christian Simm. We must go quickly, people know they cannot work 80 hours a week for twenty years.” and “You want to know the secret of Silicon Valley? asks Fadi Bishara, head of the incubator Blackbox. Failure is not an issue. It is completely accepted. It is even considered an apprenticeship.”

The Dream of Silicon Valley Can the Lake Geneva area reproduce the ecosystem of the U.S. technology hub ?

by Renaud Bournoud

Often imitated, never equaled. The famous ecosystem of Silicon Valley, near San Francisco, is one of the most dynamic regions of the world. The success stories of Google, Apple and Facebook continue to fascinate, even on the Lake Geneva. But on paper, this Eldorado for innovation has much in common with our region. In a similar geographic area, a large bean sixty kilometers long, the two countries are ranked in the world’s most successful regions. If Silicon Valley is based on the prestigious universities of Stanford and Berkeley, the Lake Geneva can count on the EPFL, the Universities of Geneva and Lausanne or the IMD, the High School of Management. In both cases, the density of highly qualified people is high. Even daily commuters from Silicon Valley experience the discomfort that we know well . They also wait for hours in traffic jams. U.S. Highway 101, which irrigates the valley is as congested as the A1, between Lausanne and Geneva. Housing is also a concern that we share with them. The real estate prices are well above the U.S. average and have nothing to envy to those on Lake Geneva. So what are the ingredients that make Silicon Valley so special?

Demographic factors

A century ago, the orange groves reigned as kings over this corner of California. Now the land has nearly four million people. More broadly, the population of the San Francisco Bay is the size of that of Switzerland. The presence of reputable universities brings a lot of talent, as well as the attraction of the region. Silicon Valley Community Foundation considers that 60% of the engineers were born abroad, many of whom are from Asia. But the valley also attracts many Americans. “Here we are at the extreme west of the United States. We cannot go further, says Christian Simm, founder of Swissnex (note: the Swiss Agency for Promotion of Science and Innovation) in San Francisco. People who consider Boston too quiet come here to create. Because everything seems possible.” This density of great talent pool is ideal for company recruitment. A startup like Square, active in payment systems, could recruit 600 programmers in less than four years. This would not necessarily be feasible in the Lake Geneva region. These people have often come alone and can concentrate fully on their work. “Some explain the excitement that prevails here because of a feeling of urgency, says Christian Simm. We must go quickly, people know they cannot work 80 hours a week for twenty years.”

Cultural factors

A they arrived alone in Silicon Valley, people are quite willing to meet others, creating a culture of networking. Many networking events are regularly organized, like the Start Up Weekends. They also exist here, but in smaller proportions, simply because the population and the number of start-ups are lower. “It makes it easy to find a partner to build a startup,” says Ahmed Siddiqui, one of the organizers of Start Up Weekends Bay Area. “Here the world lives around the field of technology , explains Alexandre Gonthier, the boss of PayWithMyBank in Redwood City. I met my partner at the playground where I watched my children.” Not only can we can find a future partner in the sandbox, it is also easy to cross the pundits of Silicon Valley at random from a barbecue party. They are available and are ready to play mentors for younger people. “It is not as easy to meet bosses in Europe … Unless they learn that you are installed in Silicon Valley. There, the doors open,” notes Alexandre Gonthier. Contacts are natural, and the mentality towards failure also has a role. “You want to know the secret of Silicon Valley? asks Fadi Bishara, head of the incubator Blackbox. Failure is not an issue. It is completely accepted. It is even considered an apprenticeship.” And if the project does not fail, it will soon be on the market. “The minimum viable product” is the leitmotif of the Silicon Valley. “We need to create something simple that you can use right away,” says Solomon Dykes, the founder of the start-up Dotdoud in San Francisco. “I would add that the idea is not very important, Fadi Bishara continues. Googje invented nothing, there were already search engines. What matters is the “packaging”, how the project is sold.” It’s the reason why storytelling is used a lot to sell. These stories also serve to develop an entrepreneurial spirit. Many myths have grown from Silicon Valley. There is the famous story about the birth of startups in garages. Like, for exampl , Google, which had rented a garage, whereas it had already raised $ 1 million.

Financial factors

Good idea or not, nothing is possible without money. The region of Silicon Valley attracts 46% of venture capital in the United States, according to the Bay Area Council Economic Institute. This happens especially much earlier in the development of projects than here.” If, after a year , the start -up has not found funding , we believe that we need to move on,” adds Jeff Burton , director of Skydesk , an incubator located on the Berkeley campus . “For us, the institutional money comes much later, said Joao Antonio Brinca, representative of BCV board at the Foundation for Technological Innovation in Lausanne. Financing through venture capital funds typically occurs between the fifth and seventh year of the project life. “The sums involved are not the same. A young company of Lake Geneva can hopee to raise between 300,000 and 600,000 francs for its first round of funding. In Silicon Valley it is at least twice. So there is a gap between the first efforts of startups to exit the academic world and the interests of investors . This longer period may explain the difficulty of transforming research into marketable products. Another advantage of Silicon Valley is its close proximity maintained between universities and private firms. In this regard, the Lake Geneva is still lagging behind. But it would be wrong to say that nothing is done about it. EPFL has worked in recent years to attract firms in the area of innovation, so that they mingle with the start-ups. But again, the structures of the same type that abound in Silicon Valley are favored by the scale. The density of start-ups produces a unique emulation world. Also keep in mind the economy of scale to explain this difference. A U.S. start -up happens in a domestic market of 320 million potential customers. In Switzerland, an emerging company has to deal with a much smaller market, divided into three languages and twenty- six cantons.

This article was produced as part of a tour organized by BCV for ten young Vaudois.

A new report on venture capital brings interesting conclusions and updates. Here is the summary that you can also fidn on the Nesta web site:

1. The returns performance of UK and US VC funds in recent years has been very similar. UK funds have historically underperformed US funds, but this gap has significantly narrowed. The gap in fund returns (net IRR) between the average US and UK fund has fallen from over 20 percentage points before the dotcom bubble (funds raised in 1990-1997) to one percentage point afterwards (funds raised in 1998-2005). However, this convergence has been driven by declining returns in the US after the burst of the dotcom bubble, rather than by increasing returns in the UK. Average returns for funds raised after the bubble in both the UK and the US have been relatively poor, but VC performance is likely to move upwards as VC funds start to cash out their investments in social networks (particularly in the US).

2. The wider environment in which UK funds and the companies they finance operate was a major contributor to the historical gap in VC returns. While there are some large differences in the observable characteristics of VC funds between both countries, they cannot account for the historical returns gap.

3. Average returns obscure the large variability in returns within countries. The dispersion in returns across funds was highest during the pre-bubble years, and has fallen significantly since then. But in both periods the gap in returns between good and bad performing funds within a country was much larger than the gap in the average returns across countries. Thirteen per cent of UK funds established since 1990, would have got into the top quartile of US funds by returns (this has increased to 22 per cent for funds established in the post bubble period), while 45 per cent of UK funds outperformed the median US fund. Selecting the right fund manager is thus more important than choosing a particular country.

4. The strongest quantifiable predictors of VC returns performance are

(a) whether the fund managers’ priorfunds outperform the market benchmark;

(b) whether the fund invests in early rounds;

(c) whether the fund managers have prior experience; and

(d) whether the fund is optimally sized (neither too big nor too small).

Moreover, historical performance has been higher for funds located in one of the four largest investor hubs (Silicon Valley, New York, Massachusetts and London) and for investments in information and communication technology.

5. UK government-backed funds have historically underperformed their private counterparts, but the gap between public and private returns has narrowed in recent periods. This suggests that in later years governments have become savvier when designing new VC schemes.

Most US funds have traditionally only invested locally, with less than a third of US funds raised between 1990 and 2005 having invested in one or more companies outside the US.In contrast, the majority of European funds have invested outside of their home market.

The situation has changed somewhat in recent times. A higher proportion of European funds raised in 2006-2009 have chosen to invest locally while US-based funds are becoming more global. As a result, the proportion of European VC capital being invested in the US has halved, falling to 10 per cent, and a slightly larger share of US VC capital is coming to Europe.

Overall, this analysis suggests that Europe does not offer an attractive proposition to US VC funds. Europe has a less developed VC market than the US, so attracting US funds (their money but also, crucially, their expertise) ought to benefit European economies. Instead, the opposite is happening. A much larger share of European VC funds invest in the US than the other way around. While Europe is likely to benefit from its funds investing in the US (for the returns it provides, the network it builds and the experience it generates), the small flow in the opposite direction is a cause for concern.

In conclusion

– The global venture capital industry is concentrated in very few hubs (and does not exist in a vacuum)

– The convergence in returns is not the result of changes in the characteristics of UK funds

– Small funds underperform medium sized funds, but larger is not always better

– More experienced fund managers achieved higher returns

– Past performance predicts future performance

– Funds in investor hubs had better returns

Investing in earlier rounds leads to better performance

– But much of the variability in returns is not explained by these factors

Finally some advice on Policy:

Remember venture capital activity does not exist in a vacuum.

Resist the temptation to overengineer public support schemes

There is a lot of interesting content and if you have the time, listen to the full roundtable. It’s a good summary of our current or maybe complexity crisis. I do not agree with all arguments, for example the ones saying Europe is weak because of regulations. I believe it’s cultural. But probably, regulations change culture over the long term.

I noticed the usual-suspect arguments:

– You need a culture of rivalry and competition.

– You need money which means smart capital.

– We need an education to build (products and companies) not only academic skills.

– You need to be international from day one and not local only, so do not be modest. The topic of language was seen as much as an asset as a liability for Europe.

Esther Dyson is quite convincing in our need for the skills to build company. “In Europe, your mother tells you to work for SAP or Coca Cola.” Then she added it’s easy to create a 5-people company but it is tough to scale to 1’000 and there you need middle managers and skills. You may read Esther Dyson directly in her own post The Dangerous Myth of the Hero Entrepreneur. As important, Esther Dyson shows it is a complex topic.

As she nicely wrote in her post:

“But there are two benefits that do redound to a hero entrepreneur’s home country. First, the local entrepreneur serves as a role model. He (rarely she) encourages people to dream – and also to take risks, persist in the face of long odds, and generate economic activity.

(…)

Yet sometimes I think this hero-entrepreneur myth is dangerous. In an economy such as the United States, where start-ups are revered, people who would make perfectly good project supervisors or salespeople establish their own companies, starving the ecosystem of middle managers. Thousands of perfectly smart and highly useful people feel inadequate because they are not heroes. Many make the wrong career choices in search of glory.

(…)

In cultures where start-ups are considered risky and not quite honorable, it’s also hard for entrepreneurs to find troops to play the non-starring roles. Most people would rather work for an established company, or for the government.

So, rather than focusing on the supposed shortage of entrepreneurs, consider for a moment the very real shortage of qualified people willing to work for them.”