When I read that Nassim Nicholas Taleb said this is “one of the most important management books of all time”, I was intrigued. Usually I do not like general business books. But here, not only is it a great book, but fun to read!

What is the halo effect? A tendency to make inferences about specific traits on the basis of a general impression [Page 50].

The author has a major question: Is management a science? Pages 12-17 cover that sensitive topic: “In other fields, from medicine to chemistry to aeronautical engineering, knowledge seems to march ahead relentlessly. What do these fields have in common? In a word, these fields move forward thanks to a form of inquiry we call science. Richard Feynman once defined science as “a method for trying to answer questions which can be put into the form: If I do this, what will happen?” Science isn’t about beauty or truth or justice or wisdom or ethics. It’s eminently practical. It asks, If I do something over here, what will happen over there? If I apply this much force, or that much heat, or if I mix these chemicals, what will happen? By this definition, What leads to sustained profitable growth? is a scientific question. It asks, If a company does this or that, what will happen to its revenues or profits or share price?” [Page 12]

“Our inability to capture the full complexity of the business world through scientific experiments has provided fodder for some critics of business schools. Management gurus Warren Bennis and James O’Toole, in 2005 Harvard Business Review article, criticized business schools for their reliance on the scientific method. They wrote: “This scientific model is predicated on the faulty assumption that business is an academic discipline like chemistry or geology when, in fact, business is a profession and business schools are professional schools – or should be”. The notion seems to be that since business will never be understood with the precision of the natural sciences, it’s best understood as a sort of humanity, a realm where the logic of scientific inquiry doesn’t apply. Well, yes and no.” [Page 14]

Rozenzweig concludes this 1st chapter with a beautiful story (page 16), again from Richard Feynman: In the South Seas, there is a cult of people. During the war they saw airplanes land with lots of materials, and they want the same thing to happen now. So they’ve arranged to make things like runways, to put fires along the sides of the runways, to make a wooden hut for a man to sit in, with two wooden pieces on his head like headphones and bars of bamboo sticking out like antennas – he’s the controller. And they wait for the airplanes to land. They’re doing everything right. The form is perfect. But it doesn’t work. No airplanes land. So I call these things Cargo Cult Science, because they follow all the apparent precepts and forms of scientific investigation, but they’re missing something essential, because the planes don’t land. He called that last section Science, Pseudoscience and Coconut Headsets.

Storytelling and science

His criticism in chapter 6 of famous bestsellers In Search of Excellence by Peters and Waterman [page 83] and then of Built to Last by Collins and Porras [page 94] are particularly striking. Stories and science are different and the author explains many delusions created by approximate science:

#1: The Hallo Effect

#2: The delusion of Correlation and Causality

#3: The Delusion of Single Explanations

#4: The Delusion of Connecting the Winning Dots

#5: The Delusion of Rigorous Research

#6: The Delusion of Lasting Success

#7: The Delusion of Absolute Performance

#8: The Delusion of the Wrong End of the Stick

#9: The Delusion of Organizational Physics.

(if you are too lazy to read this great book, have at least a look at https://en.wikipedia.org/wiki/The_Halo_Effect_(business_book))

Rosenzweig tries to explain the complexity of measuring company performance. What are the key elements that managers should take into account for excellence? And Rosenzweig shows that storytelling has been as important as research in that quest. He further claims that authors of bestsellers such as In Search of Excellence, Built to Last or From Good to Great who claim their results were based on research, indeed were more excellent story tellers than rigorous researchers.

“It’s not that the important elements are not right. In Search of Excellence gives eight best practice: a bias for action; staying close to the customer; autonomy and entrepreneurship; productivity through people; hands-on, value-driven; stick to the knitting; simple form, lean staff; and simultaneous loose-tight properties.” [Page 85]

“Whereas in Built to Last, Collins and Porras give their 5 timeless principles: having a strong core ideology; building a strong corporate culture; setting audacious goals; developing and promoting people; creating a spirit of experimentation and risk-taking; driving for excellence”. [Page 96]

“Several researchers have studied the rate at which company performance changes over time. Pankaj Ghemawat at Harvard Business School examined the return on investments (ROI) of a sample of 692 American companies over a ten-year period from 1971 to 1980. He put together one group of top performers, with an average ROI of 39 percent, and one group of low performers, with an average ROI of just 3 percent. Then he tracked the two groups over time. What would happen to their ROIS? Would the gap persist, would it grow, or would it diminish? After nine years, both groups converged together toward the middle, the top performers falling from 39 percent to 21 percent and the low performers rising from 3 percent to 18 percent.” [Page 104]

“These studies, and others like them, all point to the basic nature of competition in a market economy. Competitive advantage is hard to sustain. Sure, if you want to, you can look back over seventy years of business history and pick out a handful of companies that have endured, but that’s selection based on outcomes.” [Page 105]

“Interviews with managers, asking them to look back over the ten-year period and recount their experiences (…) these sort of retrospective interviews are likely to be full of halos, as people take cues from performance and make attributions accordingly.” [Page 108]

Again Rosenzwieg has nothing against interviews, he just warns the reader that they have to be meticulously prepared to avoid any bias and answers based on outcomes.

“Another famous study, the Evergreen project, identified eight practices: strategy; execution; culture; structure; talent; leadership; innovation; and mergers and partnerships (Page 110). Yet once we see that performance is relative, it becomes obvious that companies can never achieve success simply by following a given set of steps, no matter how well intended; their success will always be affected by what rivals do” [Page 116].

“Perhaps the most interesting factor in Big Winners and Big Losers is mentioned as a brief aside but not examined closely: Marcus points out that large companies show up more frequently among the Big Losers, while almost all the Big Winners are small or midsize companies. This observation ought to spark one’s curiosity, because large companies got that way in the first place by doing things well – they didn’t grow by being Losers – yet something seemed to prevent them from maintaining that high performance. Extremer performance, for better and for worse, is more common among small companies”. [Page 132]

But a 10 percent difference in performance doesn’t say anything about what will happen at my company – the impact could be more or less or nothing at all. There’s no guarantee, no promise that inspires me to take action. Books, which provide simple and definitive advice and studies of organizational performance, stand in two very different worlds. The first world speaks to practicing managers and rewards speculations about how to improve performance. The second world demands and rewards adherence to rigorous standards of scholarship. Here science is paramount, storytelling less so. The result is a schizophrenic tour de force in which the demands of the roles of the consultant and teacher are disassociated form the demands of the researcher”. [Page 135]

“According to the Economist, Tom Peters can charge corporate clients up to $85,000 for a single appearance, and Jim Collins commands a fee of $150,000. There’s a lucrative market for spinning stories of corporate success. Will anyone hire (a researcher) at $85,000 or $150,000 a pop to talk about a statistically significant 4 percent difference in performance? Somehow it seems doubtful [page 136].

The test of a good story is not whether it is entirely, fully, scientifically accurate – by definition it won’t be. Rather, the test of a good story is whether it leads us toward valuable insights, if it is inspires towards helpful action, at least most of the time. [Page 137]

Strategy and execution

“Here’s how I like to think about company performance. According to Michael Porter of Harvard Business School, company performance is driven by two things: Strategy and execution.” [Page 144]

But both are full of uncertainties: “Strategy always involves risk because we don’t know for sure how our choices will turn out. […] A first reason has to do with customers. […] Sam Philips, the legendary Sun records producer, once cautioned, “Anytime we think you know what the public’s going to want that’s when you know you’re looking at a damn fool when you’re looking in the mirror”. Market reaction is always uncertain, and smart strategists know it. [Page 146]

“A second source of risk has to do with competitors. […] An entire branch of economics, game theory, has grown up around a simple form of competitive intelligence. […] A third source of risk comes from technological change. […] In his groundbreaking research Clayton Christensens at Harvard Business School showed that in a wide range of industries, from earth-moving equipment to disk drives to steel, successful companies were repeatedly dislodged by new technologies. [Page 147]

Jim Collins expressed surprised that [his] eleven Great companies came from ordinary, unspectacular industries. […] I suspect a different interpretation. These industries can be described as dowdy, but a better word might be stable. They were less subject to radical changes in technology, were less susceptible to shifts in customer demand, and may have had less intense competition. [Page 147]

As James March of Stanford and Zur Shapira of New York University explained, “Posthoc reconstruction permits history to be told in such a way that “chance”, either in the sense of genuinely probabilistic phenomena or in the senses of unexplained variation, is minimized as an explanation.” But chance does play a role, and the difference between a brilliant visionary and a foolish gambler is usually inferred after the fact, an attribution based on outcomes. [Page 150]

There are fewer unknowns […], yet execution still involves a number of uncertainties. [Page 151] And that brings us to the best answer I can provide to the question, What leads to high performance? If we set the usual suspects of leadership and culture and focus and so on – which are perhaps causes of performance – we’re left with two broad categories: strategic choice and execution. The former is inherently risky since it’s based on our best guesses about customers, about competitors, and technology, as well as about our internal capabilities. The latter is uncertain because best practices that work well on one company may not have the same effect in another. […] Wise managers know that business is about finding ways to improve the odds of success – but never imagine that success is certain. If a company makes strategic choices which are shrewd, works hard to operate effectively, and is favored by Lady Luck, it may put some distance between itself and its rivals, at least for a time. But even those profits will tend to erode over time. [Page 156]

The answer to the question what really works? is simple: Nothing really works. At least not all the time. […] So what can be done? A first step is to set aside the delusions that color so much of our thinking about business performance. To accept that few companies achieve lasting success. To admit that the margin between success and failure is often very narrow, and never quite as distinct or as enduring as it appears at a distance. And finally, to acknowledge that luck often plays a role in company success. [Page 158]

Rosenzweig finishes his book with examples of bold decisions from leaders at Goldman Sachs, Intel, BP, Logitech. Entrepreneurship inherently involves risks, but not doing anything would be much riskier.

As you noticed if you read my previous posts, I’ve been quite impressed by Peter Thiel’s notes about start-ups. I’ve written 7 long parts. I had been similarly impressed by Mariana Mazzucato’s The Entrepreneurial State even if with only 5 posts!

I said it already, I would have loved to attend their debate in a few days at the conference Human After All, Toronto 2014. But apparently they do not participate to the same roundtable anymore… (After reading what follows, I see that Taleb would have been a great addition).

– He will discuss “The Economics of Radical Uncertainty.”

How do human beings truly react when confronted with conditions of genuine “unknown unknowns”? According to Frank Knight, “Uncertainty must be taken in a sense radically distinct from the familiar notion of risk, from which it has never been properly separated…The essential fact is that ‘risk’ means in some cases a quantity susceptible of measurement, while at other times it is something distinctly not of this character; and there are far – reaching and crucial differences in the bearings of the phenomena depending on which of the two is really present and operating… It will appear that a measurable uncertainty, or ‘risk’ proper, as we shall use the term, is so far different from an unmeasurable one that it is not in effect an uncertainty at all.” The economics literature from Knight onward is very good at laying out the propensity of markets to greatly overshoot and undershoot the fundamentals. However, economics does not adequately address the implications of “Knightean” uncertainty, because the discipline finds it hard to model this phenomenon. To get a full measure of this, one has to enter into the realm of psychology and neuroscience. That’s where the definition lies. Radical uncertainty, like so much else, is too important to be left to the realm of economics alone.

– She will be part of “Innovation: Do Private Returns Produce the Social Returns We Need?”

The machines of the first age replaced and multiplied the physical labour of humans and animals. The machines of the second age will replace and multiply our intelligence. The driving force behind this revolution will, argue the “techno-positivists,” exponentially increase the power (or exponentially reduce the cost) of computing. The celebrated example is Moore’s Law, named after Gordon Moore, a founder of Intel. For half a century, the number of transistors on a semiconductor chip has doubled at least every two years. But the information age has coincided with – and must, to some extent, have caused – adverse economic trends: stagnation of median real incomes; rising inequality of labour income and of the distribution of income between labour and capital; and growing long – term unemployment. Are the great gains in

wealth and material prosperity created by our entrepreneurs in and of themselves sufficient to produce desired social returns demanded in today’s world?

Start-ups are a great area to study the tension between individuals and society. A kind of chicken and egg situation… Indeed they might explain the growing gap between the USA and Europe in many dimensions. Mazzucato would be on the social side, Thiel closer to the individual. But do not see any provocative statement here. The thoughts of Thiel and Mazzucato are profound. I agree with most of what they say, disagree with smaller pieces, though most people could think their thinking can not be reconciled. I really think that combining their point of views is an interesting approach to what innovtaion really is…

PS (May 8, 2014): I just found that video of Thiel at SXSW.

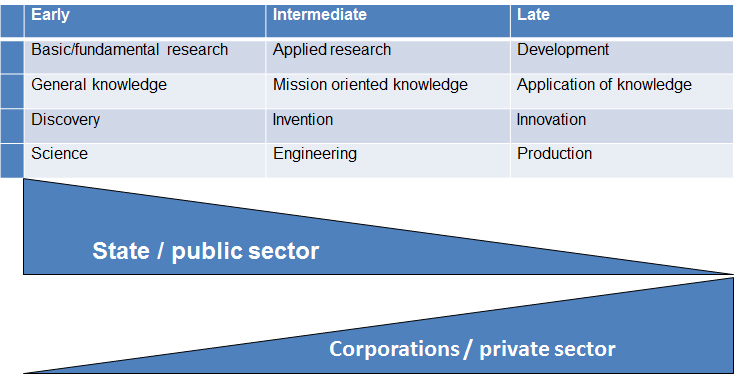

We agree on the issue of funding of technologies, inventions and innovations. It has been generally understood that the commercialization of products and their prior development is the responsibility of the private sector in a capitalist economy. The funding of research (at least basic research) is generally the mission of the state, but applied research (though I never really understood what this is) might be done by the State as well as by the private sector.

Let me open a short parenthesis here: I am not of big supporter of the concepts of basic and applied research, but I understand better other concepts from an early to later stage. Here they are:

Research has no known output a priori, except knowledge, whereas at a later stage the objectives are a little clearer. This being said, I am not fully comfortable about the arguments Mazzucato brings on the table when she says the State is doing a lot in innovation. But she clearly shows there is a grey zone between the 3 stages I have above. I belong (at least for now) to the group of people who believe it is the mission of the State to be active in the first two ones, and the private sector being in the third. Nothing forbids the private sector to go earlier and the public sector to be more active later, but it is seldom the case. Here are my notes on Chapters 3 and followings:

Chapter 3 – Risk-taking state : from « de-risking » to « bring it on ! »

During a visit of President Mitterand to Silicon Valley, Thomas Perkins which fund started Genentech extolled the virtues of the risk-taking investors who finance the entrepreneurs. Perkins was cut off by Stanford Professor and Nobel Prize Paul berg. He asked, “Where were you guys in the 50’s and 60’s when all the funding that had to be done in the basic science?” [Page 57]

Entrepreneurship, like growth, is one of the least-well understood topics in economics. According to Schumpeter, an entrepreneur is a person willing and able to convert a new idea or invention into a successful innovation (i.e. product, service or process). Entrepreneurship employs the “gale of creative destruction” to replace, in whole or in part, inferior innovations, simultaneously creating new products including new business models. Each major new technology leads to creative destruction. [Page 58]

[Again I need to react: where I fully agree with the Entrepreneurship and Innovation definitions, I am skeptical about the comment on technology: some major new technologies never destroyed anything because they were not commercially successful (artificial intelligence, speech recognition for example and there are many others). I would say major new successful innovations lead to creative destruction. This is important because as Mazzucato rightly says, there is no linear process for innovation and a lot of uncertainty too.]

Entrepreneurship is about risk and is highly uncertain. R&D investments that contribute to technological change not only take years to materialize into new products, but most products developed fail. Silicon Valley model tells a story of “freewheeling entrepreneurs and visionary venture capitalists and yet misses the crucial factor: the military’s role in creating and sustaining it. [Mazzucato shows the same issues in Pharma where the big players develop me-too drugs and let the State fund radical innovations in universities, as is shown in the anecdote above with Mitterand, Perkins and Berg.]

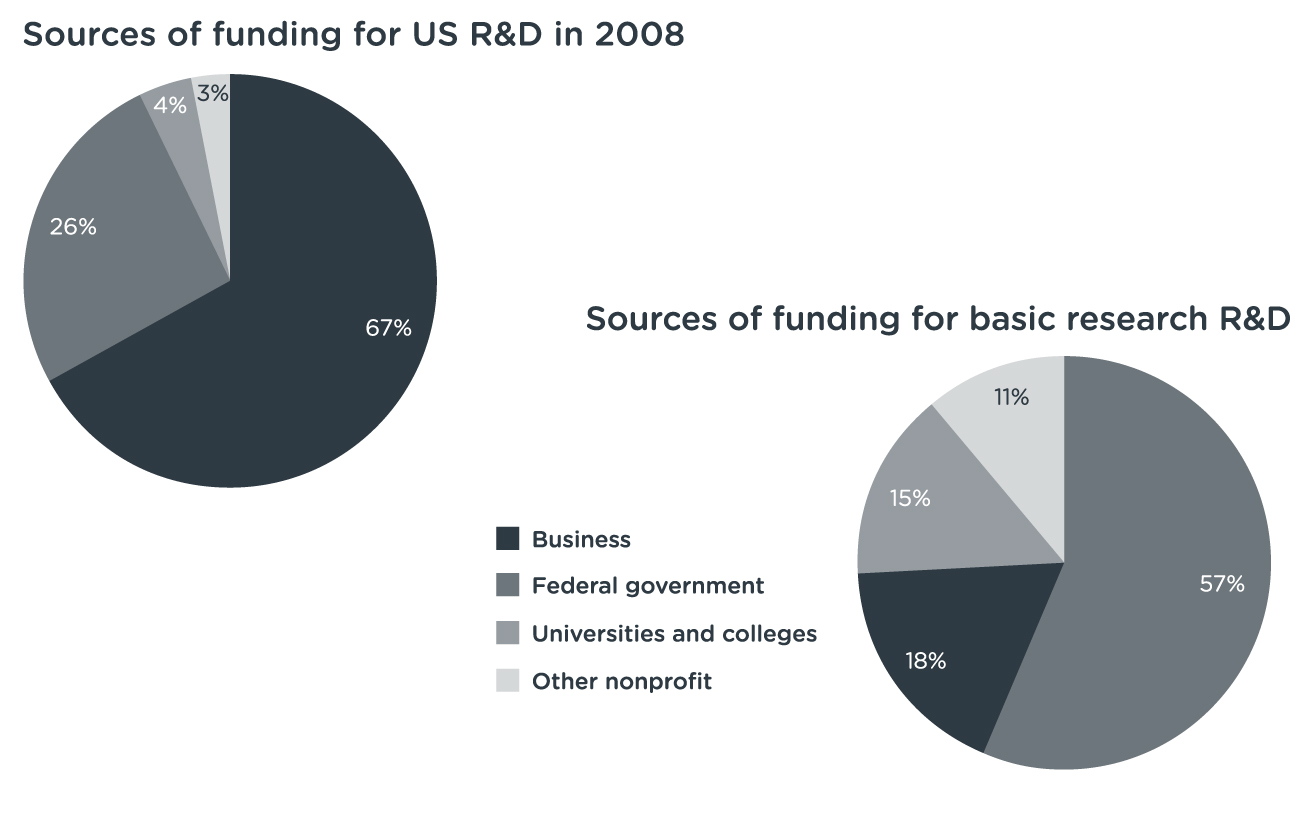

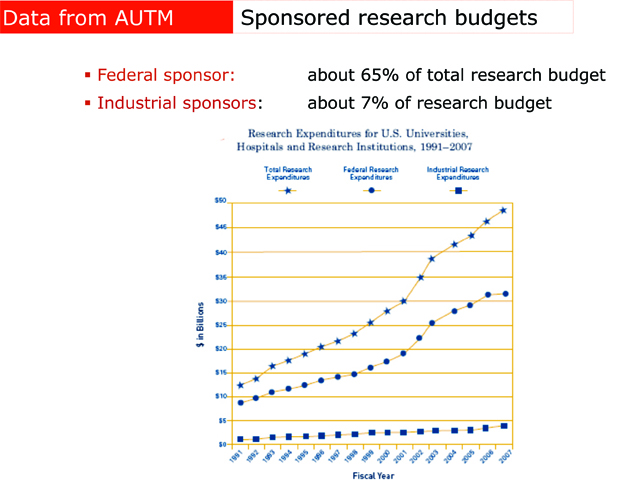

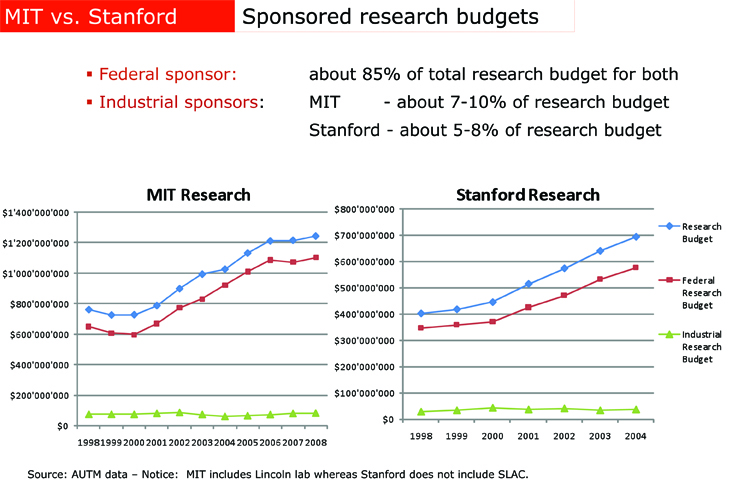

Again, I have some concerns with this decription. First in the image above, I would have liked to see the R vs. D and not only the fundamental R vs global R&D. Mazzucato is right in the funding of research, no doubt about it. I used such data for many years where the funding of research in universities by the industry is 4-7% whereas the federal funding is around 60%! You can look at Figures 1 and 2 below. But then, when it comes to innovation, I do not see where the State produced the biotech or IT industry. It made inventions available. You still needed the visionary entrepreneurs and investors as I told about in the Genentech case on my blog a few years ago [see Bob Swanson & Herbert Boyer: Genentech and Robert Swanson, 1947-1999]

Figure 1: Federal and Industry funding of university research in the USA.

Figure 2: Federal and Industry funding of research at Stanford University and MIT.

Chapter 4 – The US entrepreneurial state.

In this short chapter, Mazzucato shows through four examples how the US government fostered innovation. These are DARPA (the funding of American research by the military), SBIR (The Small Business Innovation Research), Orphan Drugs and Nanotechnologies.

On Darpa, “A series of small offices, staffed with leading scientists, are given considerable budget autonomy, … funding a mix of university-based researchers, start-ups, established firms and consortia… helping firms to get products to the stage of commercial viability”. [Page 78 ] Again the impact of DARPA in funding research is a no brainer. And Yes, I should be said. Mazzucato is right about too much silence on the role of the State. Check as a great reference Rebecca’s Lowen “Creating the Cold War University – the Transformation of Stanford”.

I am less convinced about the SBIR. “Government agencies designate a fraction of their research funding to support small, independent, for-profit firms.” Mazzucato claims Apple was funded with such a fund, Continental Illinois Venture Corp. but I checked Apple IPO document and CIVC was not at the origin of the company. Arthur Rock and Don Valentine convinced Markkula to help the two Steve and invested in January 1979. Even if CIVC invested that early, it was a minority and passive shareholder. Furthermore, CIVC was the VC arm of a bank, so not a purely State investment… She also quotes Lerner and Audretsch, leading professors as references. In a recent book (Boulevard of Broken Dreams – Pages 125-126), the same Lerner explains that the lack of flexibility of SBIR and ATP was detrimental (it had to be pre-commercial funding for ATP; start-ups had to be 51% owned by US citizens or residents, to the point that the presence of venture capital could exclude the firm from SBIR funding!) I have been struggling for years to find the real impact of SBIR and could never find convincing data of an important role. State direct role in VC funding has been a recurrent debate with unclear answers for years.

I do not know about orphan drugs, but I am skeptical about nanotechnologies. “Nanotechnology is very likely to be the next general purpose technology”. [Page 83] “It will be even more important than the computer revolution.” “Today it does not yet create a major economic impact because of the lack of commercialization of new technologies, due to the excessive investments made in research relative to the lack of investments in commercialization. […] This raises a question: if government has to do the research, fund major infrastructure investments and also undertake the commercialization effort, what exactly is the role of the private sector?” [Page 86]

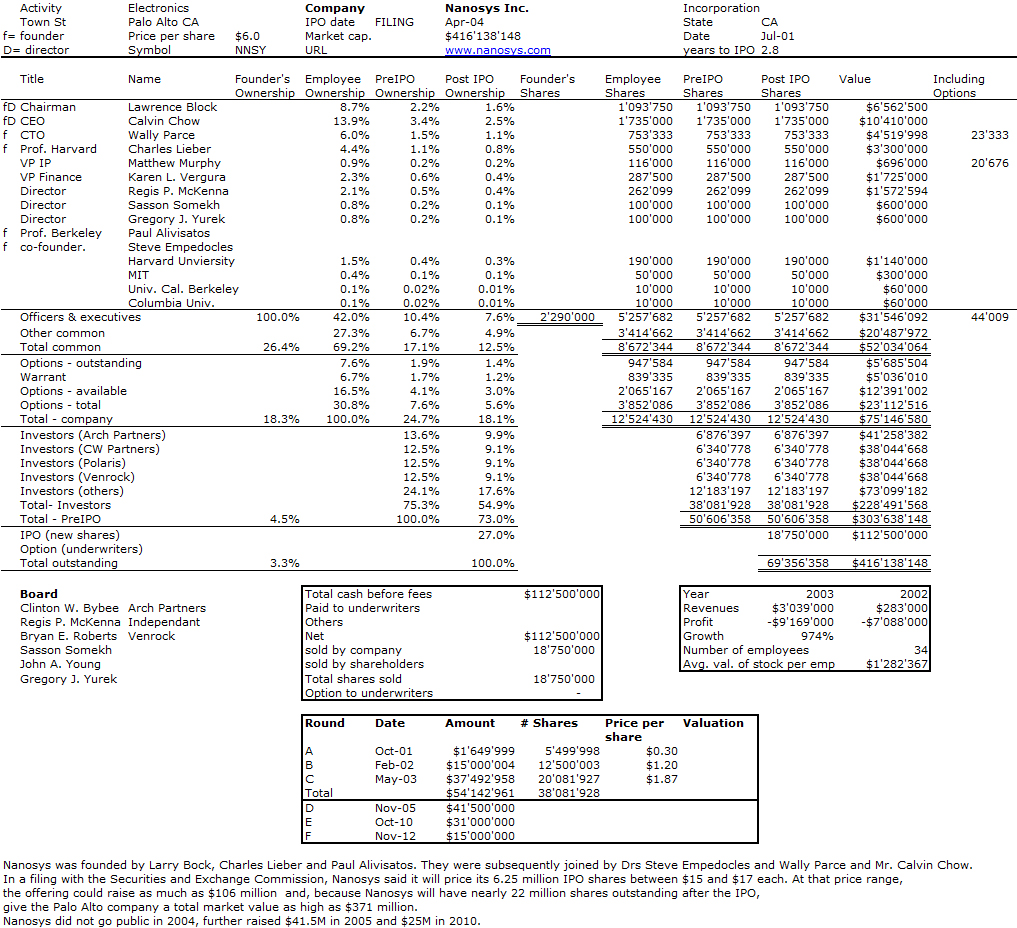

Well again many things are unclear and somehow contradictory in the arguments. If nanotechnology was just another low hanging fruit thanks to the State investment, we should have already seen early results. The US initiative on Nanotech was launched in 2000. There has been a very visible start-ups such as Nanosys or A123 to a lesser extent. Next is Nanosys cap. table as of 2004. One can read the then and additional funding from private sources.

I am now reading chapter 5 and will come back on Mazzucato’s book in a part 3!

Mazzacuto’s Entrepreneurial State is I think an important book. The author claims we have been unfair with the role in innovation of government and the public sector in general, which has provided funds for most not to say all R&D (Pharma, IT, Space). I share the blame as I am a strong supporter of start-ups, venture capital, Silicon Valley being the ultimate model. And the idea that the State should just provide the basics (education, research, infrastructure) and let the private sector innovate may have been a big mistake (of mine included). I will not take the blame on the second argument as I always shared with the author the idea that tax breaks and tax evasion makes the judgment even more unfair. Finally, the private sector is very risk averse so that there is less innovation (not only venture capital but corporate R&D, compared to the past when corporate R&D labs at IBM, Bell or Xerox were big or when VCs really contributed to innovation in semiconductor, computers and biotech in the 60s and 70s)

Let me now quote Mariana Mazzacuto following her book linearly. You can also listen to her when she gave a talk at TedX.

While innovation is not the State’s main role, illustrating its potential innovative and dynamic character – its historical ability, in some countries, to play an entrepreneurial role in society is perhaps the most effective way to defend its existence. (Page 1.)

Entrepreneurship is not (just) about start-ups, venture capital and “garage tinkerers”. It is about the willingness and ability of economic agents to take on risk and real Knightian* uncertainty, what is genuinely unknown. (Page 2.) Note: *Knightian uncertainty relates to the “immeasurable“ risk, i.e. a risk that cannot be calculated.

Even during a boom most firms and banks (would) prefer to fund low-risk incremental innovations, waiting for the State to make its mark in more radical areas. (Page 7.) Examples are provided from the pharmaceutical industry – where the most revolutionary new drugs are produced mainly with public, not private funds. (Page 10.)

Apple must pay tax not only because it is the right thing to do, but because it is the epicenter of a company that requires the public purse to be large and risk-taking enough to continue making the investments that entrepreneurs like Jobs will later capitalize on. (Page 11) Precisely because State investments are uncertain, there is a high risk that they will fail. But when they are successful, it is naive and dangerous to allow all the rewards to be privatized. (Page 12)

Chapter 1 – (The Innovation Crisis)

The emphasis on the State as an entrepreneurial agent is not of course meant to deny the existence of private sector entrepreneurship activity, from the role of young new companies in providing the dynamism behind new sectors (e.g. Google) to the importance source of funding from private sources like venture capital. The key problem is that this is the only story that is usually told. (Page 20)

It is naive to expect venture capital to lead in the early and most risky stage of any new economic sector today** (such as clean technology). In biotechnology, nanotechnology and the Internet, venture capital arrived 15-20 years after the most important investments were made by public sector funds. (Page 23) The State has been behind most technological revolutions and periods of long-term growth. This is why an “entrepreneurial” state is needed to engage in risk taking and the creation of a new vision. Note: ** Well maybe not in the 50s to the 70s, certainly in the last 10 years.

Big R&D labs have been closing and the R of the R&D spend has also been falling. A recent MIT study (1) claims that the current absence in the US of corporate labs like Xerox PARC (which produced the graphical user interface technology that led to both Apple’s and Windows’ operating systems) and Bell Labs – both highly co-financed by government agency budgets – is one of the reasons why the US innovation machine is under threat. (Page 24) Rodrik (2004) states that the problem is not in which types of tools (R&D, tax credits vs. subsidies) or which types of sectors to choose (steel vs. software), but how policy can foster self-discovery processes, which foster creativity and innovation – the need to foster exploration trial and error (and this is the core tenet of the “evolutionary theory of economic change” in chapter 2) References

[1] MIT 2013. Innovation Economic Report, web.mit.edu/press/images/documents/pie-report.pdf

[2] Rodrik, 2004. Industrial Policy for the 21st century. CEPR Discussion Paper 4767

Chapter 2 – Technology, Innovation and Growth.

Progressive redistribution policies are fundamental, but they do not cause growth. Bringing together the lessons of Keynes and Schumpeter can make this happen. (Page 31) Solow discovered that 90 per cent of variation in economic output was not explained by capital and labor, he called the residual “technical change”. (Page 33)

An “evolutionary theory” explains this as a constant process of differentiation among firms, based on their ability to innovate. Selection does not always lead to “survival of the fittest” both due to the effects of increasing returns and also to the effects of policies. Selection dynamics in products markets and financial markets may be at odds.

Innovation is firm specific and highly uncertain. It is not the quantity of R&D, but how it is distributed throughout an economy. The old view that R&D can be modeled as a lottery where a certain amount will create a certain probability of successful innovation is criticized because in fact innovation would be an example of a true Knightian uncertainty, which cannot be modeled with a normal (or nay other) probability distribution. (Page 35 – the Black Swan again)

Systems of innovation are defined as the “network of institutions in the public and private sector whose activities and interactions initiate, import, modify and diffuse new technology”. (Equilibrium theory cannot work; rather than using incremental calculus from Newtonian physics, mathematics from biology are used, which can explicitly take into account heterogeneity, and the possibility of path dependency and multiple equilibria.) (Page 36) The perspective is neither micro nor macro, but meso. The causation between basic science, to large scale R&D, to applications to diffusing innovation is not linear, but full of feedback loops. One must be able to recognize serendipity and uncertainty that characterizes the innovation process. […] Using Japan as an example, “the contributions of the development state in Japan cannot be understood in abstraction from the growth of companies such as Toyota, Sony or Hitachi aside from the Japanese State’s public support for industry”. (Page 38)

Regional systems of innovation focus on the cultural geographical, and institutional proximity that creates and facilitate transactions between different socioeconomic actors, including local administrations, unions and family-owned companies… The State does this by rallying existing innovation networks or by facilitating the development of new ones that bring together a diverse group of stakeholders. But a rich system of innovation is not sufficient. The State must develop strategies for technological advance.

Mazzacuto finishes Chapter 2 with 6 myths about innovation I totally agree with!

Myth 1: Innovation is about R&D. “It is fundamental to identify the company-specific conditions that must be present to allow spending on R&D to positively affect growth.”

Myth 2: Small is Beautiful. “There is confusion between size and growth.” What is important is the “role of young high-growth firms. Many small firms are not high-growth. […] Most of the impact is from age.” “Targeting assistance to SMES through grants, soft loans and tax breaks will necessarily involve a high degree of waste. While this waste is a necessary gamble in the innovation process,” it should be targeted on high growth and not SMEs, i.e. support “young companies that have already demonstrated ambition”.

Myth 3: Venture Capital is Risk-Loving. “Risk capital is scarce in the seed stage; it is concentrated in areas of high-growth potential, low technological complexity and low capital intensity.” […] “The short-term bias is damaging to the scientific exploration process which requires longer-term horizon and tolerance to failure.” “Rewards to VC have been disproportional to risks taken”, but Mazzacuto also recognizes that “Venture capital has succeeded more in the US when it provided not only committed finance, but managerial expertise.” Finally “The progressive commercialization of science seems to be unproductive”.

Myth 4: Patents. “The rise in patents does not reflect a rise in innovation”. [I will not come back here on the topic, read again Against Intellectual Monopoly]

Myth 5: Europe’s problem is all about Commercialization. “If the US is better at innovation, it isn’t because university-industry links are better (they aren’t) or because US universities produce more spinouts (they don’t). It simply reflects more research being done in more institutions, which generate better technical skills in the workforce. US funding is split between research in universities and early stage technology development in firms. Europe has a weaker system of scientific research and weaker and less innovative companies.”

Myth 6: Business Requires Less Tax. “The R&D tax credit system does not hold firms accountable as whether they have conducted new innovation that would not otherwise have taken place, or simply pursued routine forms of product development.” “As Keynes emphasized, business investment is a function of the gut instinct of investors about future growth prospects.” This is impacted not by tax break, but by the quality of the science base, education, credit system and human capital. “It is important for innovation policy to resist the appeal of tax measures of different kinds”.

More will follow when I have read chapters 3 and followings. Now I need to share some of my concerns, first by quoting again:

“Entrepreneurship by the State can take on many forms. Four examples: DARPA, SBIR, the Orphan Drug Act, Nanotechnology. (…) Apple is far from the “market” example it is often used to depict. It is a company that not only received early stage finance from the government (through the SBIC program) but also “ingeniously” made use of publicly funded technology*** to create “smart” products.” (Pages 10-11) Note: *** Internet, GPS, Touch screen, Siri.

“Many of the most innovative young companies in the US were funded not by private venture capital but by public venture capital, such as that provided by the Small Business Innovation Research (SBIR) program.” (Page 20)

My concerns are that

– research is not innovation & the transfer is where entrepreneurship occurs so that investing in research is not innovating or even being entrepreneurial. This is at least my experience in the field.

– SBIR real impact unclear

– Green and nano-tech impact also unclear

But I have not finished reading yet…

I have already talked about statistics here, and not in good terms. It was mostly related to Nicholas Nassim Taleb‘s works, The Black Swan and Antifragile. But this does not mean statistics are bad. They may just be dangerous when used stupidly. It is what Charles Wheelan explains among otehr things in Naked Statistics.

Naked Statistics belongs to the group of Popular Science. Americans often have a talent to explain science for a general audience. Wheelan has it too. So if you do not know about or hate the concepts of mean/average, standard deviation, probability, regression analysis, and even central limit theorem, you may change your mind after reading his book.

Also you will be explained the Monty Hall problem or equivalent Three Prisoners problem or why it is sometimes better (even if counterintuitive) to change your mind.

Finally Wheelan illustrates why statistics are useless and even dangerous when the data used are badly built or irrelevant (even if the mathematical tools are correctly used!). Just one example in scientific research (which is another topic of concern to me) “This phenomenon can plague even legitimate research. The accepted convention is to reject a hypothesis when we observe something that would happen by chance only 1 in 20 times or less if the hypothesis were true. Of course, if we conduct 20 studies, or if we include 20 junk variables in a single regression equation, then on average, we will get 1 bogus statistically significant finding. The New York Times magazine captured this tension wonderfully in a quotation from Richard Peto, a medical statistician and epidemiologist: “Epidemiology is so beautiful and provides such an important perspective on human life and death, but an incredible amount of rubbish is published”.

Even the results of clinical trials, which are usually randomized experiments and therefore the gold standard of medical research, should be viewed with some skepticism. In 2011, the Wall Street Journal ran a front-page story on what it described as one of the “dirty little secrets” of medical research: “Most results, including those that appear in top-flight peer-reviewed journals, can’t be reproduced. […] If researchers and medical journals pay attention to positive findings and ignore negative findings, then they may well publish the one study that finds a drug effective and ignore the nineteen in which it has no effect. […] On top of that, researchers may have some conscious or unconscious bias, either because of a strongly held prior belief or because a positive finding would be better for their career. (No one ever gets rich or famous by proving what doesn’t cure cancer. […] Dr. Ionnadis [a Greek doctor and epidemiologist] estimates that roughly half of the scientific papers published will eventually turn out to be wrong.” [Pages 222-223]

I am not sure how many posts I wrote on Taleb’s Black Swan. Whatever, I was asked by EPFL to add a contribution to its relationship with start-ups. This is my eighth contribution on start-ups to the EPFL web site. Here it is:

08.05.13 – What do natural disasters and unusually successful high-tech businesses have in common? They are both statistical outliers, and they both have outsized impact. This is the concept of the “Black Swan.”

The concept of Black Swan was created by Nassim Nicholas Taleb in his works on risk and randomness and popularized by a best-seller published in 2007 and sold over 3 million copies! Taleb explains the concept of Black Swan as follows: “There are two very distinct classes of statistics. The first defines the Mediocristan, the second defines the Extremistan. Without going into much detail, the Mediocristan exceptions occur, but don’t carry large consequences. Add the heaviest person on the planet to a sample of 1000. The total weight would barely change. In Extremistan, exceptions can be everything (they will eventually, in time, represent everything). Add Bill Gates to your sample: the total wealth may increase by a factor of 10,000. The first kind is of “Gaussian-Poisson” nature with thin tails, the second kind is of “fractal” or Mandelbrotian nature, with fat tails. But note here an epistemological question: there is a category of “I don’t know” that I also bundle in Extremistan – simply because I don’t know much about the probabilistic structure or the role of large events.” The Black Swans are unknown events, in Extremistan. These events are rare, very rare, unpredictable and have a huge impact. Ironically, we tend to rationalize them afterwards. The fall of the Berlin Wall, the events of September 11th, the Fukushima accident are examples of Black Swans.

The world of high-tech entrepreneurship is particularly well described with the concepts of Taleb. We have hundreds of start-ups in Switzerland. Thousands of start-ups are founded each year around the world. But a small number grows and survives. An even smaller number will become a great success. Logitech, Swissquote, Actelion in Switzerland. But if it were only about that kind of success, using the concept of Black Swan here would be misleading. Google and Apple are two real Black Swans. The extent of the success of these two former start-ups was simply unpredictable. Many authors have tried to rationalize the success after the fact, but failed, I think. Apple market capitalization is about twice as large as any other company. Steve Jobs, an unlikely entrepreneur, founded it in 1976 at the age of 21 and even more incredibly, he saved it from disaster with his comeback in 1997. Read the new book “I’m Feeling Lucky” on Google’s first steps and you will understand the extraordinary exceptionality of its two founders, Sergei Brin and Larry Page. Google is less than 15 years old, counts more than 50,000 employees and has nearly $40B in revenue.

Taleb is very controversial and provocative. He denounces the excesses of the statistical discipline, which sometimes makes us believe in the elimination of risks. He hates the “wisdom” of scholars to the point of attacking them personally. I remember a conference where the president of the session “blamed” my great passion for high-tech start-ups which according to him is only a fraction of firms. I did not try to hide my bias, but simply pointed out to him that their impact is far from being marginal and also that the field is fascinating in the difficulty in anticipating the potential success. Passion sometimes has to prevail over reason…

Taleb drove the nail with the publication last November of Antifragile, which is subtitled “things that gain from disorder.” This book is a multifaceted, sometimes messy, work, praising the artisan, the souk and the experimenter; he also criticizes the expert, often worn because too rational. Again Taleb’s ideas fit perfectly with innovation. “The fragility of every start-up is necessary for the economy to be antifragile, and that’s what makes, among other things, entrepreneurship work: the fragility of the individual entrepreneurs and their necessarily high failure rate.”

The Black Swan may have a quite simple explanation. It often has its roots in the weaknesses (for disasters) and genius (for the wonders) of the human species. Albert Einstein, Leonardo da Vinci, Steve Jobs and Lionel Messi are creators of genius. It is possible to quantify through science and technology many phenomena, but it is still difficult to measure human capabilities. Black Swans would probably not be as unpredictable if they did not have their root in the human interference in nature.

Here’s probably one of the toughest post I ever had to write and I am not sure it is a good one, even if the topic I am addressing is great and important. But it’s been a challenge to summarize what I learnt: Nicholas Nassim Taleb gives in this follow-up to the Black Swan a very interesting analysis of how the world can be less exposed to Black Swans, not by becoming more robust only, but by becoming antifragile, i.e. by benefiting from random events. His views include tensions between the individual and the groups, how distributed systems are more robust than centralized ones, how small unites are less fragile than big ones. This does not mean Taleb is against orgamizations, governments or laws as too little intervention induces totally messy situations. It is about putting the cursor at the right level. Switzerland represents for Taleb a good illustration of good state organizations with little central government, a lot of local responsibility. He has similar analogies for the work place, where he explains that an independent worker, who knows well his market, is less fragile to crises than big corporations and their employees. One way to make systems less fragile is to put some noise, some randomness which will stabilize them. This is well-known in science and also in social science. Just remember Athens was randomly nominating some of its leaders to avoid excess!

You can listen to Taleb here:

Now let me quote the author. These are notes only but for serious reviews, visit the author’s website, www.fooledbyrandomness.com/. First Taleb is, as usual, unfair but maybe less than in the Black Swan. Here is an example: “Academics (particularly in social science) seem to distrust each other, […] not to mention a level of envy I have almost never seen in business… My experience is that money and transactions purify relations; ideas and abstract matters like “recognition” and “credit” warp them, creating an atmosphere of perpetual rivalry. I grew to find people greedy for credentials nauseating, repulsive, and untrustworthy.” [Page 17] Taleb is right about envy and rivalry but wrong in saying it is worse in academia; I think it is universal! In politics for example. But when money is available, maybe rivalry counts less than where there is little.

Now a topic close to my activity: “This message from the ancients is vastly deeper than it seems. It contradicts modern methods and ideas of innovation and progress on many levels, as we tend to think that innovation comes from bureaucratic funding, through central planning, or by putting people through a Harvard Business School class by one Highly Decorated Professor of Innovation and Entrepreneurship (who never innovated anything) or hiring a consultant (who never innovated anything). This is a fallacy – note for now the disproportionate contribution of uneducated technicians and entrepreneurs to various technological leaps, from the Industrial Revolution to the emergence of Silicon Valley, and you will see what I mean.” [Page 42] [Extreme and unfair again, even if not fully wrong!]

“The antifragility of some comes necessarily at the expense of the fragility of others. In a system, the sacrifices of some units – fragile units, that is, or people – are often necessary for the well-being of other units or the whole. The fragility of every start-up is necessary for the economy to be antifragile, and that’s what makes, among other things, entrepreneurship work: the fragility of the individual entrepreneurs and their necessarily high failure rate”. [Page 65] What surprised me later is that Taleb shows that this is true of restaurants (not many succeed) as much as of high-tech start-ups. So it is not only about the uncertainty of new markets, but about uncertainty above all.

Mathematics of convexity

I have to admit Taleb is not easy to read. Not because it is complex (sometimes his ideas are pure common sense), but because it is dense with different even if consistent ideas. The book is divided in 25 chapters, but also in 7 books. In fact, Taleb insists on it, he might have written 7 different books! Even his mathematics is simple. His definition of convexity is a little strange though I found it interested (I teach convex optimization, and you might not know, it was the topic of my PhD!).

Jensen inequality is interesting [Pages 342, 227 – Jensen was an amateur mathematician!]– the convex transformation of a mean is less or equal than the mean after convex transformation. Again individual (concave, we die) vs. collective (convex, antifragile, benefits from individual failures). So risk taking is good for collectivity if with insurance mechanisms. Risk taking + insurance vs. speculation with no value added. An example of a short and deep idea: “Decision making is based on payoffs, not knowledge”. [Page 337]

“Simply, small probabilities are convex to errors of computation. One needs a parameter, called standard deviation, but uncertainty about standard deviation has the effect of making the small probabilities rise. Smaller and smaller probabilities require more precision in computation. In fact small probabilities are incomputable, even if one has the right model – which we of course don’t.” [Taleb fails to mention Poincare yet he quoted him in the Black Swan, but whatever.]

A visible tension between individual and collective interests

Quotes again: “What the economy, as a collective, wants [business school graduates] to do is not to survive, rather to take a lot, a lot of imprudent risks themselves and be blinded by the odds. Their respective industries improve from failure to failure. Natural and nature-like systems want some overconfidence on the part of the individual economic agents, i.e., the overestimation of their chances of success and underestimation of the risks of failure in their business, provided their failure does not impact others. In other words, they want local, but not global overconfidence”. […] In other words, some class of rash, even suicidal, risk taking is healthy for the economy – under the conditions that not all people take the same risks and that these risks remain small and localized. Now, by disrupting the model, as we will see, with bailouts, governments typically favor a certain class of firms that are large enough to require being saved in order to avoid contagion to other businesses. This is the opposite of healthy risk taking; it is transferring fragility from the collective to the unfit. […] Nietzsche’s famous expression “what does not kill me makes me stronger” can be easily implemented as meaning Mithridatization or Hormesis but it may also mean “what did not kill me did not make me stronger, but it spared me because I am stronger than others; but it killed others and the average population is now stronger because the weak are gone”. […] This visible tension between individual and collective interests is new in history. […] Some of the ideas about fitness and selection are not very comfortable to this author, which makes the writing of some sections rather painful – I detest the ruthlessness of selection, the inexorable disloyalty of Mother Nature. I detest the notion of improvement thanks to harm to others. As a humanist, I stand against the antifragility of systems at the expense of individuals, for if you follow the reasoning, this makes us humans individually irrelevant. ” [Pages 75-77]

A National Entrepreneur Day

“Compare the entrepreneurs to the bean-counting managers of companies who climb the ladder of hierarchy with hardly ever any real downside. Their cohort is rarely at risk. My dream – the solution – is that we would have a National Entrepreneur Day, with the following message: Most of you will fail, disrespected, impoverished, but we are grateful for the risks you are taking and the sacrifices you are making for the sake of the economic growth of the planet and pulling others out of poverty. You are the source of our antifragility. Our nation thanks you.” [Page 80]

Local distributed systems, randomness and modernity

“You never have a restaurant crisis. Why? Because it is composed of a lot of independent and competing small units that do not individually threaten the system and make it jump from one state to another. Randomness is distributed rather than concentrated.” [Page 98]

“Adding a certain number of randomly selected politicians to the process can improve the functioning of the parliamentary system.” [Page 104]

“Modernity is the humans’ large-scale domination of the environment, the systematic smoothing of the world’s jaggedness, and the stifling of volatility and stressors. We are going into a phase of modernity marked by the lobbyist, the very, very limited liability corporation, the MBA, sucker problems, secularization, the tax man, fear of the boss…” [Page 108]

“Iatrogenics means literally “caused by the healer”. Medical error still currently kills between three times (as accepted by doctors) and ten times as many people as car accidents in the United States, it is generally accepted that harm from doctors – not including risks from hospitals germs – accounts for more deaths than any single cancer. Iatrogenics is compounded by the “agency problem” which emerges when one party (the agent) has personal interested that are divorced from those of the one using his services (the principal). An agency problem is present with the stockbroker and medical doctor whose ultimate interest is their own checking account, not your financial and medical health.” [Pages 111-112]

Theories and intervention.

“Theories are super-fragile outside physics. The very designation “theory” is even upsetting. In social science, we should call these constructs “chimeras” rather than theories. [Now you understand why Taleb has many enemies.] A main source of the economic crisis started in 2007 in the Iatrogenics of the attempt by […] Alan Greenspan to iron out the “boom-bust” cycle which caused risks to go hide under the carpet. The most depressing part of the Greenspan story is that the fellow was a libertarian and seemingly convinced of the idea of leaving systems to their own devices; people can fool themselves endlessly. […] The argument is not against the notion of intervention; in fact I showed above that I am equally worried about under-intervention when it is truly necessary. […] We have a tendency to underestimate the role of randomness in human affairs. We need to avoid being blinded to the natural antifragility of systems, their ability to take care of themselves and fight our tendency to harm and fragilize them by not giving them a chance to do so. […] Alas, it has been hard for me to fit these ideas about fragility within the current US political discourse. The democratic side of the US spectrum favors hyper-intervention, unconditional regulation and large government, while the Republican side loves large corporations, unconditional deregulation and militarism, both are the same to me here. Let me simplify my take on intervention. To me it is mostly about having a systematic protocol to determine when to intervene and when to leave systems alone. And we may need to intervene to control the iatrogenics of modernity – particularly the large-scale harm to the environment and the concentration of potential (though not yet manifested) damage, the kind of thing we only notice when it is too late. The ideas advanced here are not political, but risk-management based. I do not have a political affiliation or allegiance to a specific party; rather, I am introducing the idea of harm and fragility into the vocabulary so we can formulate appropriate policies to ensure we don’t end up blowing up the planet and ourselves.” [Pages 116-118]

“To conclude, the best way to mitigate interventionism is to ration the supply of information. The more data you get, the less you know.” [Page 128]

“Political and economic “tail” events are unpredictable and their probabilities are not scientifically measurable.” [Page 133]

The barbell strategy and optionality

“The Barbell strategy is a way to achieve anti-fragility, by decreasing downside rather than increasing upside, by lowering exposure to negative Black Swans. So just as Stoicism is the domestication, not the elimination, of emotions, so is the barbell a domestication, not the elimination, of uncertainty.” [Page 159] “It is a combination of two extremes, one safe and one speculative, deemed more robust than a monomodal strategy. In biological systems, the equivalent of marrying an accountant and having an occasional fling with a rock star; for a writer, getting a stable sinecure and writing without the pressures of the market. Even trial and error are a form of barbell.” [Glossary page 428]

“The strength of the computer entrepreneur Steve Jobs was precisely in distrusting market research and focus groups – those based on asking people what they want – and following his own imagination, his modus was that people don’t know what they want until you provide them with it.” [Page 171]

“America’s asset is simply risk taking and the use of optionality, the remarkable ability to engage in rational forms of trial and error, with no comparative shame in failing, starting again and repeating failure. In modern Japan, by contrast, shame comes, with failure, which causes people to hide risks under the rug, financial or nuclear.”

“Nature does a California-style “fail early” – it has an option and uses it. Nature understands optionality effects better than humans. […] The idea is voiced by Steve Jobs in a famous speech: “Stay hungry, stay foolish.” He probably meant “Be crazy but retain the rationality of choosing the upper bound when you see it.” Any trial and error can be seen as the expression of an option, so long as one is capable of identifying a favorable result and exploiting it.” [Page 181]

“Option is a substitute for knowledge- actually I don’t understand what sterile knowledge is, since it is necessarily vague and sterile. So I make the bold speculation that many things we think are derived by skill come largely from options, but well-used options, much like Thales’s situation [who had an option with olive presses – pages 173-174] rather than from what we claim to be understanding.” [Page 186]

Taleb is skeptical with experts, with anyone believing in a linear model academia -> applied science ->practice (“lecturing birds how to fly”); he believes in tinkering, heuristics, apprenticeship, and makes again many enemies for free! He claims the jet engine, financial derivatives, architecture, medicine were first developed by practitioners and then theorized by scientists, not invented or discovered by them.

Tinkering vs. research

“There has to be a form of funding that works. By some vicious turn of events, governments have gotten huge payoffs from research, but not as intended – just consider the Internet. It is just that functionaries are too teleological in the way they look for things and so are large corporations. Most large companies, such as Big Pharma, are their own enemies. Consider blue sky research, whereby grants and funding are given to people, not projects, and spread in small amounts across many researchers. It’s been reported that in California, venture capitalists tend to back entrepreneurs, not ideas. Decisions are largely a matter of opinion, strengthened with who you know. Why? Because innovations drift, and one needs flâneur-like abilities to keep capturing the opportunities that arise. The significant venture capital decisions were made without real business plans. So if there was any analysis, it had to be of a backup, confirmatory nature. Visibly the money should go to the tinkerers, the aggressive tinkerers who you trust will milk the option.” [Page 229]

“Despite the commercial success of several companies and the stunning growth in revenues for the industry as a whole, most biotechnology firms earn no profit.” [Page 237] [Optionality again]

“(i) Look for optionality; in fact, rank things according to optionality, (ii) preferably with open-ended, not closed-ended, payoffs; (iii) do not invest in business plans but in people, so look for someone capable of changing six or seven times over his career, or more (an idea that is part of the modus operandi of the venture capitalist Marc Andreessen); one gets immunity from the backfit narratives of the business plan by investing in people. Make sure you are barbelled, whatever that means in your business.” [Page 238]

“I did here just debunk the lecturing-Birds-How-to-Fly epiphenomenon and the “linear model”, suing simple mathematical properties of optionality. There Is no empirical evidence to support the statement that organized research in the sense it is currently marketed leads to great things promised by universities. [Cf also Thiel lamentations about the promise of technologies – https://www.startup-book.com/2010/10/12/tech-equals-salvation/ ] Education is an institution that has been growing without external stressors; eventually the thing will collapse.” [A conclusion to book IV, page 261]

Why is fragility non linear?

“For the fragile, the cumulative effect of small shocks is smaller than the single effect of an equivalent single large shock. For the antifragile, shocks bring more benefits (equivalently, less harm) as their intensity increases (up to a point).”

Via negativa

“We may not need a name for or even an ability to express anything. We may just say something about what it is not. Michelangelo was asked by the pope about the secret of his genius, particularly how he carved the statue of David. His answer was: It’s simple, I just remove everything that is not David.” [Page 302-304]

[…] “Charlatans are recognizable in that they will give you positive advice. Yet in practice, it is the negative that’s used by the pros. One cannot really tell if a successful person has skills, or if a person with skills will succeed – but we can pretty much predict the negative, that a person totally devoid of skills will eventually fail.”

[…] “The greatest – most robust – contribution to knowledge consist in removing what we think is wrong. We know a lot more what is wrong than what is right. Negative knowledge is more robust to error than positive knowledge. […] Since one small observation can disprove a statement, while millions can hardly confirm it [The Black Swan!], disconfirmation is more rigorous than confirmation. […] Let us say that, in general, failure (and disconfirmation) are more informative than success and confirmation.”

[Funnily, I remember the main critics against my book were the lack of [positive] proposal in the end. I should have said there we many about what not to do!]

“Finally, consider this modernized version in a saying from Steve Jobs: “People think focus means saying yes to the thing you’ve got to focus on. But that’s not what it means at all. It means saying no to the hundred other good ideas that there are. You have to pick carefully. I’m actually as proud of the things we haven’t done as the things I have done. Innovation is saying no to 1,000 things.” [Page 302-304]

Less is more

“Simpler methods for forecasting and inference can work much, much better than complicated ones. “Fast and frugal” heuristics make good decisions despite limited time. First extreme effects: there are domains in which the rare event (good or bad) plays a disproportionate share and we tend to be blind to it. Just worry about Black Swan exposures and life is easy. There may not be an easily identifiable cause for a large share of the problems, but often there is an easy solution, sometimes with the naked eye rather than the use of the complicated analyses. Yet people want more data to solve problems.” [Page 305-306]

“The way to predict rigorously is to take away from the future, reduce from it things that do not belong to the coming times. What is fragile will eventually break, and luckily we can easily tell what is fragile. Positive Black Swans are more unpredictable than negative ones. Now I insist on the via negativa method of prophecy as being the only valid one.” [Page 310]

“For the perishable, every additional day in the life translates into a shorter additional life expectancy. For the non perishable, every additional day may imply a longer life expectancy. On general, the older the technology, the longer it is expected to last. I am not saying that all technologies do not age, only that those technologies that were prone to aging are already dead.” [Page 319]

“How can we teach children skills for the twenty-first century, since we do not know which skills will be needed? Effectively my answer would make them read the classics. The future is in the past. Actually there is an Arabic proverb to that effect: he who does not have a past has no future.” [Page 320]

[As can be read later in the book Taleb does not like the Bay Area culture. And it is no coincidence, it is a region with nearly no past, nearly no history, but it certainly help it create Silicon Valley innovations…]

“If you have an old oil painting and a flat screen television, you will never mind changing the television, not the painting. Same with an old fountain pen and the latest Apple computer; [Taleb is really cautious with modernity and innovation, even if a user of it. With architecture, he has similar concerns. Again he prefers tradition to aggressive modernity. Same with the metric system vs. old methods] Top-down is usually irreversible, so mistakes tend to stick, whereas bottom-up is gradual and incremental, with creation and destruction along the way, thought presumably with a positive slope.” [Pages 323-24]

“So we can apply criteria of fragility and robustness to the handling of information – the fragile in that context is, like technology, what does not stand the test of time. […] Books that have been around for ten years will be around for ten more; books that have been around for two millennia should be around for quite a bit of time. […] The problem in deciding whether a scientific result or a new “innovation” is a breakthrough, that is, the opposite of noise, is that one needs to see all aspects of the idea – and there is always some opacity that time, and only time, can dissipate.” [Page 329]

“Now, what is fragile? The large, optimized, overreliance on technology, overreliance on the so-called scientific method instead of age-tested heuristics.”

“By issuing warnings based on vulnerability – that is, substractive prophecy – we are closer to the original role of the prophet: to warn, not necessarily to predict, and to predict calamities if people don’t listen.”

Ethics

“Under opacity and complexity, people can hide risks and hurt others. Skin in the game is the only true mitigator of fragility. We have developed a fondness for neomanic complication over archaic simplicity. […] The worst problem of modernity lies in the malignant transfer of fragility and antifragility from one party to the other, with one getting the benefits, the other one (unwittingly) getting the harm, with such transfer facilitated by the growing wedge between the ethical and the legal. Modernity hides it especially well. It is of course an agency problem.” [Page 373]

[You can/should have a look at table 7, page 377]

“In traditional societies, a person is only respectable and as worthy as the downside he (or, more, a lot more, than expected, she) is willing to face for the sake of others.” [Page 376]

“I want predictors to have visible scars on their body from prediction errors, not distribute these errors to society.” [Page 386]

[Don Quixote was already the sign of the end of the heroism, of the ethical behavior. Taleb’s models are Malraux and Ralph Nader – “the man is a secular saint” [Page 394]. His enemies Thomas Friedman, Rubin and Stieglitz]

[Is “skin in the game” the only way? The only solution? What about transparency?]

About Science

“Science must not be a competition; it must not have rankings – we can see how such a system will end up blowing up. Knowledge must not have an agency problem. One doctoral student once came to tell me that he believed in my ideas of fat tails and my skepticism of current methods of risk management, but that it would not help him get an academic job. “It’s what everybody teaches and uses in papers” he said. Another student explained that he wanted a job at a good university, so he could make money testifying as an expert witness – they would not buy my idea on robust risk management because “everyone uses these textbooks”. [Page 419]

“All I want is to remove the optionality, reduce the antifragility of some at the expense of others. It is simple via negativa. […] The golden rule: “Don’t do unto others what you don’t want them to do to you”. […] Everything gains or loses from volatility. Fragility is what loses from volatility or uncertainty. […] Time is volatility. Education in the sense of the formation of the character, personality, and acquisition of true knowledge, likes disorder; label-driven education and educators abhor disorder. Innovation is precisely something that grains from uncertainty.” [Pages 420-22]

“It so happens that everything nonlinear is convex, concave or both. […] We can build Black-Swan-protected systems thanks to detection of concavity, […] and with a mechanism called convex transformation, the fancier name for the barbell. […] Distributed randomness (as opposed to the concentrated type) is a necessity.”

[General comments]

Taleb sometimes gives the feeling of contradictions: marketing is bad, but Steve Jobs is great; barbell strategy and optionality is great, but isn’t it about risks and downsides transferred to others [Isn’t Thales a pure speculator?], cigarettes are bad but traditions are good.

Also this love of tradition makes people with more background at ease to take risks with barbell strategy; but what about the poor with nothing to lose? Benefits might statistically go to those who already have… [It reminds the story told by J.-B. Doumeng: It is a millionaire who recounts his difficult beginnings: “I bought an apple 50 cents, I polished it to shine and I sold it for one franc. With this, I bought two apples 50cts, I carefully polished and I sold them 2 Fr after a moment, I could buy a cart to sell my apples and then I made a big inheritance … “]

You now know why it has been a challenge. A very strange, dense, fascinating book, but if you like these concepts, you must read Antifragile. In fact you must read the Black Swan first, if you have not and if you like it, I am sure you will read Antifragile.

If you understand French, you might be interested in how I explained the Black Swan on French-speaking radio broadcast Babylon on Espace 2. You just have to click on the picture. Many thanks to Jean-Marc Falcombello for the time he gave me to describe Taleb’s ideas. It is 19 minutes long – between 23:15 and 42:00.

“Thought is only a flash in the middle of a long night. But this flash means everything.”

Henri Poincaré*

When I talked to friends and colleagues about The Black Swan (“BS”), they were surprised about my interest in the movie with Natalie Portman. I cannot say, I have not watched it. I was talking about Nassem Nicholas Taleb’s book and theory. Some other friends classified at it as American b… s…, these superficial books that give advice on anything and that seem to always become bestsellers; my colleagues would classify it as airport literature, not to be read in academic circles.

I read it and enjoyed it, but I have to admit Taleb is sometimes painful. Is it because he was so much frustrated by I do not know whom or what or is it because he is so proud of his certainties? I am not sure. But his ideas are certainly worth thinking about more than a minute. (Whereas you forget about airport American b… s… after 30 seconds). So back to the BS.

You’ll find great accounts of his book or of his theory, e.g.

– Nassim Taleb’s “The Black Swan” by Andrew Gelman,

– The Wikipedia page on the Black Swan theory

– or even another essay by Taleb, the Fourth Quadrant,

so I will not try to do the same.

However defining the Black Swan might be useful! In the Fourth Quadrant, Taleb writes the following:

There are two classes of probability domains—very distinct qualitatively and quantitatively. The first, thin-tailed: Mediocristan”, the second, thick tailed Extremistan. Before I get into the details, take the literary distinction as follows: In Mediocristan, exceptions occur but don’t carry large consequences. Add the heaviest person on the planet to a sample of 1000. The total weight would barely change. In Extremistan, exceptions can be everything (they will eventually, in time, represent everything). Add Bill Gates to your sample: the wealth will jump by a factor of >100,000. So, in Mediocristan, large deviations occur but they are not consequential—unlike Extremistan. Mediocristan corresponds to “random walk” style randomness that you tend to find in regular textbooks (and in popular books on randomness). Extremistan corresponds to a “random jump” one. The first kind I can call “Gaussian-Poisson”, the second “fractal” or Mandelbrotian (after the works of the great Benoit Mandelbrot linking it to the geometry of nature). But note here an epistemological question: there is a category of “I don’t know” that I also bundle in Extremistan for the sake of decision making—simply because I don’t know much about the probabilistic structure or the role of large events. Black Swans are the unknown deviations in Extremistan.

Here are more notes taken while reading.

[Page xxii] The black swan is characterized by “rarity, extreme impact and retrospective (though not prospective) predictability” (with additional footnote: the occurrence of a highly improbably event is the equivalent of the nonoccurrence of a highly probably one.

[Page 8] The human mind suffers from 3 aliments:

-The illusions of understanding, or how everyone thinks he knows what is going on in a world that is more complicated (or random) than they realize;

-the retrospective distortion, or how we can assess matters only after the fact, as if they were in a rearview mirror; and

-the overvaluation of factual information and the handicap of authoritative and learned people – when they platonify.

[Page 15] While in the past a distinction had been between drawn Mediterranean and non- Mediterranean (i.e., between the olive oil and the butter), in the 1970s, the distinction suddenly became between Europe and non-Europe.

[Page 54] There is a major difference and often-made mistake between no evidence of something and the evidence of its non-occurence (mental bias.)

[Page 77] The answer is that there are two varieties of rare events: a) the narrated Black Swans, those that are present in the current discourse and that you are likely to hear about on television, and b) those nobody talks about, since they escape models – those that you would feel ashamed discussing in public because they do not seem plausible. I can safely say that it is entirely compatible with human nature that the incidences of Black Swans would be overestimated in the first case, but severely underestimated in the second one.

[Page 80] One death is a tragedy; a million is a statistic. […] We have two systems of thinking. System 1 is experiential, effortless, automatic, fast, and opaque. System 2 is thinking, reasoned, local, slow, serial, progressive. Most mistakes come from using system 1 when we think we use system 2.

[Page 140] We overestimate what we know and underestimate uncertainty. Another bias, ”think about how many people divorce. Almost all of them are acquainted with the statistic that between one-third and one-half of all marriages fail, something the parties involved did not forecast while tying the know. Of course, “not us” because “we get along so well” (as if others tying the know got along poorly.)”

[Page 174-179] Poincaré is a central personality of Taleb’s theory, in particular through the 3-body problem. According to Taleb, “Poincaré angrily disparages the use of the bell curve.” Now the next figure simply illustrates the concept of sensitivity to initial conditions.

Predicting

Operation 1: imagine an ice cube and consider how it may melt.

Operation 2: consider a puddle of water. Try to reconstruct the shape of the ice-cube.

The forward process is generally used in physics and engineering, the backward process in nonrepeatable, nonexperimental historical approaches. And the backward is much more complex to analyze.

[Page 198] While in theory it is an intrinsic property. In practice, randomness is incomplete information. Nonpractitioners do not understand the subtlety. A true random process does not have predictable properties. A chaotic system has entirely predictable properties, but they are hard to know.

a) There are no functional differences in practice between the two since we will never get to make the distinction.

b) The mere fact that a person is talking about the difference implies he has never made a meaningful decision under uncertainty – which is why he does not realize that they are indistinguishable in practice.

Randomness in practice, in the end, is just unknowledge. The world is opaque and appearances fool us.

[Page 204] Trial and error means trying a lot. In the Blind Watchmaker, Richard Dawkins brilliantly illustrates this notion of the world without grand design, moving by small incremental random changes. Note a slight disagreement on my part that does not change the story by much: the world, rather moves by large incremental random changes. Indeed, we have psychological and intellectual difficulties with trial and error and with accepting that series of small failures are necessary in life. “You need to love to lose”. In fact the reason I felt immediately at home in America is precisely because American culture encourages the process of failure, unlike the cultures of Europe and Asia where failure is met with stigma and embarrassment. [It’s really Taleb writing and not the blog’s author, but I fully agree !]

[Page 207] When you have a very limited loss, you need to be as aggressive as speculative and sometimes as unreasonable as you can be. Middlebrow thinkers sometimes make the analogy with lottery tickets. It is plain wrong. First lottery tickets do not have a scalable payoff. Second, lottery tickets have known rules.

The economics of superstars

[Page 24] Who is this book written for? You need to understand who your audience is and amateurs write for themselves, professionals write for others. [This irony of the author’s is stimulating. I experienced it, I’m an amateur. But are the masterpieces not then written by amateurs? The Black Swans (The Lord of the Rings, Harry Potter) look often like a work of amateurs. The Yevgenia Krasnova example provided by Taleb is also stimulating]

[Page 214] Someone who is marginally better can easily win the entire pot. The problem is the notion of “better.” People take from the poor to give to the rich. An initial advantage follows someone through life and keep getting cumulative advantages. Failure is also cumulative. The advent of modern media has accelerated these cumulative advantages. The sociologist Pierre Bourdieu noted a link between the increased concentration of success and the globalization of culture and economic life.

[Page 221] Taleb claims new comers mitigate the cumulative advantages. “of the five hundred largest US companies in 1957, only seventy-four were still part of that select group, the S&P 500, forty year later. Only a few hundred had disappeared in mergers; the rest either shrank or went bust.

Actors who win an Oscar tend to live on average five years longer than their peers who don’t. People live longer in societies that have flatter social gradients.