I published a post about Figma in October 2022 when it was announced it would be acquired by Adobe for $20B. Here is the article. At the time I could not find official data about the startup and I built a cap. table based on public data available online (see at the bottow).

This morning I found a SEC filing document published in Nov. 2022 that I had not seen before, which says much more. So I built a revised cap. table and you can compare it also below close to the older one. They are not that different though. My motivation for looking for such a document is that Figma has confidentially filed for an IPO. So if it happens, updated numbers will emerge like fundrasising between 2022 and 2025, real revenues, profit (or loss) and employee count. Still I had to publish this revised version.

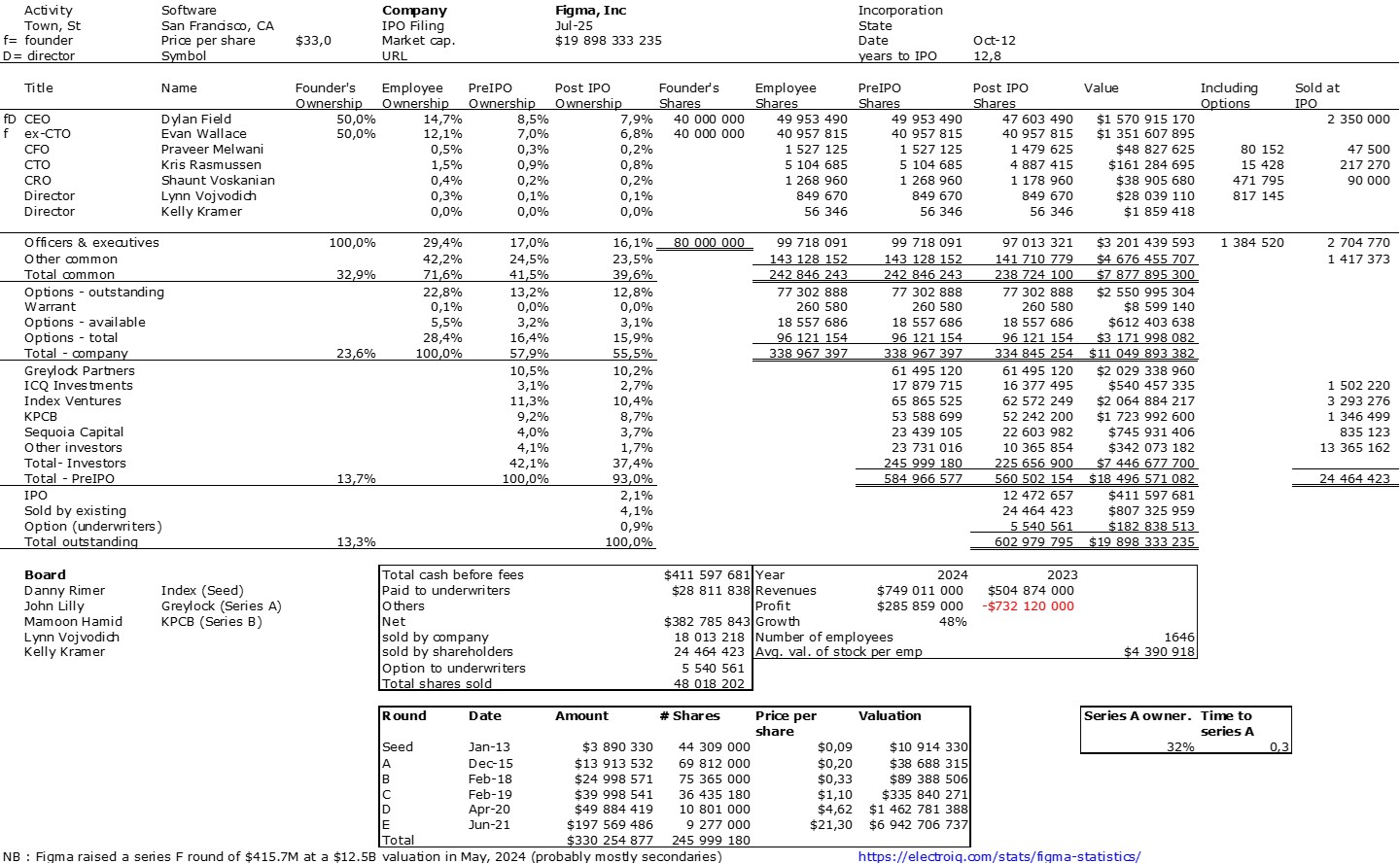

Figma cap. table as revised in July 2025

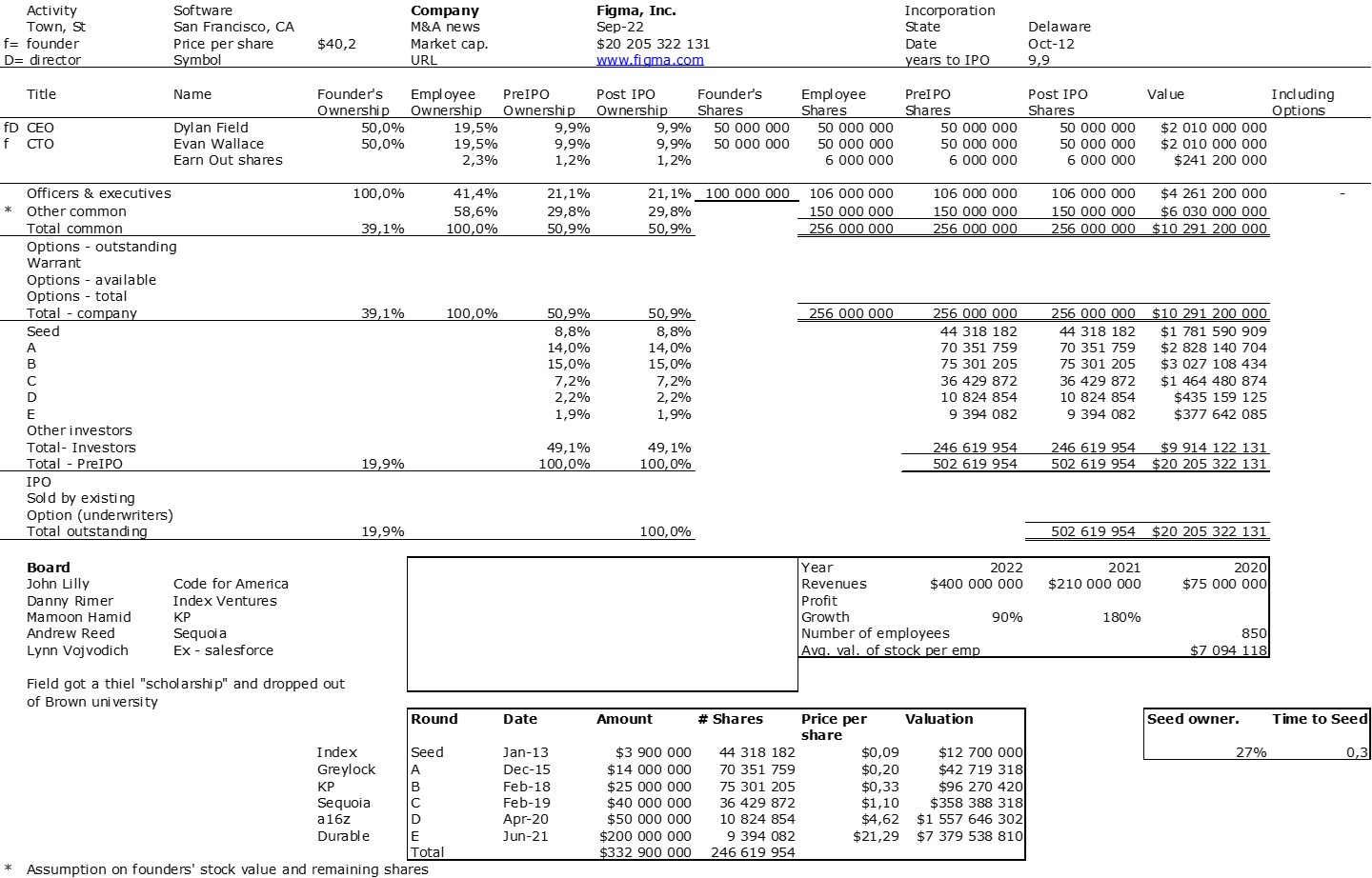

Figma cap. table estimated in October 2022

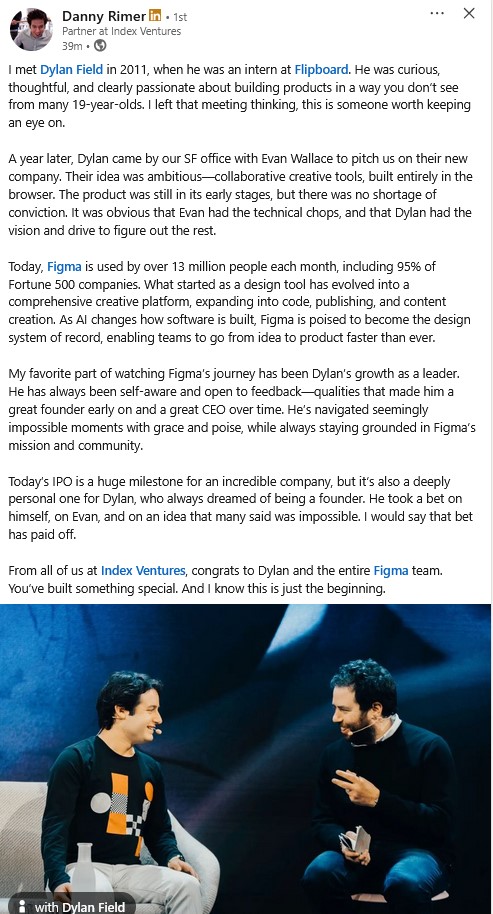

And cherry on the cake, a LinkedIn post by Danny Rimer :

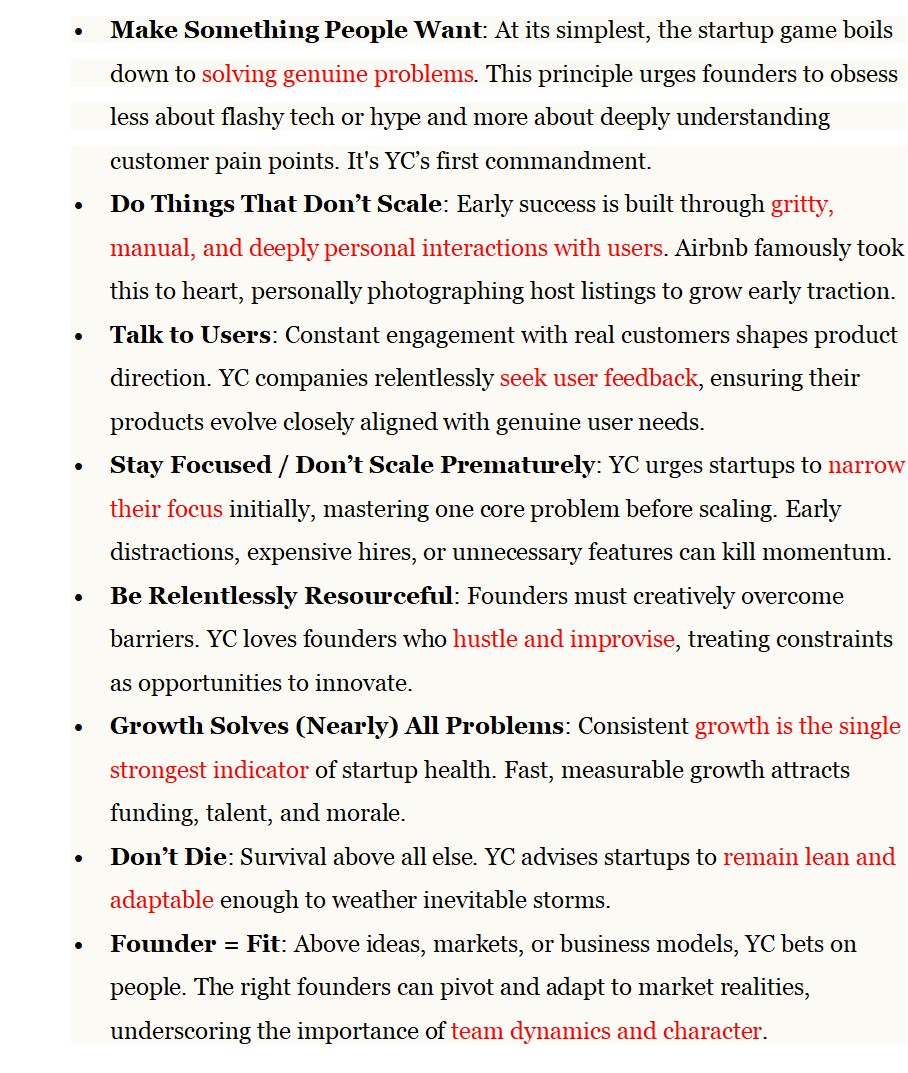

“Make something people want” Y Combinator (current) motto

What a shock to discover the briefing of Y Combinator “against” Google in the U.S.’s monopoly case against the search giant. The link is here and the pdf there:

I have been a fan of both entities for 20 years. But time flies and the world apparently changes. At the end of this post I will come back to the reasons why I have been impressed by Y Combinator over time and in particular the duo Jessica Livingston / Paul Graham.

In fact this article is more about Y Combinator. It could be that what I liked about Google is dead as it was hinted in Goomics. So no real need to talk about Google. I have done it so often with the tag #google. But I first need to describe shortly the accelerator’s arguments against Google.

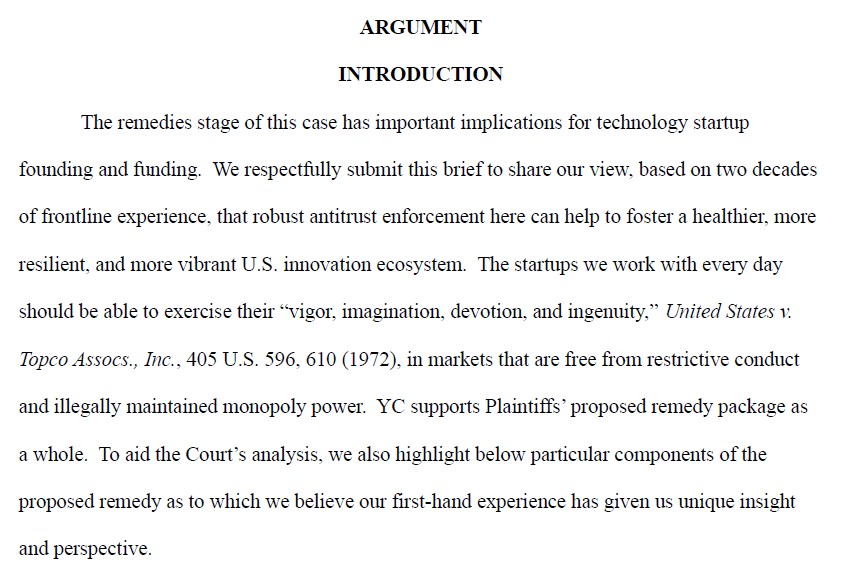

BRIEF OF Y COMBINATOR, LLC AS AMICUS CURIAE IN SUPPORT OF PLAINTIFFS

The remedies stage of this case has important implications for technology startup founding and funding. We respectfully submit this brief to share our view, based on two decades of frontline experience, that robust antitrust enforcement here can help to foster a healthier, more resilient, and more vibrant U.S. innovation ecosystem. The startups we work with every day should be able to exercise their “vigor, imagination, devotion, and ingenuity,” United States v. Topco Assocs., Inc., 405 U.S. 596, 610 (1972), in markets that are free from restrictive conduct and illegally maintained monopoly power. YC supports Plaintiffs’ proposed remedy package as a whole. To aid the Court’s analysis, we also highlight below particular components of the proposed remedy as to which we believe our first-hand experience has given us unique insight and perspective.

Anticompetitive measure have been constant in the history of the USA and the brief reminds it :

Experience has taught us that technological inflection points are critical moments for competition and innovation. The rise of novel, transformative technology can create an opening for nimble startups to disrupt established incumbents. […] Dominant incumbents often respond by using exclusionary conduct to try to slow down or coopt the future. […] For example, during the mid-1990s, Microsoft recognized the disruptive potential of web-based software applications and reacted by anticompetitively blocking rival internet browsers from reaching users. United States v. Microsoft Corp., 253 F.3d 34, 60 (D.C. Cir. 2001). More recently, Facebook recognized the explosion in usage of mobile applications and reacted by acquiring mobile-native startups that it viewed as competitive threats. See FTC v. Meta Platforms, Inc., No. CV 20-3590 (JEB), 2024 WL 4772423, at *29–30 (D.D.C. Nov. 13, 2024) (“[T]he case for buying Instagram focused heavily on neutralizing a competitive threat.”).

Antitrust remedies have a long track record of unlocking American dynamism and ingenuity. An antitrust consent decree in 1956, for example, required AT&T to provide open access to its patents and technical manufacturing information. That remedy order helped usher in the modern digital age, in large part because it enabled “young and small” firms—what we think of today as “little tech” companies—to compete. See Martin Watzinger et al., How Antitrust Enforcement Can Spur Innovation: Bell Labs and the 1956 Consent Decree, 12 AM. ECON. J. ECON. POL’Y 328, 330 (2020). A new generation was able to enter and expand in a multitude of markets, helping to vault the United States into position as the world’s leader in technological innovation. Id. Economists have called the 1956 antitrust decree “one of the most unheralded contributions to economic development” in history, and the co-founder of Intel called it “one of the most important developments for the commercial semiconductor industry.” This tradition has continued in the modern era. In 2022, for example, the U.S. Federal Trade Commission blocked Nvidia Corp.’s proposed acquisition of Arm Ltd., a semiconductor technology firm. Arm’s CEO later explained that the structural separation “helped us” focus on delivering better products at a time when “more applications [were] moving towards the cloud” and “AI [was] starting to raise its head.” An Interview with Arm CEO Rene Haas. Arm has since gone public on the Nasdaq stock exchange, delivered record revenues, and is now worth more than $100 billion. Meanwhile, Nvidia’s earnings have nearly quintupled as its chips helped to fuel the rise of generative AI technology.

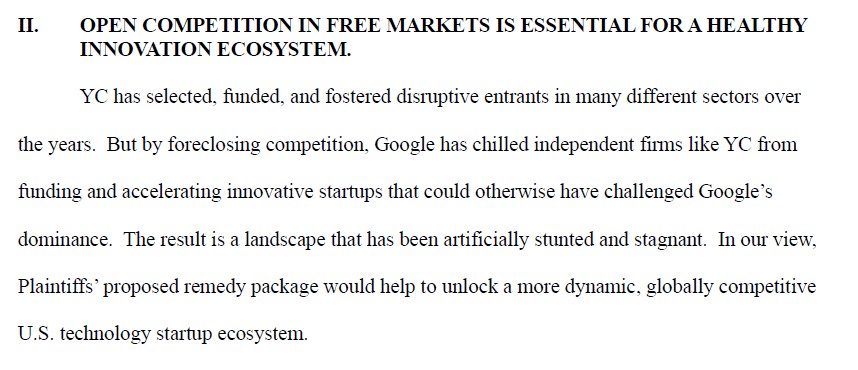

But by foreclosing competition, Google has chilled independent firms like YC from funding and accelerating innovative startups that could otherwise have challenged Google’s dominance. The result is a landscape that has been artificially stunted and stagnant. In our view, Plaintiffs’ proposed remedy package would help to unlock a more dynamic, globally competitive U.S. technology startup ecosystem.

Y combinator proposes the following remedies:

A. The Remedy Should Open Access to Google’s Datasets and Search Index.

B. The Remedy Should Prevent Google from Extending Its Monopolies into Query-Based AI Tools.

C. The Remedy Should Prevent Google From Entering Pay-to-Play Arrangements with Distributors.

D. The Remedy Order Should Deter Circumvention and Retaliation.

I’m not sure I understand all of this, but the implications would certainly be major. I will not go into more details, but for sure this is deep and quite fascinating.

First their philosophy is what mainly attracts me. And once again, this is linked to the people who founded it, in particular Paul Graham and Jessica Livingston. I will not count how many times Graham is quoted here, his essays are famous (I just counted 228 different articles since 2005) and in a way they are close to Montaigne’s. Just check one for example, The Two Kinds of Moderate.

As the article says, Jessica Livingston has an underrated role, “If Paul Graham was Y Combinator’s philosophical architect, Jessica Livingston was its social architect—quietly and effectively shaping YC’s culture and community from the earliest days.” If you have never heard of her, it is never to late to read Founders at Work. And indded Paul Graham felt the need to right an essay entitled Jessica Livingston 🙁

Their philosophy is simple and complex at the same time. Again read the article mentioned above and here are their “mantras, distilled from hard-earned experiences, are now part of global startup culture:

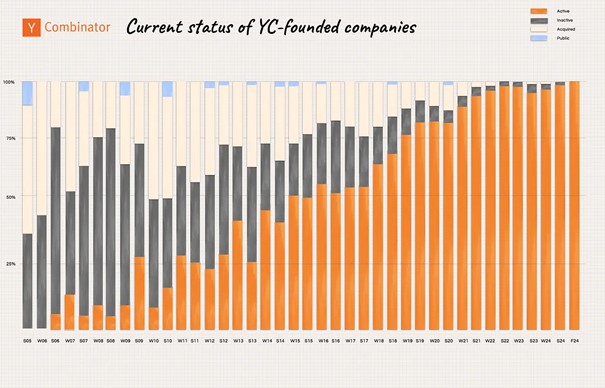

THE PERFORMANCE OF Y COMBINATOR

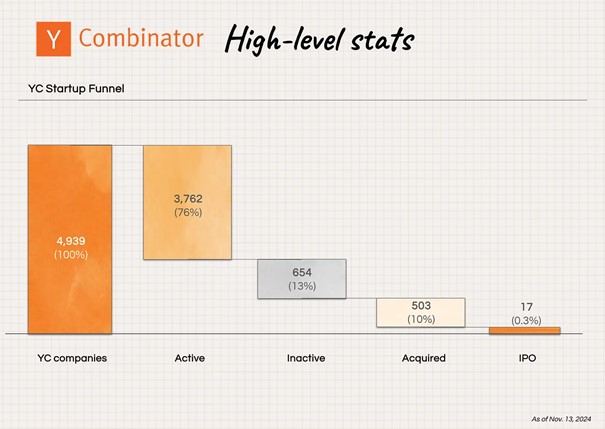

Don’t get me wrong. All this does not mean Y Combinator has found the recipe for success. Let met add just figures from the article:

You can have you own thoughts about these numbers. What I read is :

– out of 5000 startups, 17 went public (less than 1%) and about 500 were acquired (about 10%) and remember an acquisition can be at a very low value.

– not that many fail, particularly in the first years , so the “fail fast” mantra is not that obvious.

Is Y Combinator more sucessful than others. I do not know but I loved their approach to entrepreneurship.

ABOUT THE EVOLUTION AND DEATH OF INNOVATIVE ENTITIES

I just said “loved” and not “love”. I begin to feel that old structures lose their agility and creativity. It is what Y Combinator thinks of Google. I discovered that Graham and Livingston have retired from YC. I also believe that a culture is difficult to maintain when the founders leave. And I had a similar feeling with YC when Sam Altman & others began to lead it. There is somethind depressing about the comment but maybe not.

Death is very likely the single best invention of Life. It is Life’s change agent. It clears out the old to make way for the new. Right now the new is you, but someday not too long from now, you will gradually become the old and be cleared away. Sorry to be so dramatic, but it is quite true.

Your time is limited, so don’t waste it living someone else’s life. Don’t be trapped by dogma – which is living with the results of other people’s thinking. Don’t let the noise of others’ opinions drown out your own inner voice. And most important, have the courage to follow your heart and intuition. They somehow already know what you truly want to become. Everything else is secondary.

Excellent issue of FUTU&R, the magazine by Usbek & Rica, which main feature is entitled Silicon Valley, Chronicle of a Collapse. It’s not a good time to be a fan of the region these days. If you follow my blog, you’ve seen my struggles to understand what’s going on there. This issue contributes to this, and you’ll discover dubious characters like Curtis Yarvin, Balaji Srinivasan, Palmer Lucky, in addition to the famous Peter Thiel, Marc Andreessen, David Sacks, and even Larry Ellison. The issue is a bit biased, but that’s the name of the game, since the magazine “imagines how the Tech Eldorado could collapse.”

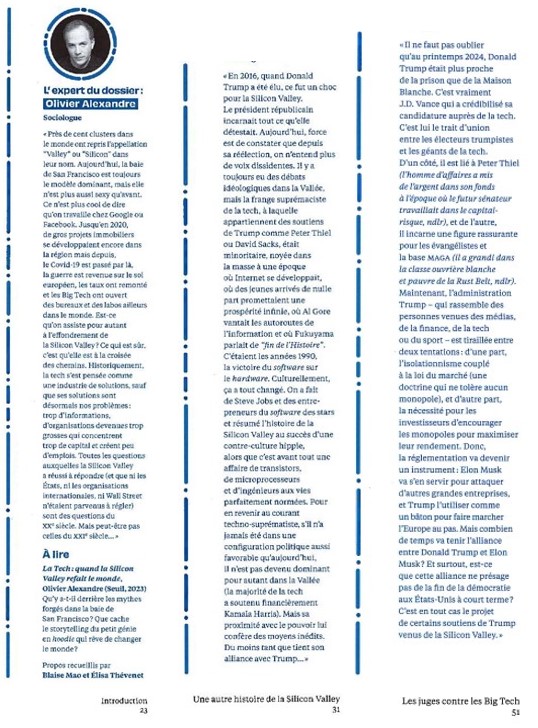

The magazine had the good idea to add the informed opinion of Olivier Alexandre, often mentioned on this blog, notably as the author of La Tech. I scanned the contributions in low resolution and I hope the magazine will forgive me for this breach of copyright. I obviously encourage you to buy a copy!

I will just comment on what Olivier Alexandre says and I will end this post by discussing a related subject through a fairly recent scientific article, The Role of Universities in Shaping the Evolution of Silicon Valley’s Ecosystem of Innovation (pdf)

“Are we witnessing the collapse of Silicon Valley? What is certain is that it is at a crossroads. Historically, tech has thought of itself as a solutions industry, except that its solutions are now our problems. […] It is clear that we no longer hear dissenting voices. There have always been debates in the Valley, but the tech supremacist fringe, to which Trump supporters like Peter Thiel and David Sacks belong, was a minority, drowned in the mass. […] Steve Jobs and software entrepreneurs have been made stars and the history of Silicon Valley has been reduced to the success of a hippie counterculture, when it is above all a story of transistors, microprocessors, and engineers with perfectly standardized lives.”

Indeed, the region was a republic of engineers, with back-and-forths between fierce competition in a global world and deregulation and occasional isolationism allowing monopolies. In the 1980s, the threat was Japan, and the semiconductor industry had appealed to the Federal State for its survival (after having benefited from the flow of public money at the height of the Cold War in the 1960s.) I recently spoke of my difficulty in finding dissenting voices too.

“In 2022, the situation changed and Big Tech started laying off employees. Since then, they’ve been cutting 5% of their payroll every year.”

On this point, I slightly disagree with the observation. In 2009 and 2013, for example, Google also reduced its workforce by 5%. I had heard that Cisco was shedding 5% of its “lowest-performing” workforce each year. The region was so dynamic that it was rarely discussed. Working conditions have always been “harsh and demanding.” A world of engineers, no doubt. It brought us computers and smartphones, the internet, and therefore opportunities to behave differently. It also contributed to creating immense biases because, without a doubt, the use of science and technology is never completely neutral.

“The question being asked of the world is the link between new technologies, innovation, and progress, which are three very different notions. Historically, innovations that have had a lasting impact are few: watches, eyeglasses, jeans… However, today, Silicon Valley mostly creates very ephemeral innovations.”

Tom Kleiner went further, mentioning the printing press, the steam engine, electricity, and finally the transistor as innovations that changed civilization. This is undoubtedly close to reality.

And Olivier Alexandre adds a beautiful question: “The products offered are essentially based on the promise of saving us time. But what do we lose when we save time?”

And he concludes (provisionally): “Dubai is one of the rare places that has managed to make the future sexy, an optimistic vision of the future: rain without clouds, islands without land, snow without mountains. But above all, technological progress without democracy. All this in a vulnerable area where the questions of resources, food, and housing have always arisen. In a way, Europe embodies the opposite: democracy, sometimes at the cost of technological progress.”

This isn’t the first time that the future of Silicon Valley has looked bleak. For example, you can find AnnaLee Saxenian’s predictions in a post titled Is Silicon Valley crazy (again)?: “In 1979, I was a graduate student at Berkeley and I was one of the first scholars to study Silicon Valley. I culminated my master’s program by writing a thesis in which I confidently predicted that Silicon Valley would stop growing. I argued that housing and labor were too expensive and the roads were too congested, and while corporate headquarters and research might remain, I was convinced that the region had reached its physical limits and that innovation and job growth would occur elsewhere during the 1980s. As it turns out I was wrong.”

There’s no doubt the region is at a new crossroads! But I’m not finished yet, see below.

I promised above to talk about a scientific article dating from 2020. I found its conclusion interesting even if overall the content well-known. So I copy paste :

Silicon Valley—a Metaphor in search of a Structure?

Silicon Valley is a metaphor for a region that lacks a viable governmental structure. It is at the stage of New York, before its 1989 consolidation into a unified city. With the notable exception of the ecology of the Bay, a downside has emerged, a public-private imbalance revealing gaps in housing and transportation Spread across multitudinous counties, towns and cities, Silicon Valley lacks sufficient governance capabilities to address the negative consequences of its overweening success.

An additional imbalance in academic capacities is, in part, a consequence of a more than half century old master plan strictly segmenting the public academic sphere that has limited individual institutional advancement. This gap has been partly redressed by establishment of branch campuses by universities in other parts of the country, like Carnegie Mellon and the Wharton School that ironically treat the region as an under-developed area, at least in its academic capabilities. Moreover, state government funding for public universities

has declined drastically, from providing 40% of Berkeley’s budget in the 1980’s to 14% percent at present. This gap is being redressed by a massive fund-raising campaign that expects to raise 6 billion dollars and increase the universities tenure track positions in coming years.

Re-balancing the Triple Helix will also require increased interaction among the spheres, a phenomenon that has declined in recent decades, placing the long-term innovation and carrying-capacity of the region at risk. The innovative and sustainable economic development of Silicon Valley not only depends on the presence of strong universities, but on how they interact and overlap roles with the other agents of the Triple Helix model, looking for mutually strategic objectives and identifying cross-cutting issues which none of them can adequately deal individually. Interactions between university, industry and government in a highly dynamic and volatile environment, represent a unique opportunity to recover from economic downturn, create new jobs, and promote a prolific, inclusive and economically sustainable development of regions in the long run.

Xavier Jaravel comes back in a column entitled “Let’s Not Forget the Lost Marie Curie(s)” for the newspaper Les Echos to one of his favorite topics: “Access to innovation depends heavily on social background, parental income, gender, and department of birth. With equal abilities, children from modest backgrounds have a much lower chance of becoming researchers, entrepreneurs, or inventors than those from privileged families.”

I was fortunate to be invited by the same IMF in January 2019 to analyze the sources of innovation. There, I discovered the similar concept of the Lost Einstein. A paper also co-authored by Xavier Jaravel and entitled Who Becomes an Inventor in America? The Importance of Exposure to Innovation provides a definition: There are many “lost Einsteins” – individuals who would have had highly impactful inventions had they been exposed to innovation in childhood – especially among women, minorities, and children from low-income families.

When I read analyses of the reasons for innovation failures, particularly in Europe, I see “rational and economic” explanations, such as overly strict regulations, uneven markets, inappropriate taxation, and inadequate investments. I hear fewer cultural or sociological reasons, which seem far more convincing to me. Xavier Jaravel helps highlight important and little-known elements. Thanks to him!

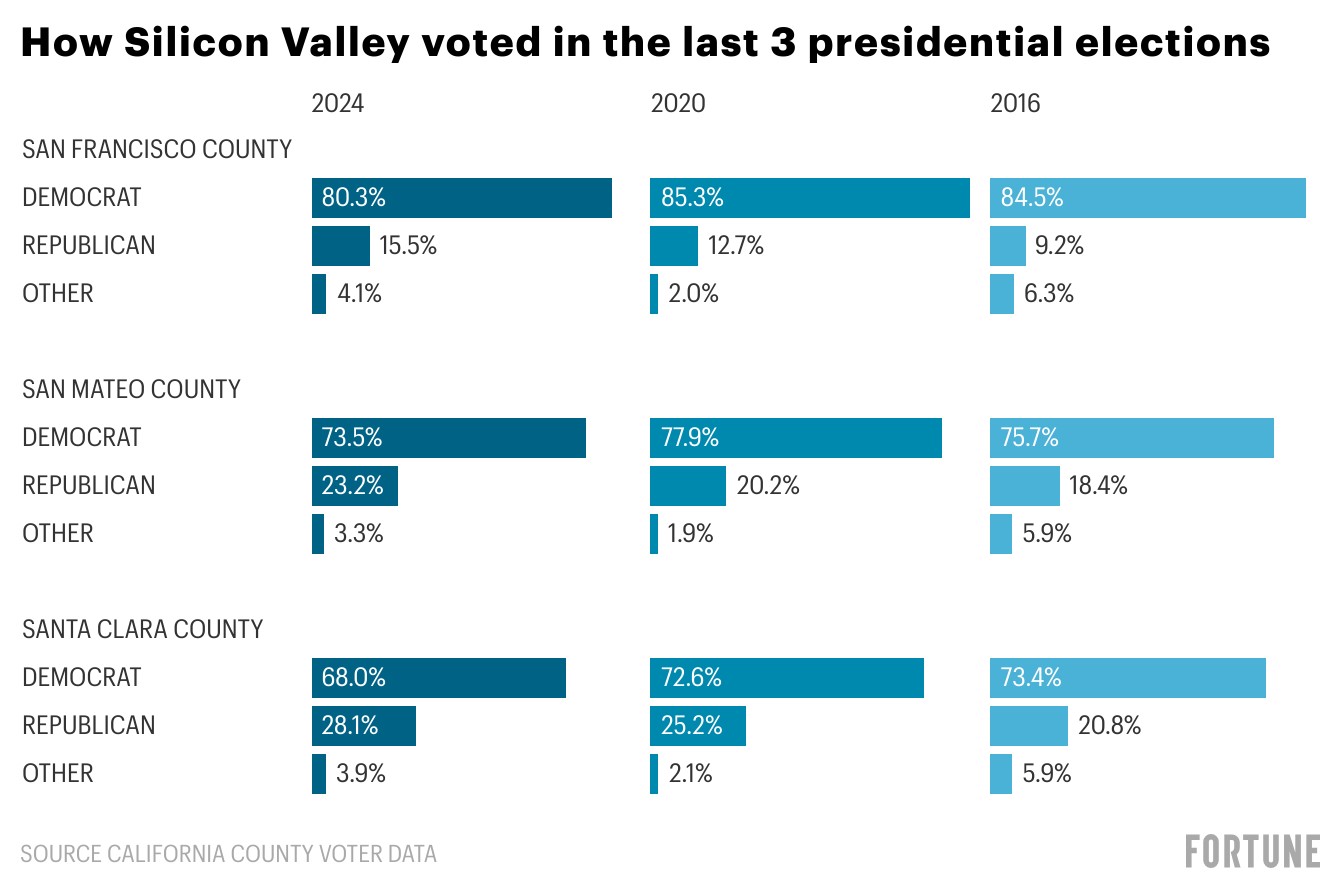

In recent weeks or months, I have been discovering with amazement or embarrassment that many people in Silicon Valley have apparently turned their backs to support Trump’s policies in the United States. It’s quite impressive, even if it’s not as impressive as we think. I already addressed the topic in July 2024, at a time when I believed Kamala Harris would be elected president. It was titled Politics and Silicon Valley. And I indeed discovered that former Democrat “sympathizers” were turning to Republicans such as Mark Zuckerberg, Sam Altman, or Marc Andreessen. Worse, it seems that even Sundar Pichai (CEO of Google) or Tim Cook (CEO of Apple) were going in the same direction. After all, in Europe, we are never shocked that a boss is right-wing and the least favored are left-wing. Again, you can reread my post on the subject. In reality, Silicon Valley is so Democrat in its voting that it was perhaps difficult to position oneself otherwise, and today, people position themselves more openly. Votes are also evolving as illustrated here.

So I asked myself the question: who is opposing Trump today in tech and Silicon Valley?

I was pleasantly surprised to find that there were figures like Bill Gates and Michael Moritz:

– Bill Gates is a moderate and not active politically. But I quote him from Bill Gates says he’s surprised about his fellow billionaires’ rightward political shift: ‘I always thought of Silicon Valley as being left of center’ : “The fact that now there is a significant right-of-center group is a surprise to me.” while “incredible things happened because of sharing information on the internet,” social media has had major downfalls. “You see ills that I have to say I did not predict,” While Gates is by no means an open Trump supporter, he said he’d do his best to work with the president. “I will engage this administration just like I did the first Trump administration as best I can,” Gates told the NYT.

– Michael Moritz is less well known, but given that he funded Google, Yahoo!, PayPal, Apple, Cisco, and YouTube, we can appreciate what he has to say in Trump’s tech backers are ‘making a big mistake,’Trump’s tech financiers and supporters were “making the same mistake as all powerful people who back authoritarians.” He wrote that wealthy financiers believe “they will be able to control Trump,” or else are committing “another cardinal error: deluding themselves that he will not do what he says or promises.” “That has not been the modus operandi of authoritarians over the centuries,”

Paul Graham, whom I respect, wrote an article on wokeness that deserves careful reading, but it’s not really an opposition to Trump; rather, it seeks to explain a movement. Please read The Origins of Wokeness. For example I’m not going to claim Trump’s second victory in 2024 was a referendum on wokeness; I think he won, as presidential candidates always do, because he was more charismatic; but voters’ disgust with wokeness must have helped. And “Trump and wokeness are cousins”.

Steve Blank is rather silent but I discovered that in 2020, that he resigned from a Department of Defense advisory board, protesting the Trump administration’s decision to oust most of his fellow board members and replace some of them with political loyalists with no defense or business experience. See here.

Who else? I’ve searched a bit in vain. My “heroes” are rather silent, but they always have been, so what can I conclude? Hopefully, some will wake up and dare to oppose them, whatever the cost…

PS: I found a little more, for example, Larry Page: “I intend to tell the president that we are with him and that we will help him in any way we can. If you can reform the tax code, reduce regulations and negotiate better trade agreements, the US technology industry will be stronger and more competitive than ever3, he would be quoted as saying by Andoidsis.

Roger McNamme is another investor: Well, everything about Trump seems like a payback, right? All these executives are giving a million dollars each. These are rounding spreads. This is money they find between the cushions of their living room couch. But, you know, this is essentially a precautionary payment. And in Musk’s case, the investment he made in Trump, which was a quarter of a billion dollars, or the investment he made in Twitter, which was about $44 billion, has paid off, obviously, many, many times over. I think Trump and Musk will eventually part ways. I don’t know Trump at all, but he doesn’t seem like the kind of guy who would support someone who competes on the same level as Musk. But we’ll see how it goes. See here.

And of course, yes, there is Reid Hoffman, the founder of Linkedin, “one of the tech bosses most fiercely opposed to Donald Trump and Elon Musk“. See here or there or again là.

PS2: April 15, 2025. On the day Harvard University rejects Donald Trump’s requests, I just read a few marvelous pages from the Magic Mountain by Thomas Mann. Here they are:

There came a day when Herr Settembrini directly confronted his pupil, and so betrayed his own pedagogic uneasiness. “But in God’s name, my good engineer, he is just a stupid old man. What do you see in him? Can he do anything for you? It is beyond all reason. It would be clear enough — though not necessarily praiseworthy—if you were simply taking him into the bargain, if in seeking out his company you were seeking out that of his current sweetheart. But it is impossible not to notice that you pay almost more attention to him than to her. I implore you, help me understand this.”

Hans Castorp laughed. “By all means,” he said. “Agreed! The fact is, as we know—permit me to say—fine!” And he tried to ape Peeperkorn’s cultured gestures as well. “Yes, yes,” he said, and laughed again. “You find that stupid, Herr Settembrini, and certainly it is vague, which in your eyes is worse than stupid. Ah, stupidity. There are so many different kinds of stupidity, and cleverness is one of the worst. Hello! Why, I think I’ve just coined a phrase, a bon mot. How do you like it?”

“Very much. I cannot wait for your first collection of aphorisms. Perhaps there is still time, however, to ask you to take into account certain observations we have occasionally made concerning the misanthropic nature of paradoxes.”

“It shall be done, Herr Settembrini. Absolutely—shall be done. No, in this bon mot of mine, you do not see me in hot pursuit of paradoxes. I was merely trying to point out the great difficulty one has in defining ‘stupidity’ and ‘cleverness.’ It is so hard to keep them separate, they are so intertwined. I know very well how you hate any sort of mystical guazzabuglio and are a man who believes in values and judgments—value judgments—and I quite agree with you. But the issue of ‘stupidity’ and ‘cleverness’ is at times a complete mystery, and it must be permissible to concern oneself with mysteries, always presuming it is an honest attempt to get to the bottom of them, if possible. Let me ask you this question: Can you deny that he has us all in his pocket? I’m putting it crudely, and yet, as nearly as I can tell, you cannot deny it. He puts us in his pocket, and somehow or other he has the right to make fun of us all. But why? And how? And where does it come from? It is certainly not a matter of his cleverness. One can hardly speak of cleverness in this case, I admit. He is much more a man of fuzziness and feelings, feelings are his cup of tea, so to speak—if you’ll forgive me the colloquial phrase. What I am saying is this: it is not by way of cleverness that he puts us in his pocket, not through intellectual prowess. You wouldn’t stand for that. And it really is out of the question. But surely it is not physical prowess, either! It cannot be because of his broad captain’s shoulders, or any raw brute force, or because he could lay any one of us flat with his fist—it would never occur to him that he could, and if it did, why, a few civilized words would calm him down. And so it’s not physical, either. And yet the physical dimension does play a role, without a doubt—not in the sense of brute strength, but in another, more mystical sense—the moment anything physical plays a role, things always get mystical. And the physical merges into the intellectual, and vice versa, and cannot be differentiated, and stupidity and cleverness cannot be differentiated. But the effect is there, the dynamic effect, and we find ourselves stuck in his pocket. And for that we have only one word at hand, and that word is ‘personality.’ We use the word in another, perfectly reasonable sense, too: we are all personalities—moral and legal and all those other sorts of personalities. But that is not what I mean. I’m talking about a mystery that extends beyond stupidity and cleverness, and that is what we need to concern ourselves with—partly to get to the bottom of it, if possible, and partly, to the extent that it is not possible, to edify ourselves. And if you are for values, then, in the end, personality is a positive value, too, I should think—a more positive value than stupidity or cleverness, positive in the highest degree, absolutely positive, like life itself—in short, a value for life and in that sense suitable for our earnest consideration. And that’s how I thought I should respond to what you said about stupidity.”

Herr Settembrini let silence reign. Then he said, “You deny that you are in hot pursuit of paradoxes. By now you should know that I have an equal dislike of seeing you in hot pursuit of mysteries. By turning personality into an enigma, you run the danger of idol-worship. You are venerating a mask. You see something mystical where there is only mystification, one of those hollow counterfeits with which the demon of corporeal physiognomy enjoys taunting us on occasion. You have never spent any time in theatrical circles, have you? So you do not know those thespian faces that can embody the features of a Julius Caesar, a Goethe, and a Beethoven all in one, but whose owners, the moment they open their mouths, prove to be the most miserable ninnies under the sun.”

“Fine, a freak of nature,” Hans Castorp said. “And yet not just a freak, not just something to taunt us. For people to be actors, they must have talent, and talent is something that goes beyond stupidity and cleverness, it is itself a value for life. Mynheer Peeperkorn has talent, too, no matter what you may say, and he uses it to put us in his pocket. Set Herr Naphta in the corner of a room and have him deliver a lecture on Gregory the Great and the City of God, something well worth listening to — and in the other corner have Peeperkorn stand there with his strange mouth and a brow raised in great creases and say nothing except, ‘By all means! Permit me to say—settled!’ And you will see people gather around Peeperkorn, down to the last man, and Naphta will be left sitting there alone with his cleverness and his City of God, although he can express himself so clearly that it makes your blood and spit run cold, to use one of Behrens’s phrases.”

“You should be ashamed of yourself, worshiping success like that,” Herr Settembrini chided him. “Mundus vult decipi. I do not demand that people flock around Herr Naphta. He is a dreadful obstructionist. But I would be inclined to stand at his side in the imaginary scene you have just painted with such reprehensible relish. Go ahead and despise distinctions, precision, logic, the coherence of the human word. Go ahead and despise it in favor of some sort of hocus-pocus of insinuation and emotional charlatanry—and the Devil will definitely have you in his—”

Reading a few articles about Deepmind (part 1 of this post) and the founders of Adallom and wiz.io, I remembered other stories of European startups or those founded by Europeans. I’m thinking of Spotify (see my posts in 2022 and 2018) or VMWare (see an older post from 2010). We see that more or less curbed ambition has led to different results. Wiz or Spotify have valuations in the tens of billions, Deepmind, Adallom and VMWare (first acquisition) in the hundreds of millions, while the second acquisition of VMWare was also in the tens of billions. I don’t know if there’s a pattern or if I’m creating it artificially, but it’s a bit as if an acquisition in the hundreds of millions was a semi-failure linked to the fear of too much competition or the impossibility of pursuing an independent adventure.

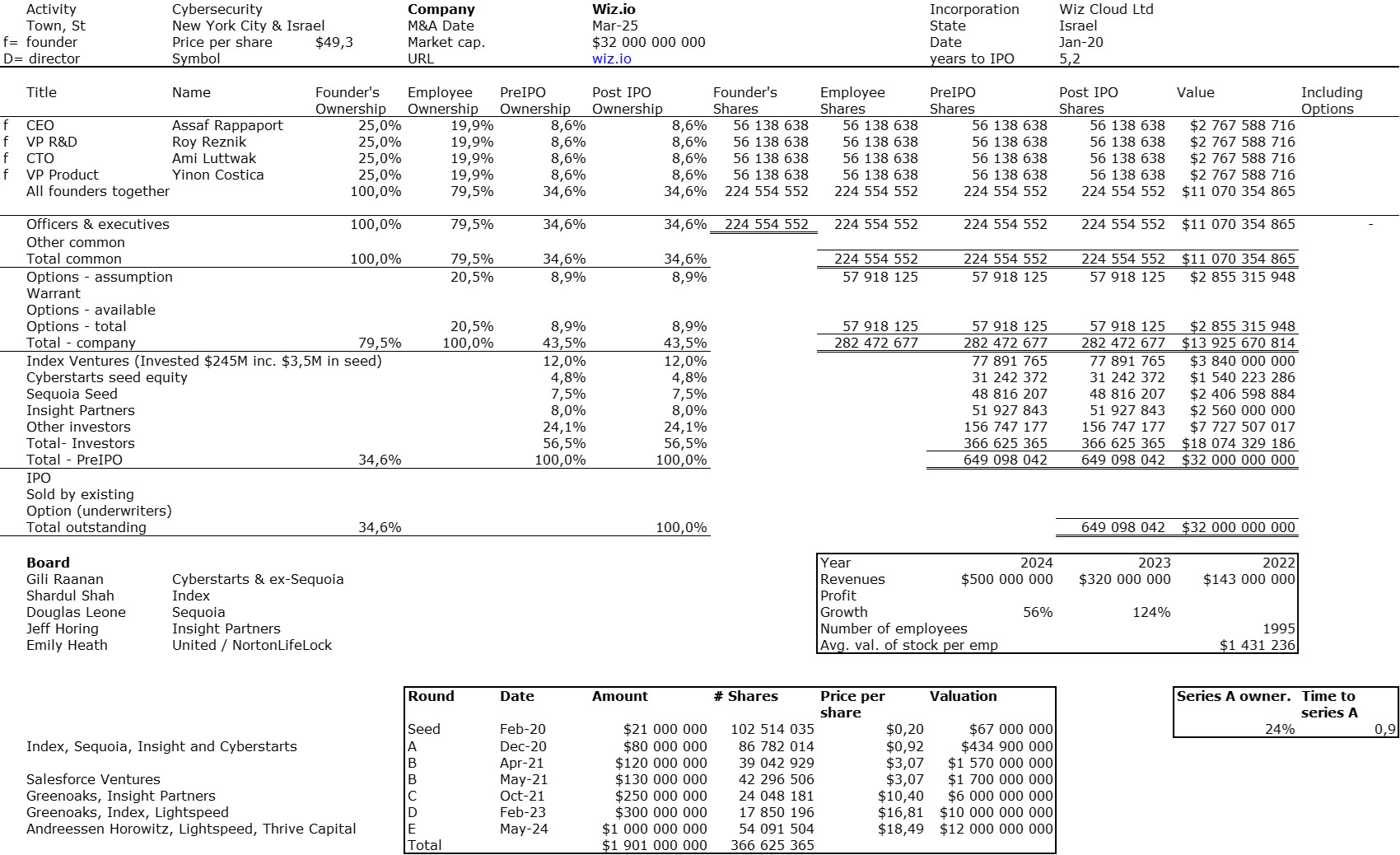

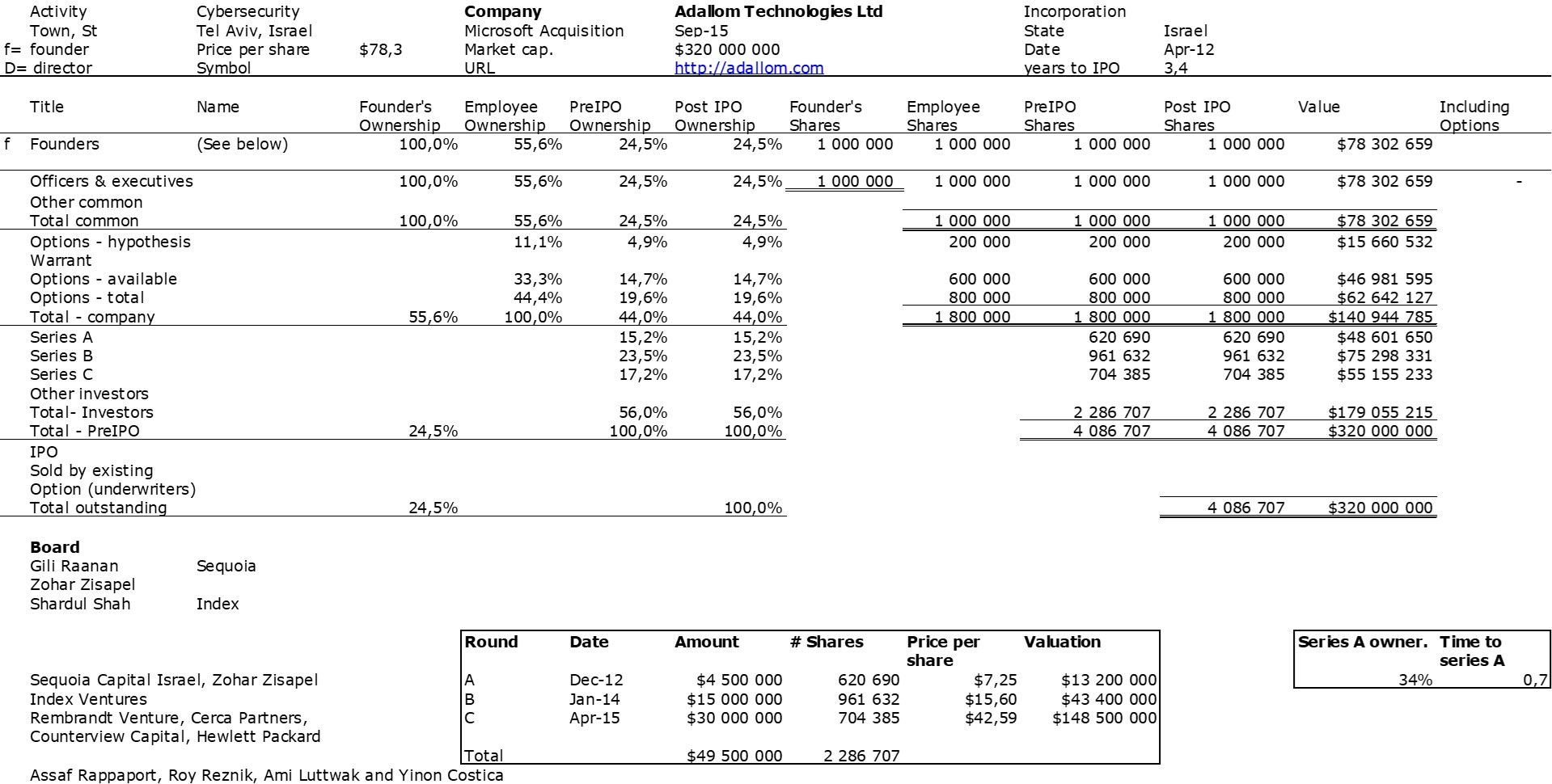

The double adventure of the founders of Adallom and Wiz.io goes a little in that direction. I read a few articles which reference you will find at the end of the article. And I will give the lessons learned by Assaf Rappaport from these two stories. A first success, Adallom bought in 2014 by Microsoft for $320M then a second, wiz.com which Google offered to buy a few days ago for $32B (i.e. 100 times more…) Unlike Deepmind, I did not have access to specific documents, so I had to make some assumptions like some others (see [2]) and cross-check the information available online. Here are the two capitalization tables. But here too, the advice given (which I repeat below) is just as important as this data.

First of all, what I take from the tables:

– Four founders whose story is a classic in Israel (see [1]) created Adallom and then wiz.io. In reality, I am not a big fan of the concept of serial entrepreneurs, but wonder if wiz.io is not rather the scaling up of Adallom like VMWare (2nd period) was for VMware (1st period) or by pushing very hard the Nobel Prize of Demis Hassabis the scaling up of Deepmind! We read in the press that the founders had earned around $25M with Adallom according to some sources and $3B with wiz.io, also a factor of about 100x.

– The same venture capital funds and partners are the investors – Gili Raanan for Sequoia then Cyberstarts and Shardul Shah for Index. These are rare enough to be mentioned especially since these funds intervened at the seed stage.

– For Adallom, multiples of 24x for Series A, 7x for Series B, and approximately 2x for Series C.

– For wiz.io, multiples of 475x for Seed, 73x for Series A, 20x for Series B, 5x, 3x, and 2.7x for Series C, D, and E.

All of this is arguable, but not uninteresting, and there’s a bit of a lottery aspect to it. Don’t get me wrong. Success is rare, never guaranteed. I remember a startup that was offered a $300 million acquisition. The founders and/or investors declined, thinking they were worth more. In the end, the acquisition price was $10 million.

About the ambition and uncertainty, it is also worth reading Shardul Shah (Index) on LinkedIn (Index Ventures just cemented its place as one of the all-time VC greats). Here are some quotes : “I don’t know why we’re talking about averages — none of us are in the business of mean reversion.” […] “I’m not seeking average returns. I’m not seeking good deals—I’m looking for outliers.” […] “I don’t seek comfort. You have to be comfortable with being uncomfortable. We’re in the business of taking risk. I’m not a value investor, right? I believe in the power law.” […] “The hardest thing is identifying if you’re delusional or if you have conviction. Sometimes it can feel like a thin line.”

Finally I extract the lessons from Assaf Rappaport:

1. The team is more important than the idea. A startup is built not around an idea, which is going to change anyway, but around a team. The really good VC funds invest in talent, and not in products, ideas or business plans. And also: Don’t drag your feet when it comes to meeting with the best funds. Don’t leave them till the end.

2. One who listens to problems will find ideas. When you meet with customers, you’re not coming to convince them; rather, you’re there to learn from them. If you’re the one who spoke for more than a quarter of the meeting, it wasn’t a good conversation. Customers have problems that you didn’t even know existed, and the way to discover them is with question marks, not exclamation marks.

And also: You need some luck.

3. ‘No’ is the correct answer to determine whether the investor is serious. No matter what kind of offer you get – investment or acquisition – there’s only one response: ‘I really appreciate your offer, but no thanks.’ This kind of answer never deterred a determined investor or company – and if they’re not determined, they won’t invest in any case. And also: You need to prepare a media plan, both internal and external; when things leak, you’ll have only enough time to hit the Send button.

4. The exit is just the beginning of the hard work. On the day after being merged into a giant corporation, don’t sit back and wait until the options mature. Instead, adopt the commando approach: We’re part of a big army, but we belong to an elite unit.

5. Don’t be afraid of activism. In every company, a moment comes when you have to give the conservative corporate people a kick, and then go ahead and act. To be the best workplace and to recruit the best workers, you need to be brave and take a stand, engaging in social activism that gives rise to tremendous team spirit.

6. Take a deep breath and don’t exhale too soon. You shouldn’t be blinded by big money, instead, use it to quickly acquire paying customers, turn down acquisition offers of hundreds of millions of dollars, and grow the company rapidly so it will become a unicorn.

7. Today, it’s possible to overtake everyone with a computer and Zoom

I probably have to admit a bias in favor of startups led by tech founders. It is what I have been advocating for decades now. So when I read about stories going that way, I am more than happy. Recently I was mentioned by friends a documentary movie entitled The Thinking Game.

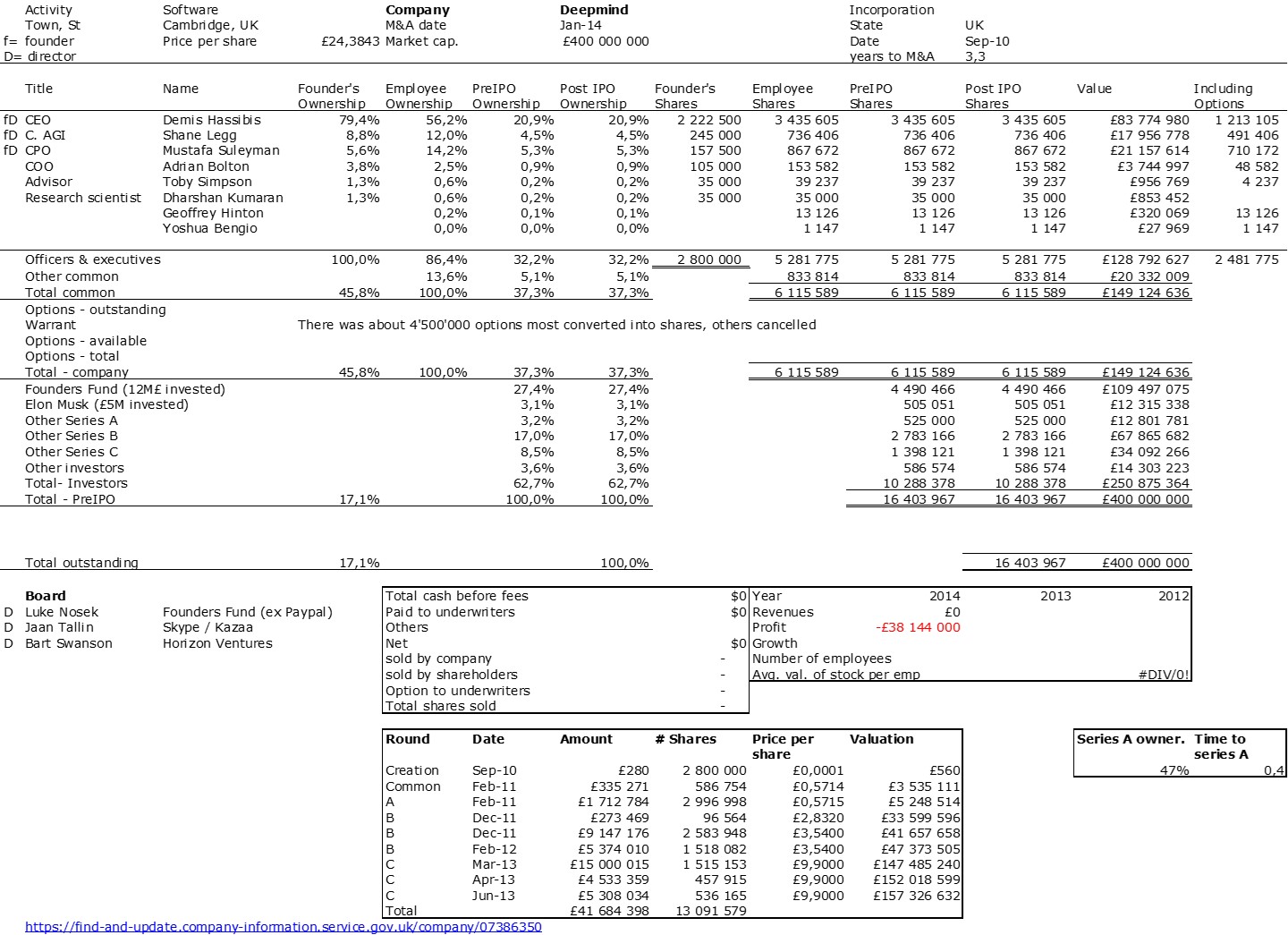

I do not know why I had not looked at DeepMind before all the more it is pretty easy to get information about British companies and this is a British startup. So you read me, I built its cap. table when it was acquired by Google in 2014 for about

What I read in the table:

– 3 or 4 main cofounders, but Demis Hassibis had the biigest initial stake (80%),

– investors took high risk as the company did not have that much but talent initially, (and no revenue until acquisition ?)

– the main or at least most famous investors were Peter Thiel and Elon Musk,

– the company did not raise that much money : 2M£ in Feb. 2011, £15M in Dec. 2011 / Feb. 2012, finally £25M in 2013 before the £400M acquisition by Google in Jan. 2014.

That’s it for the basic facts. More importantly, the lessons in the article my friends sent to me are: – First, DeepMind combines crystal-clear strategic clarity with never-ending tactical flexibility. What comes across in the film is the company’s extraordinary willingness to experiment wildly and fail persistently.

– Second, DeepMind’s mission has helped it recruit some remarkable scientific talent, critical to its success. In a discussion after the movie, Hassabis explained that he had always resisted investor pressure to move to Silicon Valley and had been determined to remain in London. “The UK has always been very strong in science and innovation and has a rich history in computing,” he said. “We are trying to carry on in that tradition.” Hassabis reckoned that there was a lot of under-utilised academic talent in Europe, and elsewhere, that could be attracted to London. So it has proved.

– Third, what was essential for DeepMind’s success was its ability to scale rapidly. Back in 2010, few VCs were prepared to go anywhere near a startup with such extravagant ambitions and no business plan. Much of its initial capital came from US investors, including Peter Thiel and Elon Musk. The company also felt compelled to sell out to Google in 2014 to give it the capital, data and computing firepower necessary to stay at the leading-edge of AI. (The extra resources were essential for recruiting and retaining top talent, too).

Often not to say always the same lessons about risk taking and ambition…

PS: I have not watched the movie yet, so I may amend this post in the near future.

Back to my favorite topic, that is Silicon Valley, after a few digressions. I just rediscovered a 2022 paper entitled Systematic analysis of 50 years of Stanford University technology transfer and commercialization. The full paper is available here. As a side comment, this has been motivated by recent articles about Technology Transfer in France and more specifically the study entitled “Étude sur la performance des SATT vis-à-vis d’une sélection d’OTT” (Study on the performance of SATTs vs. a selection of TTOs). Unfortunately, the study does not seem to be public and I could only read comments about it.

I have published a lot about Stanford University. The search engine gives the following here. So I will not go into much detail but just extract what I found interesting not to say surprising. Here it is:

– this is about money, but not only about money.

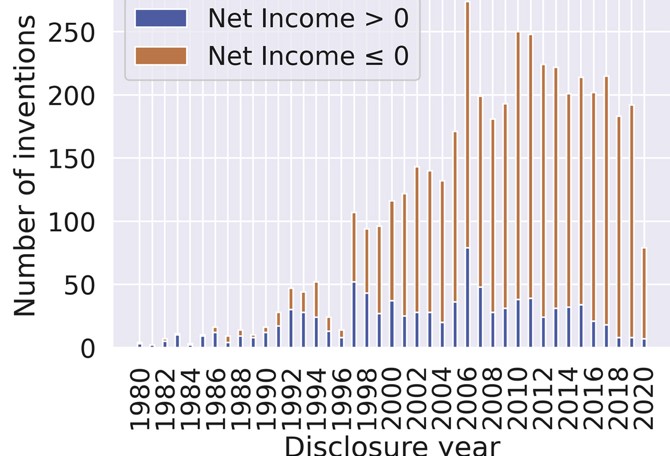

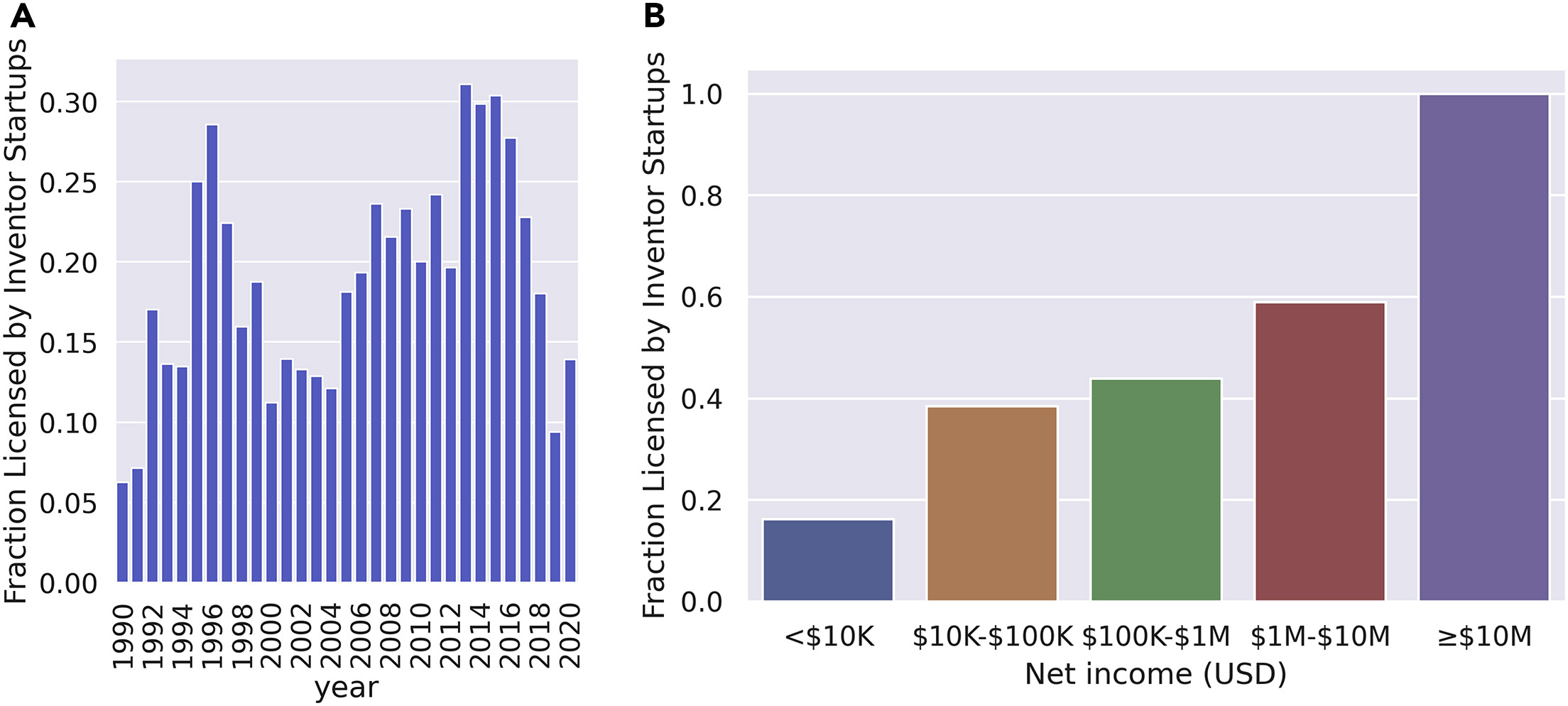

“The total net income of the inventions for all years considered is $581M, and the average net income is $0.13 M. Overall, most inventions have a negative net income, and only 20% of inventions in this dataset have produced positive net income.” Further in the paper “The invention licensing via OTLs represents only one facet of the transfer of technology from university to industry, though it is an important facet. [And] we primarily focus on net income as the outcome metric because it is straightforward to quantify and is a key metric of OTL’s own assessment. However, it is important to note that licensing income does not completely capture impact, and pursuing licensing income is not the ultimate goal of the Stanford OTL.”

Overview of the Stanford inventions data : Number of inventions by year that Stanford’s Office of Technology Licensing marketed. The color of the stacked bar chart indicates whether the cumulative net income (until June 31, 2021) is positive.

– the most profitable inventions are predominantly licensed by inventors’ own startups.

“Around 20% of the inventions were licensed by the inventor’s own startups, which we refer to as “self-licensing.” Overall, the self-licensing rate increases over time. The interesting peak of the self-licensing rate in 1995–1999 might be related to the dot-com bubble. We also found that inventions with high net income are predominantly self-licensing inventions. For example, all inventions that have generated more than $10 M net income are self-licensed, and the self-licensing rate for the inventions with $1–$10 M net income is 59%. In contrast, the self-licensing rate for inventions with less than $10 K net income is 16%. This finding is consistent with previous research showing that startups with direct connections to the university tend to be more successful than otherwise similar startups.” There is a more general side comment here : “Shane et al. found that new ventures with founders having direct and indirect relationships with venture investors are most likely to receive venture funding.”

Self-licensing (inventions licensed by the inventor’s own startups)

(A) The fraction of inventions licensed by inventor startups over time.

(B) The fraction of inventions in each net income group that the inventors license. The sample sizes for each net income category are: <$10 K: 3,776 inventions; $10–$100 K: 465 inventions; $100 K–$1 M: 212 inventions; $1–$10 M: 56 inventions; ≥$10 M: 5 inventions.

– inventions have involved larger teams over time. There is also an interesting side comment : “Smaller teams have tended to disrupt science and technology with new ideas and opportunities, whereas larger teams have tended to develop existing ones.”

“In addition, we found that the inventions from teams of only first-time inventors have a higher net income than other inventions. This highlights the importance of being open to first-time inventors.” This is correlated with my analysis of serial entrepreneurs, I had found they have a tendency to do worse over time.. See Serial entrepreneurs: are they better?

I will briefly conclude that this is a very interesting new study of Stanford’s contribution to innovation, which confirms well-known things and adds much less known ones. A must-read for experts and “food for thought” for the others!

I listened to Xavier Niel on France Culture on December 6th and I had the confirmation of a relatively atypical character. Asked in particular about Elon Musk, here is his answer: Xavier Niel distinguishes between the entrepreneur, “probably the best in the world”, and the character, “completely crazy and potentially dangerous”. He praises his willingness to consider savings for the American state: “if he applies these savings in a reasoned way, to reduce the operating costs of the American state, I am sure that it will go very well. If, after that, we start to overflow, that’s nonsense!”, he qualifies. According to Xavier Niel, it is not so much the fact of paying fot Twitter 45 billion to own the social network that poses a problem, but rather the fact that the product takes on the image of its owner, “which is less exciting”, considers the boss of Free. The price doesn’t shock me if he sets up a plan that will make this company generate money. The purpose of a company is to bring together three parties: employees, customers and shareholders. Consequently, these three parties must be happy. However, the customers are not happy in his case.” In the dialogue he establishes with Jean-Louis Missika, we find a rather fascinating character who uses “ouais” (yeah) and “nan” (nope) as if he were still the kid from Crétail where he grew up. The character is a billionaire but his career has not prevented him from (or perhaps helped him to) staying down to earth unlike some of his counterparts in Silicon Valley.

I liked this book which doesn’t give advice but allows you to understand certain things about his character and his vision of entrepreneurship. A first example: I believe that youthfulness as a state of mind is essential. It is found more often in young people, because when we get older, we become richer, we harden. Youthfulness allows you to create incredible things. You don’t yet have the constraints that are imposed on you when you get older. With age, society imposes limits on you, you no longer have the optimism or the attitude towards risk that you had in youth. Whereas when you are 20 years old, when you leave school, you want to eat the world; you want to do crazy things. [Page 35]

Beyond the usual explanations about this world, Niel expresses unfailing optimism. When I started investing in startups, I was convinced that all entrepreneurs were going to be successful, that they were all going to create huge companies. Well, there were a few disappointments, but you get the idea. In another genre, I thought that Putin was threatening to invade Ukraine but would never act. Just like I thought that Covid would be over in 3 days, and that Brexit would never happen. I am a walking disaster when it comes to forecasts, because I am too optimistic. There are people who use the word “genius” to talk about me; it’s ridiculous, I am absolutely not a genius. I have two strengths, which are based precisely on my lack of intelligence: the simplification of problems, and naivety. […]

JLM: And when it fails?

XN: And when it fails, I forget and move on. Because if you let yourself get discouraged by your failures, or if you listen to everyone who tells you “it’s impossible”, you do nothing. […] When I created Station F, I hoped to welcome 1000 start-ups. And François Hollande, to whom I presented the project, said to me: “But are you sure there are 1000 start-ups in France?” Well, you know what, at the time, I had never asked myself the question! Yet it’s a logical question, I should have thought about it, done a market study, that kind of thing. [Page 39]

The important thing is not the project, it’s the founder. [Page 133]

With Kima, yeah, we have a method. We spread the risks. We invest small amounts – around 150,000 euros – in a hundred start-ups each year. Between failures and trade sales, we must have 1,500 participations.

JLM: Less than fifty that work out of 1,500, that’s not a lot…

XN: It’s part of the game. Yes, you’re wrong, and you’re wrong often. […] We don’t finance success, we finance progress. […] Of all my investments, [Square] is the most spectacular performance. I think we did x1,000. […]

The Americans I know who had success with their start-ups were all developers. [Page 139]

Not only did they have the idea for their product, but they also developed their own software, website or app. Google, Facebook, Snapchat, they were all created like that: by people who coded their own products. Hence this idea that a start-up has a better chance of succeeding when there is a coder among its founders. That’s why I created 42.

[whereas] unicorn founders, I love them, but they always have the same faces: three white guys who went to business school [page 145]

Being an entrepreneur is [page 146]

choosing what you do during the day. If you don’t want to make something, you don’t do it. You create your own job. There’s no greater freedom. Is that okay, is that convincing enough?

JLM: Rather. But you’re forgetting the pressure…

XN: That’s not what’s important. What’s important is what you’re capable of creating. […] For me, this desire to create something from an idea, to bring together different people to bring something to society, create value, invent a different product, help the most disadvantaged. Entrepreneurship is an attitude, a state of mind. You don’t need to start a company to be an entrepreneur. Are you launching an association, a project, a social media account with a real editorial line? For me, you’re an entrepreneur. Entrepreneurship isn’t just about business. You can be an entrepreneur in humanitarian, social, educational, environmental, and so on.

A desire for revenge? [Page 204]

The taste for the game is enough in itself. No need for psychology. Everyone likes to play; it’s the playing fields that differ. Mine was the telecom market. Everything is a fucking game. An eternal game, that people have been playing since the beginning of the world. So I play, and whatever the game, I want to win. I want to be first. It’s more or less long, sometimes you get overtaken. And then you catch up. That’s what gives life spice.

[…] When I try to understand why I failed, it’s not because I regret having lost money. It’s because I want to be number one. […] Nope, I just like winning. Money is just a signal that you have won a game, because you are playing with money. [page 205]

Niel is not naive. He is even a fighter. When he returned to Créteil to talk to the “kids” It is not easy to catch their attention. We are mostly white, old, even old fools. So I have a trick to wake them up. I tell them: “I also went to school here in Créteil, and then I went to jail.” And then all of a sudden, the kids wake up. [Page 22] He also admits “Me, since I was little, I wanted to earn money” [page 15] while his first words of the interview are “Frankly, I had the happiest childhood in the world. We were a very close-knit family. I swear, everything was perfect. I was so happy that I thought I was the king of the world, and that my parents hid it from me so that I could have a normal life.”

My closest friends are entrepreneurs, some are Americans, some of whom have created social networks or others are investors. I like entrepreneurs because they are different, because they have a little grain of madness, because I am never bored with them: people see me as a billionaire, but I see myself as an entrepreneur. [Page 222]

How do you explain the excesses of entrepreneurs? [Page 227]

JLM: When Elon Musk challenges Mark Zuckerberg to an MMA fight, everyone laughs but he ridicules the ecosystem. In a less visible way, the positions taken by Peter Thiel or Marc Andreessen are just as sulphurous, and give the impression of a caste that believes itself above ordinary mortals. You know them a little, how do you explain these excesses?

XN: The people you mentioned are very different from each other. There are some who are a little crazy and who believe they have superior intelligence. And there are others who are a little like children in the playground. It’s… special: But that doesn’t prevent them from having their charm and being interesting. […] But they’re not all like that. And besides, they left Silicon Valley. It’s a part of the ecosystem. Very noisy, yes, but only a part of it.

JLM: We don’t hear the others anymore. They’re nowhere to be seen.

XN: That’s not true, they just do something else. And then if you take the current boss of Google, Sundar Pichai, he’s an Indian immigrant who doesn’t consider himself superior to the rest of humanity. I don’t know his political ideas, but I’m sure they’re quite different from Elon Musk’s. […] Elon Musk only represents himself. He’s locked himself into a transgressive extremist persona and I don’t know how he’s going to get out of it, because by talking bullshit, the time comes when you pay for it. The moral is that you can be both a brilliant entrepreneur and a dirty jerk.

You know when you talk to them, you find yourself in an unreal world, where disruptive innovation is always for tomorrow morning. How many times have I heard that nuclear fusion is in a year. Same for carbon capture. That’s what makes entrepreneurs strong: for them, if you don’t try, you have no chance of succeeding: So they try, again and again. That’s why, despite all their questionable attitudes, I love these people so much.

As a conclusion

I have already discussed the excesses of Silicon Valley, for example here. Its excesses sadden me and yet, I have a certain fascination for the achievements of its entrepreneurs. This is probably the same reason why I also enjoyed reading Une sacrée envie de foutre le bordel (A real desire to cause trouble). We may not agree at all with Xavier Niel. We may not agree with everything Xavier Niel says. The book is full of exciting anecdotes and also of questionable points of view, we must simply remember that the man is optimistic and defends freedom almost without limits. His limit is the law, and even that… not at the beginning.

Xavier Niel’s book has a bit of this effect. We often find the child behind the billionaire, his style, his passions. We discover that the entrepreneur is a cataphile. He ventures there about once a month, much more when he was younger…

The last sentence of the book [page 300]: F…!, it’s still indecent, how lucky I was!

PS. For those interested in politics and Silicon Valley, a seminar throughout the first half of 2025 seems to have an enticing program, Digital Capitalism and Ideologies.

It’s a podcast from France Culture that introduced me to Arte’s new series, Silicon Fucking Valley. I’ll take two sentences from it: “Stories that are sometimes well-known but always necessary to recall in order to participate in our digital culture and allow everyone to be able to decode our connected world a little” and “I had a little more trouble with the sometimes frenetic pace of the episodes, which are stuck in 15 short minutes. A voice-over, very present, which accompanies the viewer a little too much, who would sometimes benefit from breathing to find the time to construct their own thoughts. The writing follows the recipes of videos published on social networks whose objective is to capture attention.”

And I want to add, without, I hope, coming across as the grumpy one, that the series is sometimes lazy due to its inaccuracies, even if of little importance:

– why say that the Stanford campus (7km2) is a third of the area of Paris (which is 100km2)?

– why say that the diplomas of this university are awarded on the Quad when they are rather awarded in the stadium where Steve Jobs made his famous speech (1st article of this blog)?

– why say that the tuition fees amount to $80,000 when they are $65,000 already (forgetting to add that at the Master’s level, I think that a majority of students have a scholarship or a sponsor…)?

– why say that the Computer History Museum is in Menlo Park when it is in Mountain View?

If we forget these details and this frantic pace, then, yes, there are some very interesting things. You will discover Luc Julia and Adam Cheyer at the origin of Siri from SRI (check CALO), a startup sold to Apple for “$200M according to the rumor” and which did not leave me with very good memories because EPFL should have gotten a bigger piece of the pie during that sale. Julia is right, it was crap. The F… word is appropriate!

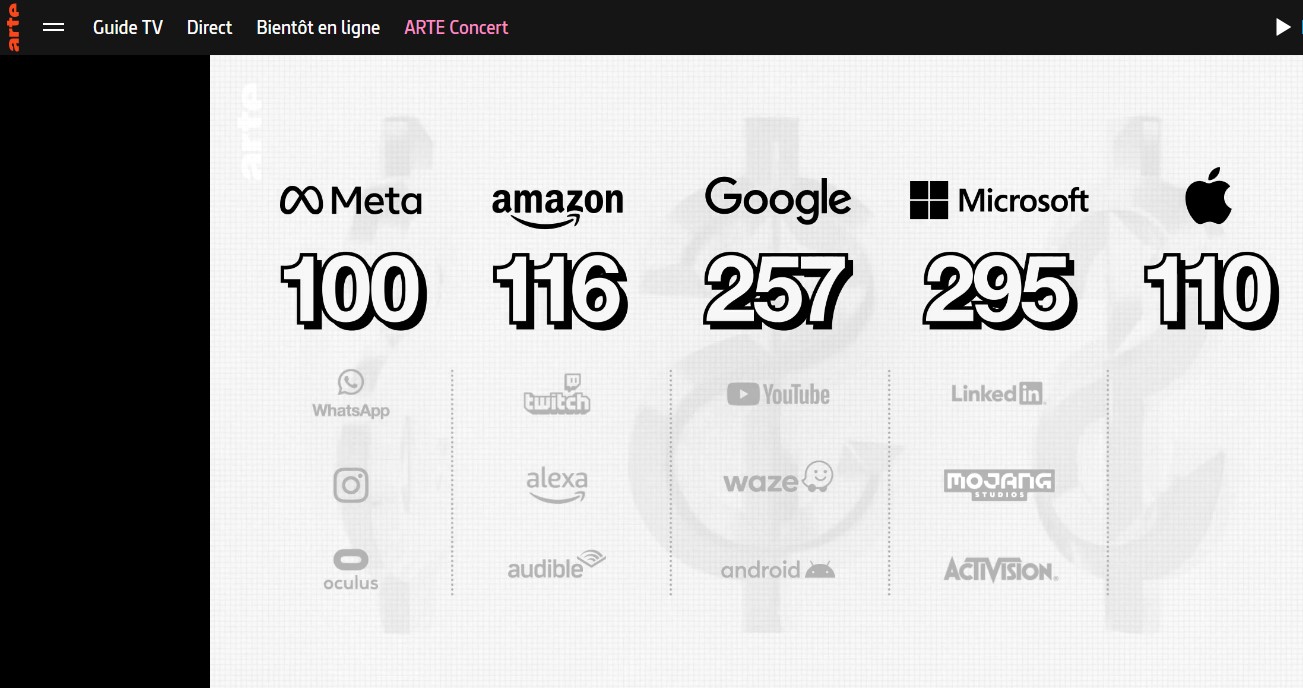

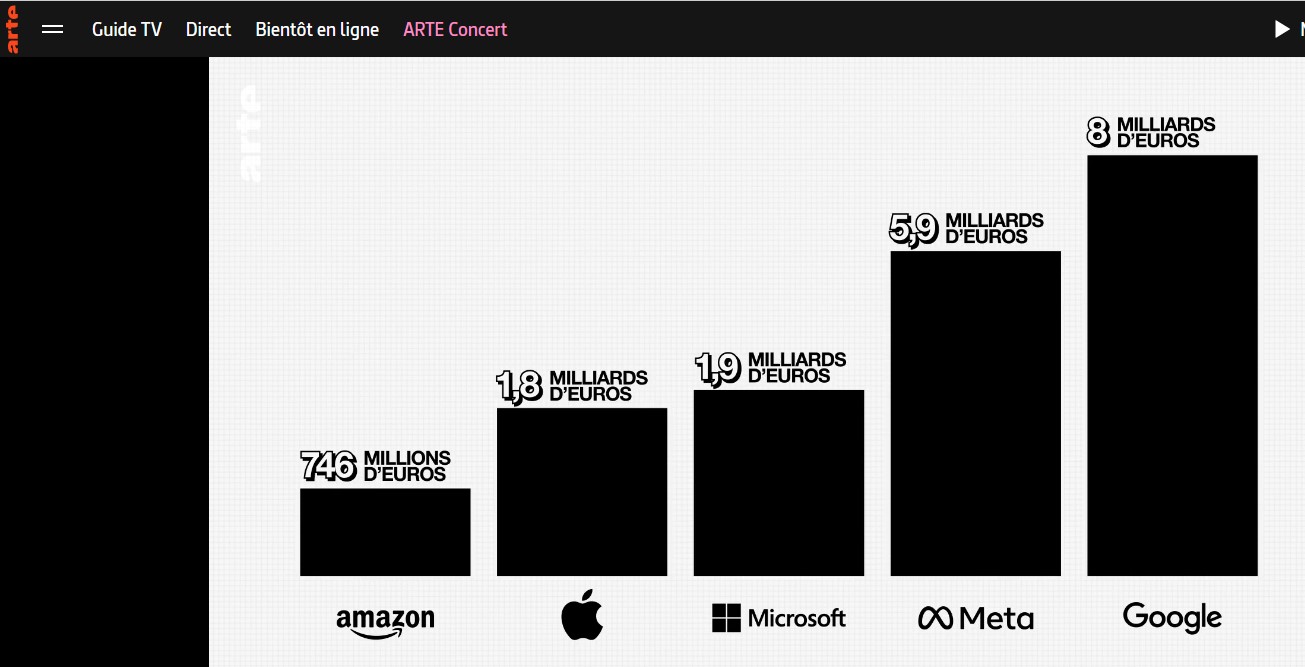

You will also discover Curious Marc. It may also remind you of what the “Mother of All Demos” was (with a strange acronym). And more seriously, the recent evolution with GAFAs. Here are two illustrations: the number of acquisitions of each actor and the amount of fines paid in Europe and the USA.

It’s also about Venture Capital and mythical San Hill Road

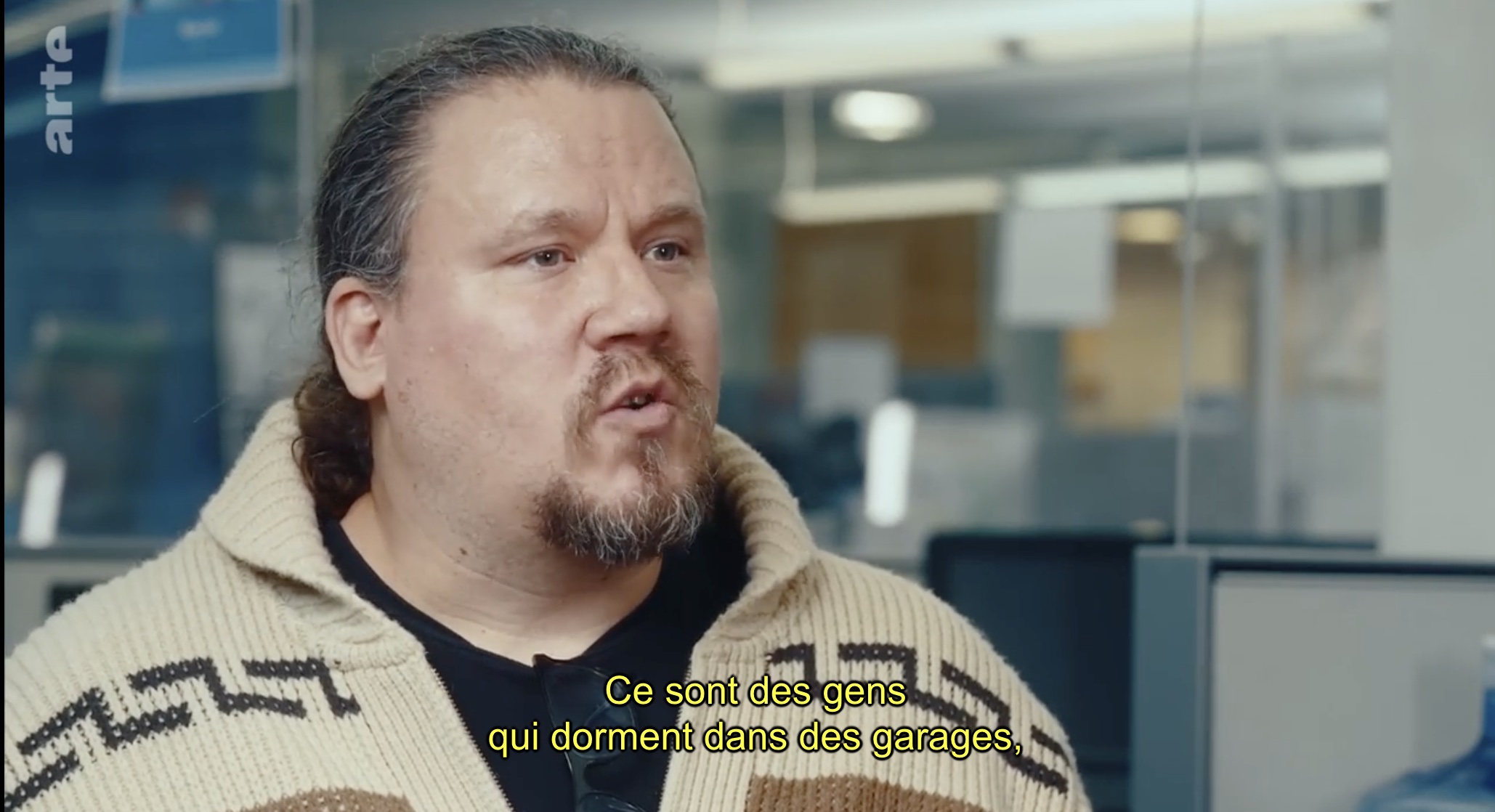

But the most touching episode remains the 6th on the wealth gap, “for one tech developer, there are six poor people who clean, serve in cafeterias, provide security, drive Google buses” and have the choice between driving 6 hours a day or sleeping in a tent or a camper van on the side of the road. The title is then telling, Silicon Fucking Valley.