This recurring question of looking for a cofounder has been bothering me for years. Similarly I do not like the idea of giving titles in the early days of a startup (project) as you may read here : Titles in Start-ups.

My argument is that you don’t look for cofounders. You have them already, you found them by talking about your project to friends or colleagues. It’s a bit like falling in love, you do not look to marry, you meet people. Point.

Of course, this does not help much, because there remains the loneliness of the entrepreneur. But do we get married just to fill the loneliness? As it turned out, thinking about it, I came across an excellent article in which I totally recognized myself: Everything You Need to Know About Startup Founders and Co-Founders.

Here are some key points:

– A founder is a person who comes up with an idea and then transforms it into a business or startup. If a founder sets up a company with other people, they are both a founder and a co-founder.

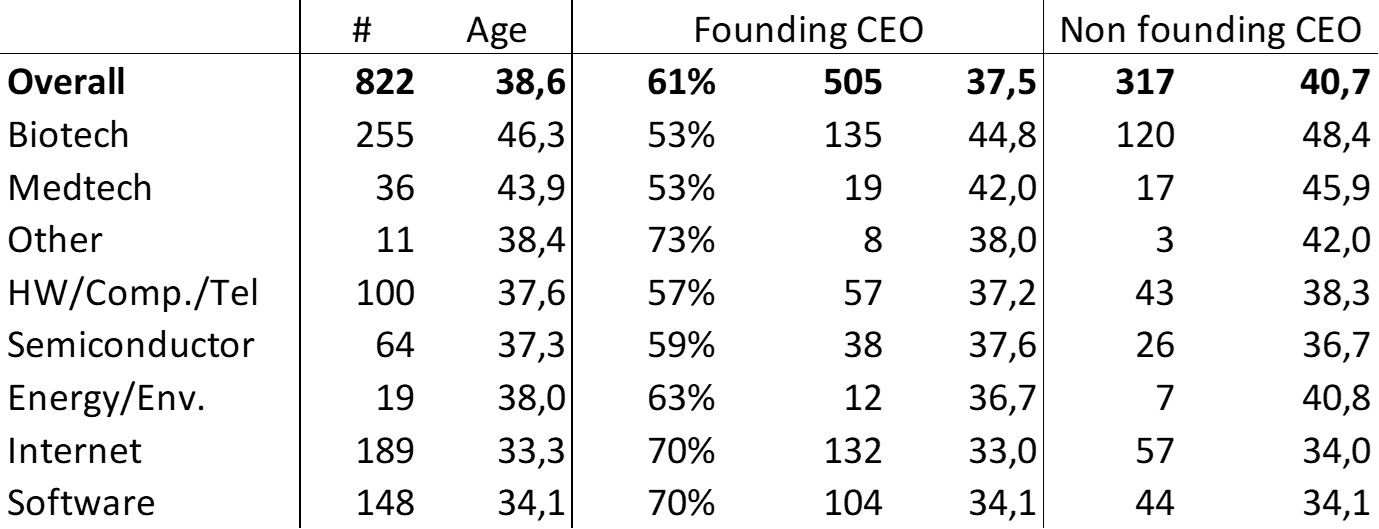

– “Founder” and “CEO” are two […] startup titles that people can carry simultaneously. One is a permanent title, while the other is not. “You will always be a Founder or Co-Founder.” Be sure to be careful however how you dole out the Founder/Co-Founder titles. That should be a lifetime title so be sure it goes to the right people who played a major role in the starting of the company and who will continue to play a role in the years to come.

– A founding member can often feel similar to a founder or co-founder because they come on so early in the process that they’re also putting in crazy hours and maybe even taking a pay cut in order to be a part of something important. But a founding team member is an early employee, not a founder. One important difference? The types of stock the two groups receive. Founder’s equity is different from Employee Stock Grants.

– “I’m totally unconvinced that two people can find a person they haven’t known previously, and become effective co-founder,” […] “I think you’re better off finding the money to hire someone than actually find a co-founder.

– If someone has come along a little later in the game, but still early — as in, pre-first employee — then you treat the same any other co-founder! If you’re choosing to add a “co-founder” after you already have employees, though, things can get a little tricky.

One thing is forgotten in the article, it is the investor (friends & family, BA, VC) or institution entering at the creation and from my point of view they are not founders because they do not (generally) contribute to the business…

Finally, the term founder does not seem to me to have a legal existence. It is only awarded by the group of people who recognize themselves as such. There is, however, an interesting example, namely how one of the founders of Tesla filed a complaint against Elon Musk, in particular because he considered that he was not a founder. The complaint is readable here (see page 28).

If you wish to dig a little more, here are two older posts:

– The Founder’s Dilemmas – The Answer is “It depends!”

– Founder without experience, lonely founder.