The first video, Investing at the Technological Frontier, describing the radical uncertainty of innovation and how it contributes to economic development.

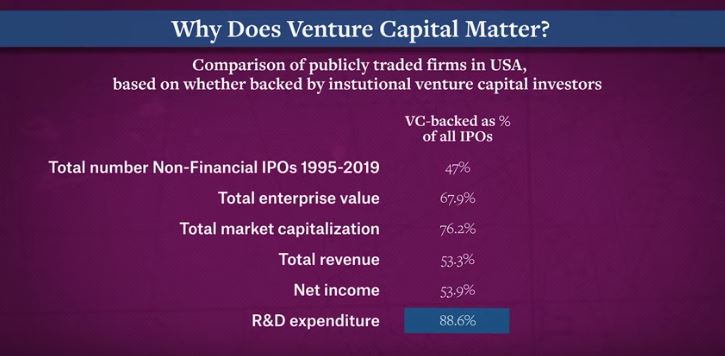

In the second video, What Venture Capitalists Do, he further develops his thoughts that I summarize through a few screenshots below. (They are self explanatory and you should certainly listen to Janeway if you are curious or intrigued).

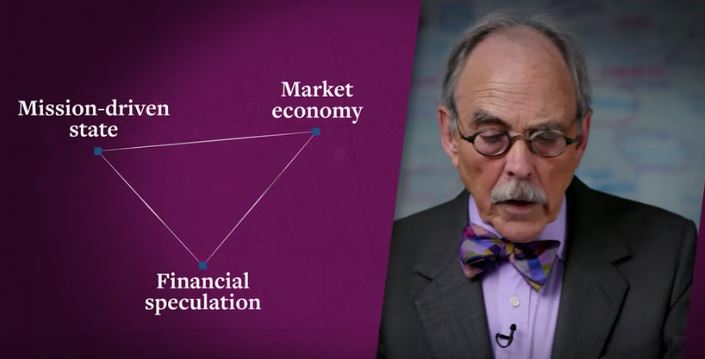

The 4th video, The Failure of Market Failure, opens the debate of state intervention and private speculation. This important topic has been largely debated by Mariana Mazzucato and you will find additional posts under tag #mazzucato.

I must admit I did not know Bill Janeway. I should have, given his long expertise in venture capital. His recent contribution was mentioned by many including Nicolas Colin and on a personal note, friends from IMF. They just mentioned to me 8 videos which seem absolutely brilliant: Venture Capital in the 21st Century.

I just watched the third: Evaluating Venture Capital Performance | #3 | Innovation in the 21st Century. Here are the slides.

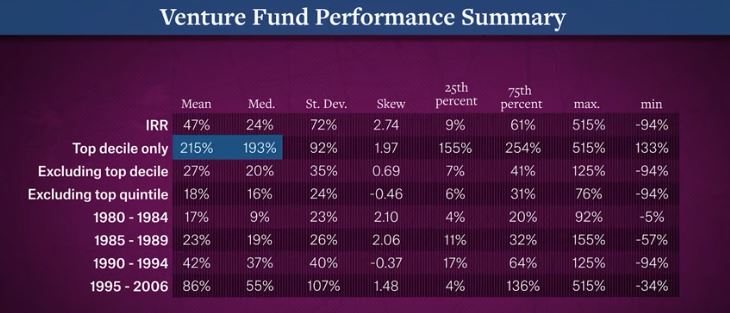

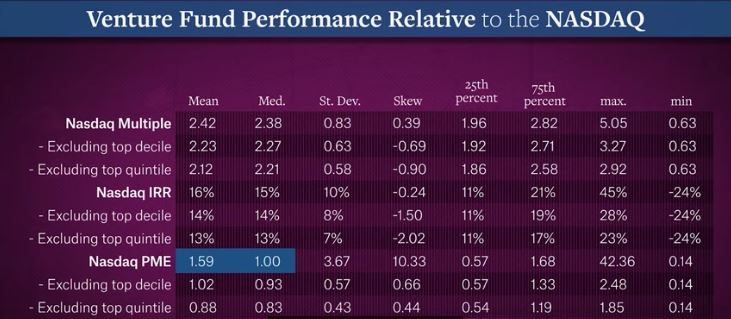

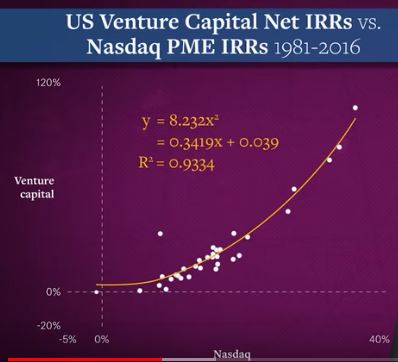

Janeway reviews the performance of Venture Capital firms and recent changes in the venture capital market. He starts by summarizing the stylized facts of venture capital returns (highly skewed, very persistent, and correlated with the stock market). VC capital increased rapidly in the late 1990s, peaking in 2000. VC returns have since settled down, with longer holdings and fewer IPOs. But with the climate of zero real interest rates since 2008, new unconventional investors (private equity, hedge funds, etc.) have waded into venture financing directly, hunting for the high returns of the next big tech giant. A “Unicorn Bubble” has developed as a result, where dubious firms have been financing their growth by selling illiquid securities at inflated prices to deep-pocketed investors with little expertise or control over the entrepreneur. This may have implications on the long-term link between venture financing and technological innovation.

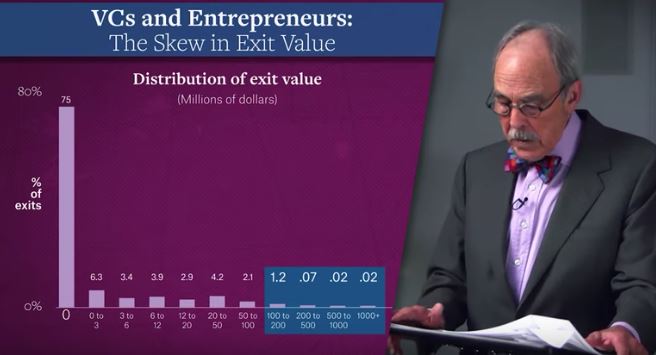

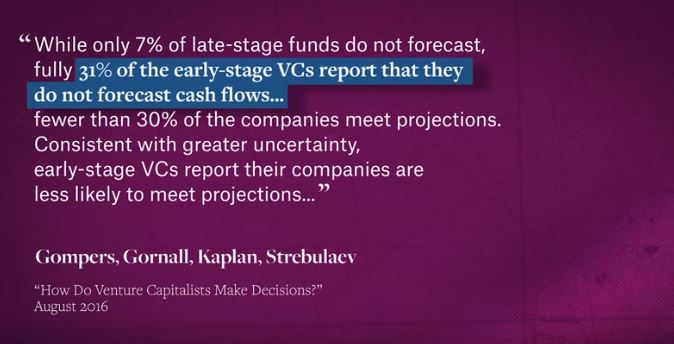

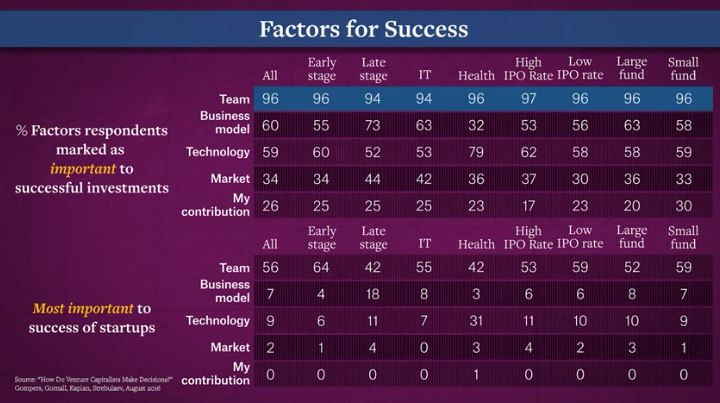

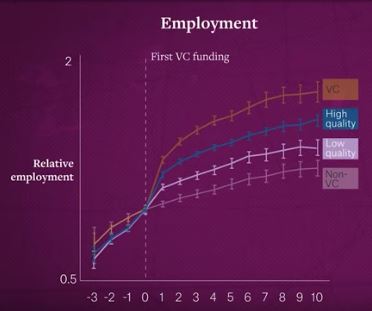

I just copied a few screenshots:

Venture capital is highly skewed and follows a power law, just like startup success models.

Venture capital returns are highly correlated to those of Nasdaq as shown above and below, so… ?

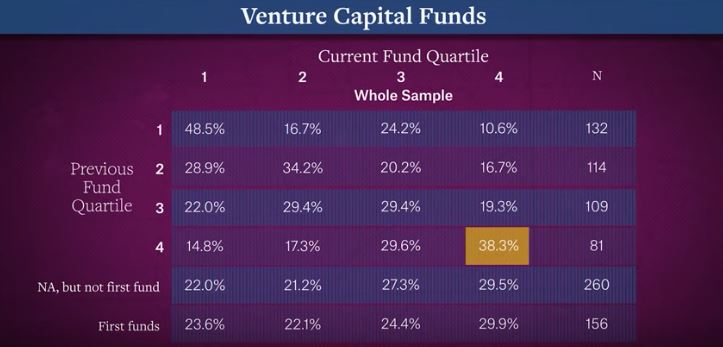

Good VCs are good and bad VCs are bad.

So…

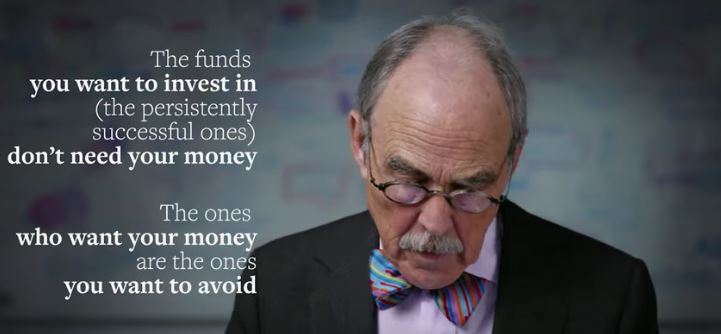

“The message here to limited partners is very clear.

A blind allocation to venture capital, just allocating a fixed proportion to venture capital runs the major risk of what’s known as adverse selection.

The funds you want to invest in, the persistently successful ones, don’t need your money.

The ones who want your money are the ones you want to avoid.”

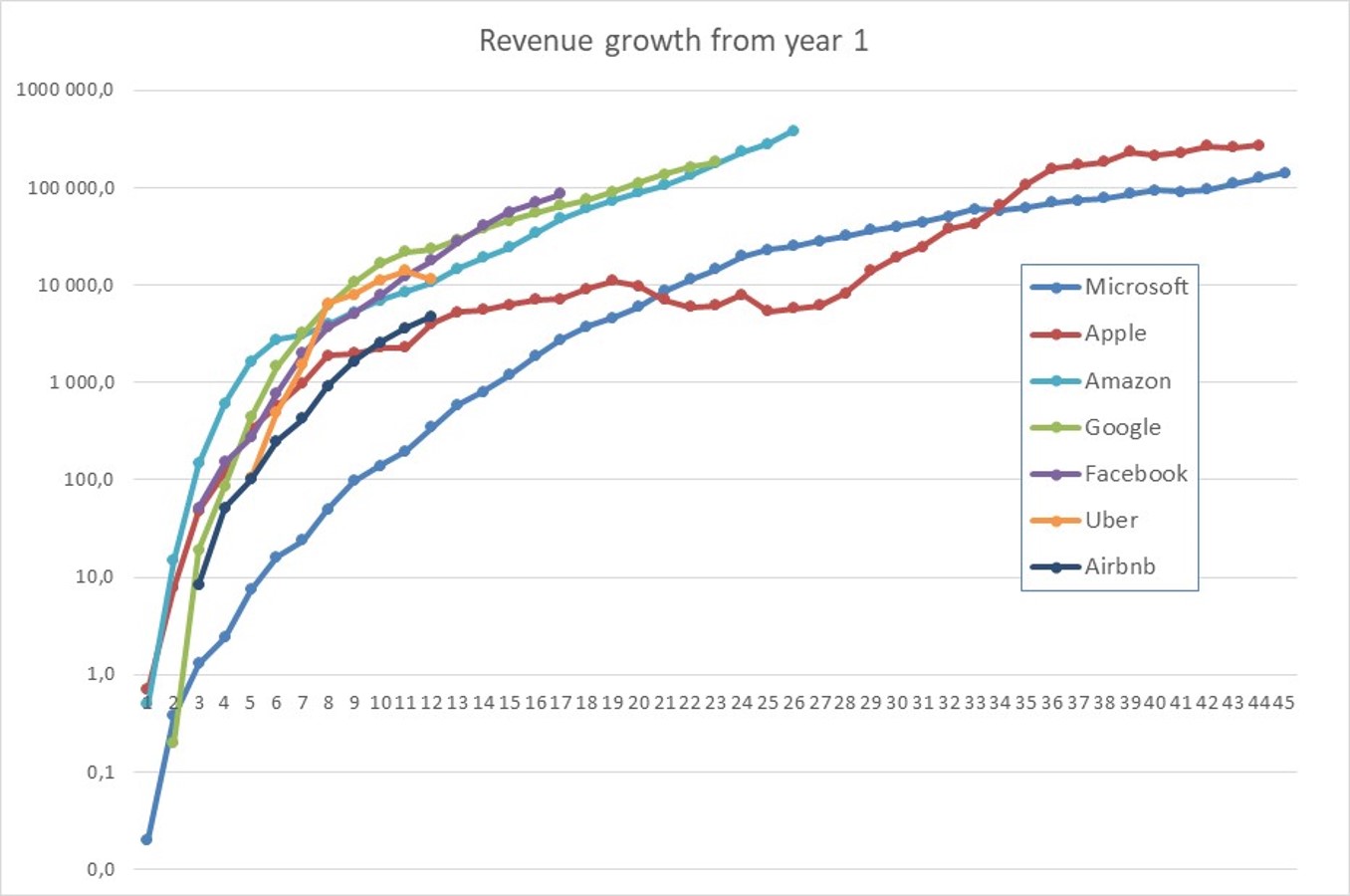

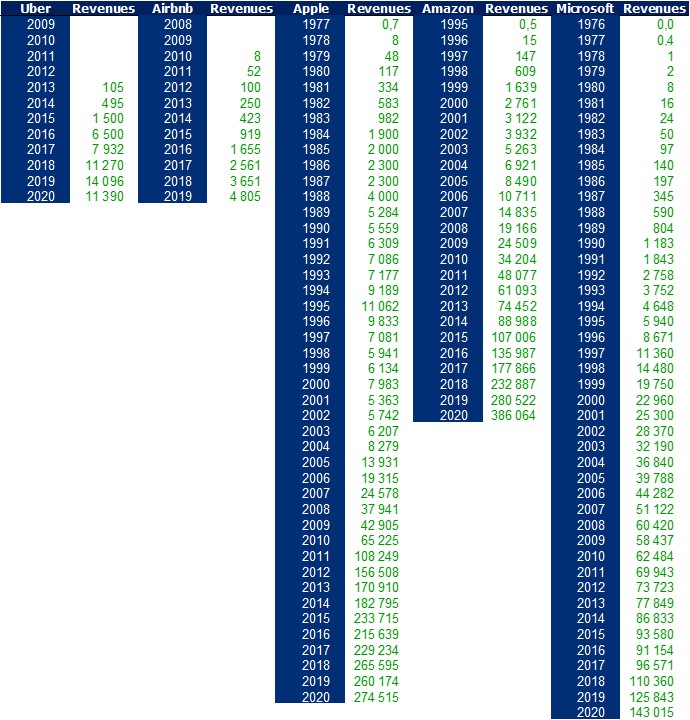

Yesterday I published data in Tesla, Google and Facebook do not suffer from the crisis. and after linking my post to the usual Twitter, LinkedIn and Facebook, one of my readers (thanks Manuel!) told me it would be fun to add Uber as a comparison. I said I would if/when I find the time and then thought why not AirBnB, Apple, Amazon, Microsoft?

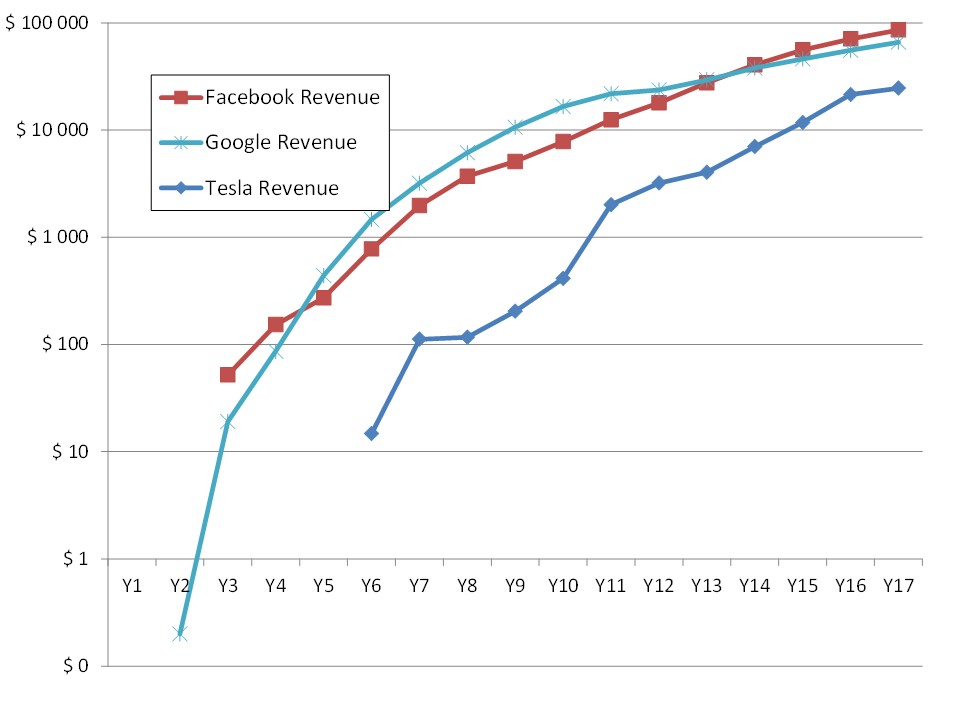

I could only compile data about revenues of these firms and I think it is striking enough:

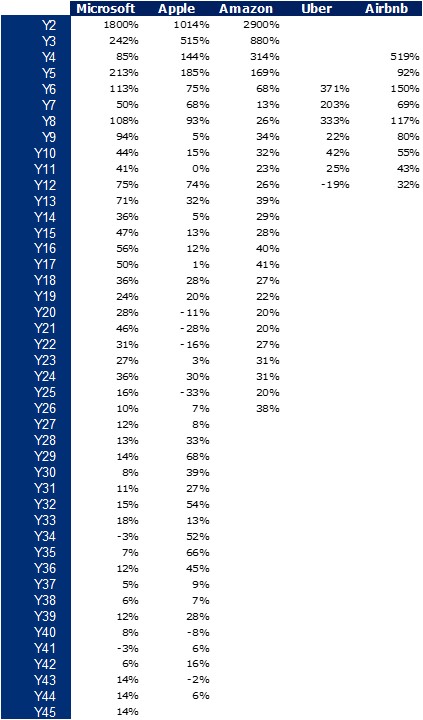

I wrote yerterday the growth rate was above 100% (doubling every year) in the early years declining to around 40% (doubling every other year) then to 15% (doubling evry five-year). Here are the growth rates of these old and new Titans. It begins again with 100+% for all of them. Too early to say about the future of Uber and AirBnB.

The three others of the GAFAM.

– Microsoft even had a 50% growth in its second decade, Amazon was closer to 30% and Apple struggled with 20%.

– In their 4th decade, Microsoft had an average grwoth of 10% and Apple 30%.

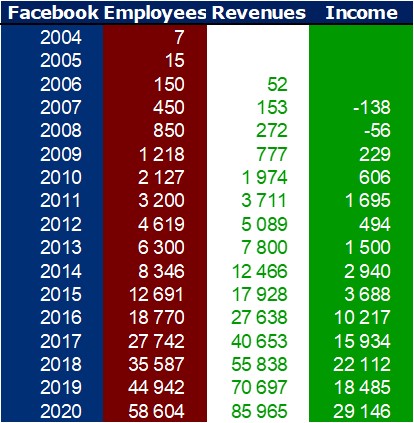

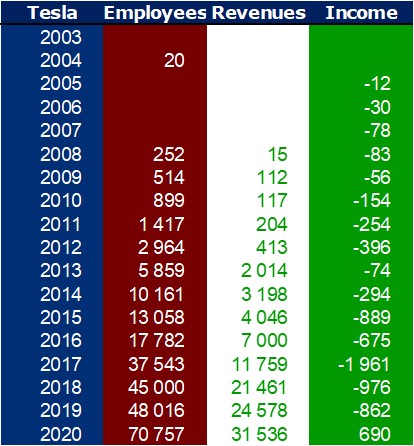

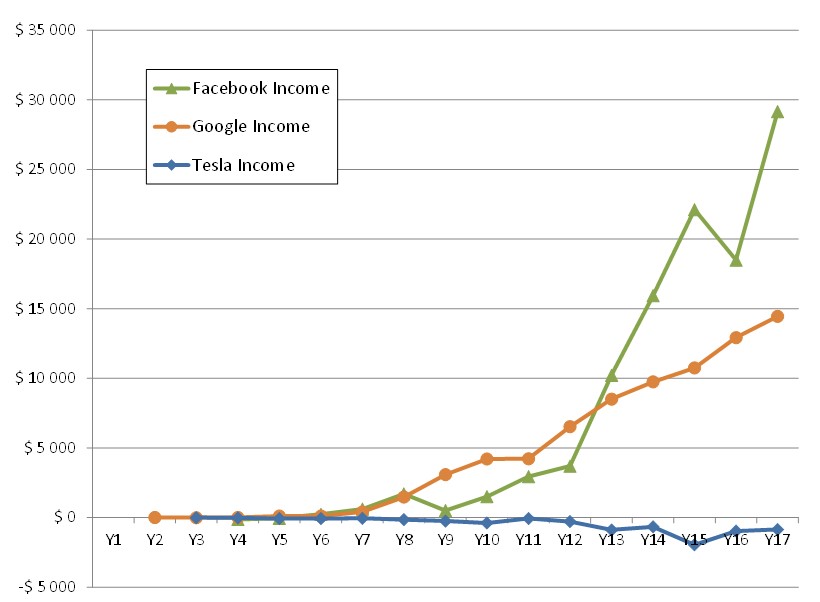

This may not be surprising and it has been said in the media. The GAFAs have generally benefited from the Covid crisis. So, as I was independantly doing in the recent years, I looked again at the growth of Google and Facebook as well as Tesla.

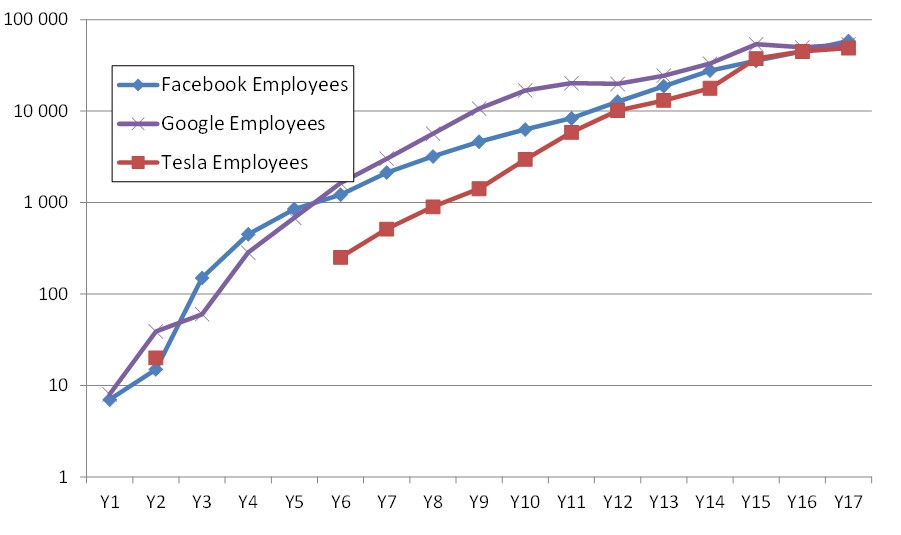

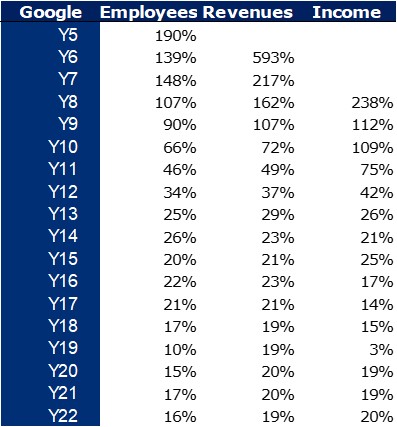

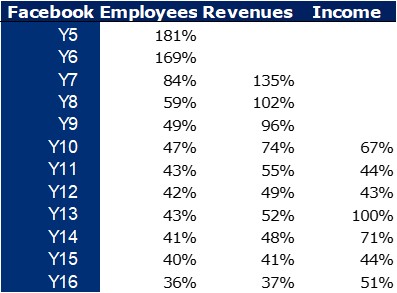

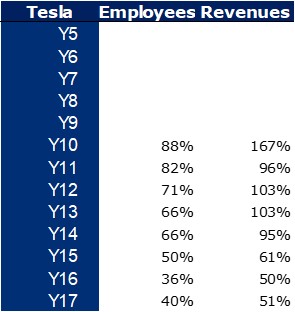

And here are my udpates abour revenue, income and employee growth of Google, Facebook and Tesla:

Revenues and profits are in millions of $. What is undoubtedly the most striking is the similarity of the growths of the three actors and of course the fact that all these numbers are considerable, not to say extraordinary.

Typical of Silicon Valley startups, the growth is often above 100% in the early years decreasing to about 40% after a few years and still above 15% after 20 years. This means respectively doubling the numbers every year, every two years and every five years.