I must admit I did not know Bill Janeway. I should have, given his long expertise in venture capital. His recent contribution was mentioned by many including Nicolas Colin and on a personal note, friends from IMF. They just mentioned to me 8 videos which seem absolutely brilliant: Venture Capital in the 21st Century.

I just watched the third: Evaluating Venture Capital Performance | #3 | Innovation in the 21st Century. Here are the slides.

Janeway reviews the performance of Venture Capital firms and recent changes in the venture capital market. He starts by summarizing the stylized facts of venture capital returns (highly skewed, very persistent, and correlated with the stock market). VC capital increased rapidly in the late 1990s, peaking in 2000. VC returns have since settled down, with longer holdings and fewer IPOs. But with the climate of zero real interest rates since 2008, new unconventional investors (private equity, hedge funds, etc.) have waded into venture financing directly, hunting for the high returns of the next big tech giant. A “Unicorn Bubble” has developed as a result, where dubious firms have been financing their growth by selling illiquid securities at inflated prices to deep-pocketed investors with little expertise or control over the entrepreneur. This may have implications on the long-term link between venture financing and technological innovation.

I just copied a few screenshots:

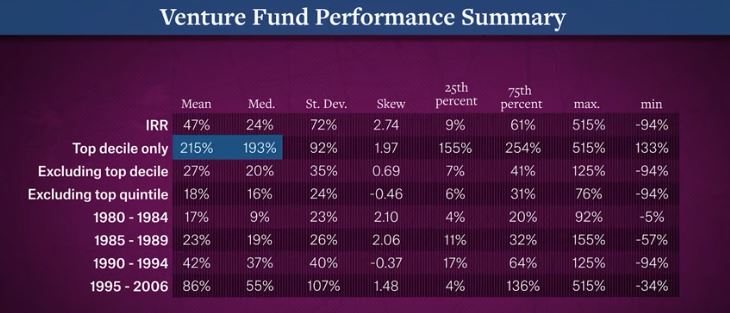

Venture capital is highly skewed and follows a power law, just like startup success models.

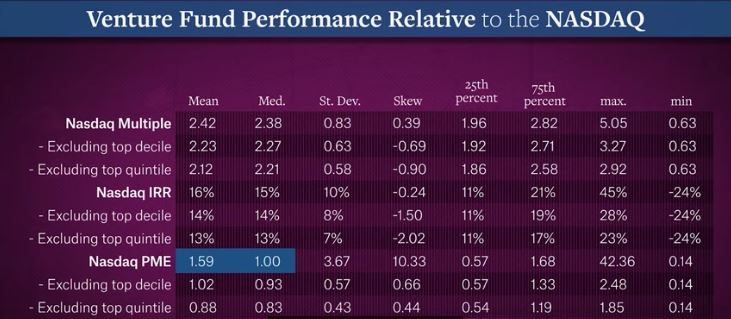

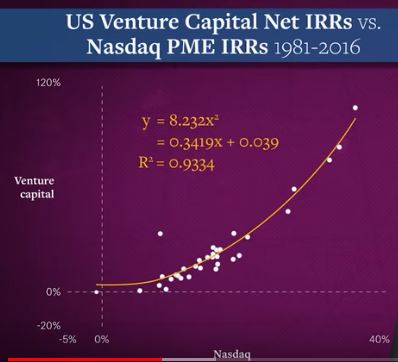

Venture capital returns are highly correlated to those of Nasdaq as shown above and below, so… ?

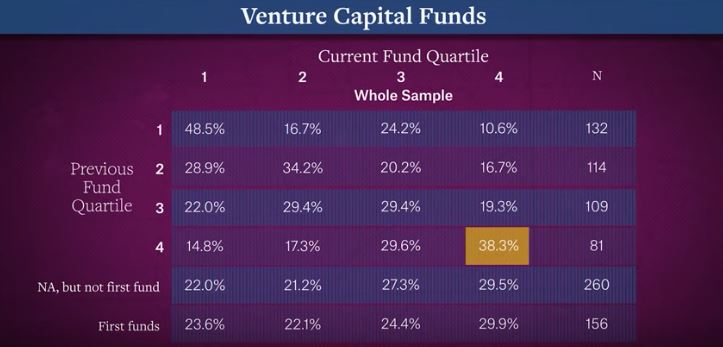

Good VCs are good and bad VCs are bad.

So…

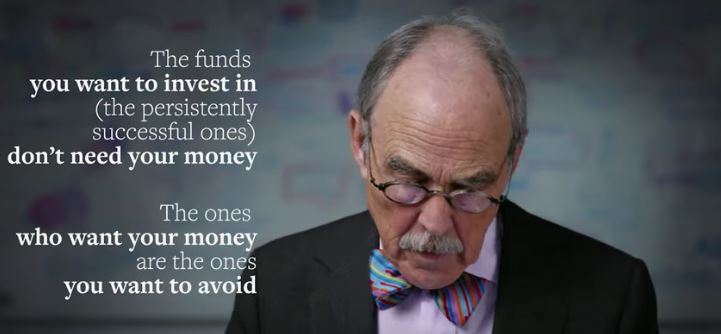

“The message here to limited partners is very clear.

A blind allocation to venture capital, just allocating a fixed proportion to venture capital runs the major risk of what’s known as adverse selection.

The funds you want to invest in, the persistently successful ones, don’t need your money.

The ones who want your money are the ones you want to avoid.”

This is the title of a great article from the not less great New Yorker, dated November 23, 2020 and written by Charles Duhigg:

How Venture Capitalists Are Deforming Capitalism, Even the worst-run startup can beat competitors if investors prop it up. The V.C. firm Benchmark helped enable WeWork to make one wild mistake after another—hoping that its gamble would pay off before disaster struck.

Illustration by Golden Cosmos (from the New Yorker article)

I am infringing copyright here and hope the magazine and author will forgive me. But the illustration says so well what the author describes! Yes, for a few years now, venture capital has become a crazy money spending machine.

I already posted blog about VC crises as over time the activity as evolved. From frugal investors in technology in the 60s and particularly in the 70s (Apple, Microsoft,..) and 80s (Cisco, Sun, …) The internet “bubble” was not the first period of hubris, there was one in the early eighties with tons of PC clones. But the real hubris came with the social media. Today, startups raise hundreds of millions of dollars before going public and experience huge, huge losses even at IPO as you may want to check in my 600 startups analysis (and it will be probably even worse in my 700 startups analysis to come). Here are past articles:

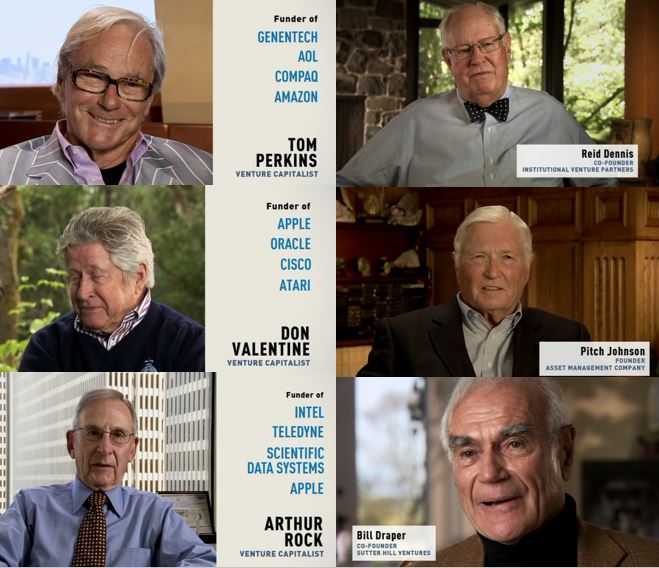

At this point read carefully what venture capital was according to the author of the article: From the start, venture capitalists have presented their profession as an elevated calling. They weren’t mere speculators—they were midwives to innovation. The first V.C. firms were designed to make money by identifying and supporting the most brilliant startup ideas, providing the funds and the strategic advice that daring entrepreneurs needed in order to prosper. For decades, such boasts were merited. Genentech, which helped invent synthetic insulin, in the nineteen-seventies, succeeded in large part because of the stewardship of the venture capitalist Tom Perkins, whose company, Kleiner Perkins, made an initial hundred-thousand-dollar investment. Perkins demanded a seat on Genentech’s board of directors, and then began spending one afternoon a week in the startup’s offices, scrutinizing spending reports and browbeating inexperienced executives. In subsequent years, Kleiner Perkins nurtured such tech startups as Amazon, Google, Sun Microsystems, and Compaq. When Perkins died, in 2016, at the age of eighty-four, an obituary in the Financial Times remembered him as “part of a new movement in finance that saw investors roll up their sleeves and play an active role in management.”

But some famous experts of innovation are quoted about the current situation:

Steve Blank: “I’ve watched the industry become a money-hungry mob. V.C.s today aren’t interested in the public good. They’re not interested in anything except optimizing their own profits and chasing the herd, and so they waste billions of dollars that could have gone to innovation that actually helps people.” and his answer to the crisis is quite strong: “The first time you see a venture capitalist prosecuted for failing to uphold their duty as a board member, you’re going to see Silicon Valley transform overnight. All it takes is one V.C. doing a perp walk and everyone gets the message—you’re responsible, you have a legal duty, and if you do things that are bad for society you’ll be called to account.”

Martin Kenney, the professor at the University of California, Davis, said, “Obama loved Silicon Valley and V.C.s, and Trump craved their approval.” He went on, “Regulators have been totally defanged from doing real investigations of venture-capital firms. I think people are finally waking up to the damage the tech industry and V.C.s can do, but it’s slow going.” Today’s V.C.s, “money-losing firms can continue operating and undercutting incumbents for far longer than previously.”

Josh Lerner, a professor at Harvard Business School: “Proclaiming founder loyalty is kind of expected now.”

A Harvard Business School professor, Nori Gerardo Lietz, noted that the document exposed WeWork’s “byzantine corporate structure, the continuing projected losses, the plethora of conflicts, the complete absence of any substantive corporate governance, and the uncommon ‘New Age’ parlance,” the S-1 was “misleading, and probably fraudulent.”

I will finish my post with a quote mentioned by Bruce Dunlevie, the partner from Benchmark who was one the WeWork boardmember, a task he did not handled perfectly even if not that badly. Nothing to add. “Power tends to corrupt, and absolute power corrupts absolutely.”Lord Acton and the rest of the quote (not mentioned in the article) is “Great men are almost always bad men…”

This morning, I was participating to a workshop about startups and one question came about the relationships with investors entrepeneurs are trying to attract and invest in their company. I told them it could be frustrating for many reasons, often because VCs never say no but decline too often to invest too. The best illustration comes from Something Ventured, a documentary movie I never stop celebrating. The Apple case is close to being hilarious. You find the extract beginning around minute 51 in the video:

and here is the text: [Narrator] In 1976, the computer was about to get personal. […] For venture capitalists, this represented the opportunity of a lifetime.

[Perkins Chuckles] We turned down Apple Computer. We didn’t – We didn’t even turn it down. We didn’t agree to meet with Jobs and Wozniak.

[Reid Dennis] Oh, that would have been a fabulous investment if we had made it, but we didn’t. We said, “Oh, no, we’re not really in that business.”

[Pitch Johnson] “How can you use a computer at home? You’re gonna put recipes on it?”

[Bill Draper] I sent my partner down to look at Apple. He came back and he said “Guy kept me waiting for an hour, and he’s very arrogant.” And, of course, that’s Steve Jobs! I said, “Well, let’s let it go.” That was a big mistake.

[Narrator] In 1976, the only people who believed in the personal computer… were the geeks and nerds who gathered at Homebrew Computer Clubs.

[Bushnell, founder & CEO of Atari] They needed an investment, and, uh, they offered me a third of Apple Computer for $50,000… and I said, “Gee, I don’t think so.” I could have owned a third of Apple Computer for $50’000. [Sighs] A big mistake. But I said, “Call Don Valentine.”

[Valentine] So we had our meeting. I went to Steve’s house. And we talked, and I was convinced it was a big market… just embryonically beginning. Steve was in his Fu Manchu look, and his question for me- “Tell me what I have to do to have you finance me.” I said, “We have to have someone in the company… who has some sense of management and marketing and channels of distribution.” He said, “Fine. Send me three people.” I sent him three candidates. One he didn’t like. One didn’t like him. And the third one was Mike Markkula. Mike Markkula worked for me at Fairchild before he went to Intel.

[Markkula] I said, “Okay.” ‘Cause that’s what I did on Mondays. I was retired. [Chuckles] I think I was 32 when I retired from Intel. But one day a week, I would help people start companies and write business plans. I did it for free, just for the interaction with bright, uh, people… So I went over and talked to the boys. [Laughs] The two of them did not make a good impression on people. They were bearded. They didn’t smell good. They dressed funny. Young, naive. But Woz had designed a really wonderful, wonderful computer. […] And I came to the conclusion that we could build a Fortune 500 company in less than five years. I said I’d put up the money that was needed.

[Narrator] Mike Markkula came out of retirement, becoming the president and C.E.O. of Apple. And the first call he made was to Arthur Rock. Arthur would have missed Apple if it weren’t for Mike Markkula.

[Rock] Jobs and Wozniak came up to see me, and they were very unappealing. Goatee, long hair [Muttering] Markkula said, “Well, before you make up your mind, there’s a computer show. You ought to come down and see what’s going on.” And he did. He thought somethin’ was happenin’. He wasn’t quite sure what. And there was this booth with everybody around it. I couldn’t even get next to it. And it was the Apple booth.

Then I got a call from Don Valentine. [Chuckles] “I want to put some money in that company” I said, “Okay, you gotta come on the board then.”

You know in the venture capital business, if you look at 200 deals, and you, you might do 10 of’em, and you will think they’re all great, and if one of’em is great, then you’re in the hall of fame.

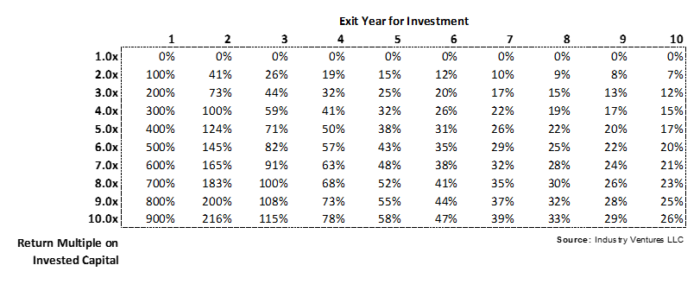

In venture capital, returns on investments is the ultimate metric and although it is not very difficult to understand, there are many little tricks worth knowing about!

The reason of this short post is a recent article my friend Fuad advised me to read from the Financial Times : The parallel universe of private equity returns by Jonathan Ford. If you are not a subsciber to the FT (and I am not), you may not be able to read the article so here are short extracts: “Ever wondered about the extraordinary performance figures that listed private equity firms trumpet in their official stock market filings? […] Not only do the firms generate stratospheric numbers — far higher than anything produced by the boring old stock market — but they can apparently do it year in, year out, with no decay in returns. […] The reality is that these consistent IRRs show nothing of the kind. What they actually demonstrate is a big flaw in the way the IRR itself is calculated.”

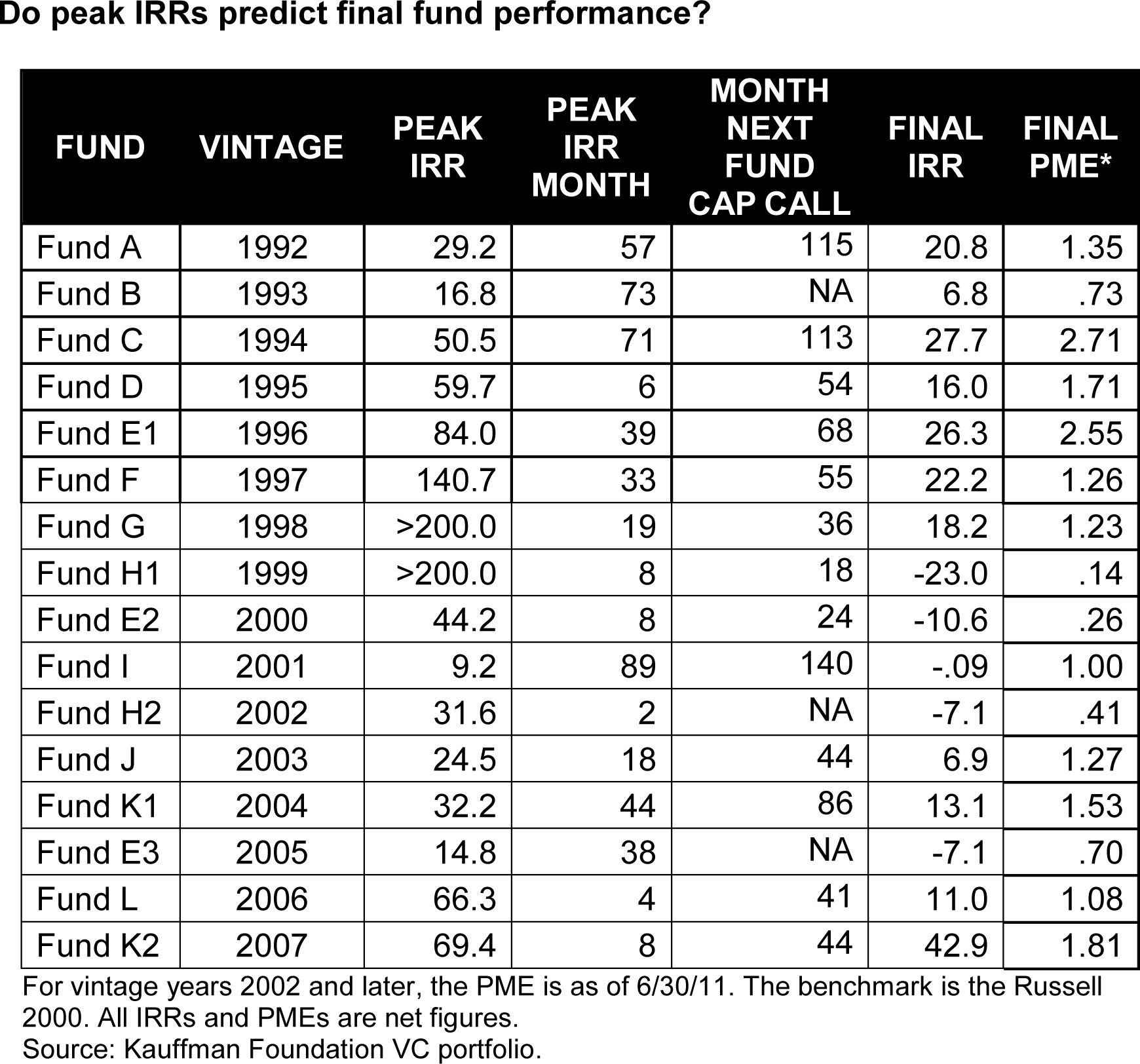

When I looked at venture capital (VC) returns in the past, I learned you must carefully look at what IRR means. It looks simple at first sight as the next table shows, just simple math:

So the first question you care about is what matters: IRRs or multiples? And my simple answer is “it depends”. Up to you!

Secondly, measuring returns makes a lot of sense when you have your money back. Of course! But IRR and multiples can also be measured while you are still invested and when your investment is not liquid, which is the case for private companies in which invests private equity (PE) – venture capital belongs to PE. You can have a look at a former post of mine, Is the Venture Capital model broken? and among other figures look at this:

The VC performance according to the Kauffman foundation

The peak IRR is measured when your assets are not liquid whereas the final IRR is when you have your money back… A fund as usually a 10-year life (or 120 months) and you can check the peak IRR month.

Even more tricky, the money is called by periods to make the holding as short as possible: basically, when the money is needed to invest, though you commit to it for the full life of the fund. Measuring the real IRR begins to be complicated but what matters to me is the multiple from the day of commitment to the finaldah when the money is back… And to you?

A final point I love to mention all the time is that VC is not so much about a portfolio of balanced investments. In the same post mentioned above, I added two links, and one of the best quote is “Venture capital is not even a home run business. It’s a grand slam business.”

“Prediction is very difficult, especially about the future.” attributed to Niels Bohr.

I was asked yesterday which startups I knew were the most promising, not to say the greatest. So I prefer to refer you to the quote above as I did not understand the potential of Google and Skype when I first heard of them. I am less shy of my lack of talent as this difficulty in predicting has been acknowledged by others.

So I did a little search and found again some more examples from again the antiportfolio of BVP (Bessemer Venture Partners) as well as from the book The Business of Venture Capital by Mahendra Ramsinghani. Enjoy!

First from the book The Business of Venture Capital on page 207:

Legendary investor Warren Buffet admired Bob Noyce, cofounder of Fairchlid Semiconductor and Intel. Buffet and Noyce were fellow trustees at Grinnell College, but when presented, Buffet passed on Intel, one of the greatest investing opportunities of his life. Buffet seemed “comfortably antiquated” when it came to new technology companies and had a long-standing bias against technology investments.

Peter O. Crisp of Venrock adds his misses to the list: One “small company in Rochester, New York [came to us, and one of our junior guys] saw no future [for] this product… that company, Haloid, became Xerox.” They also passed on Tandem, Compaq and Amgen.

ARCH Venture Partners missed Netscape – that little project Marc Andreessen started at the University of Chicago. An opportunity that, according to Steven Lazarus, would have been worth billions! “We just never knocked at the right door,” he would say. Eventually, ARCH decided to hire full-time person to just keep tabs on technology coming out of the universities to “make certain we don’t miss that door next time.”

Deepak Kamra from Canaan Partners comments on his regrets: “Oh, God, I have too many … this gets me depressed. A friend of mine at Sun Microsystems called and asked me to meet with an engineer at Xerox PARC who had some ideas to design a chip and add some protocols to build what is now known as a router. The drivers of bandwidth and Web traffic were strong market indicators, and he was just looking for $100,000. I really don’t do deals that small and told him lo raise some money from friends and family and come back when he had something to show” That engineer was the founder of Juniper Networks. He got his $100,000 from Vinod Khosla. Khosla, then with KPCB, added an IPO to his long list of winners. Juniper slipped out of Kamra’s hands because it was too early.

And of course, those were frothy times when everyone was deluged with hundreds of opportunities each day.

KPCB missed an opportunity to invest in VMWare because the valuation was too high: a mistake, according to John Doerr.

Draper Fisher Jurvetson (DFJ) was initially willing but eventually passed on Facebook (ouch!), as the firm believed the valuation was too high at $100 million pre-money.

KPCB, not wanting to be left out of an opportunity like Facebook, invested $38 million alt a $52 billion valuation.

Tim Draper of DFJ, turned down Google “because we already had six search engines in our portfolio.”

K. Ram Shriram almost missed his opportunity to invest in Google when he turned the founders away. “I told Sergey and Larry that the time for search engines had come and gone but I am happy to introduce you to all the others, who may want to buy your technology. But six months later, Ram Shriram, who had once turned Google down, now invested $500,000 as one of the first angel investors.

Now some examples of the updated BVP antiportfolio:

AirBnB: Jeremy Levine met Brian Chesky in January 2010, the first $100K revenue month. Brian’s $40M valuation ask was “crazy,” but Jeremy was impressed and made a plan to reconnect in May. Unbeknownst to Jeremy, $100K in January became 200 in February and 300 in March. In April, Airbnb raised money at 1.5X the “crazy” price.

Facebook: Jeremy Levine spent a weekend at a corporate retreat in the summer of 2004 dodging persistent Harvard undergrad Eduardo Saverin’s rabid pitch. Finally, cornered in a lunch line, Jeremy delivered some sage advice, “Kid, haven’t you heard of Friendster? Move on. It’s over!”

Atlassian: Byron Deeter flew straight to Atlassian in 2006 when he caught wind of a developer tool from Australia (of all places!). Notes from the meeting included “totally self-financed, started with a credit card” and “great business, but Scott & Mike don’t ever want to be a public company.” Years and countless meetings later, the first opportunity to invest emerged in 2010, but the $400m company valuation was thought to be a tad “rich.” In 2015, Atlassian became the largest tech IPO in Australian history, and the shares we passed on are worth more than a billion dollars today.

Tesla: In 2006 Byron Deeter met the team and test-drove a roadster. He put a deposit on the car, but passed on the negative margin company telling his partners, “It’s a win-win. I get a great car and some other VC pays for it!” The company passed $30B in market cap in 2014. Byron paid full price for his Model X.

eBay: David Cowan passed on the Series A round. Rookie team, regulatory nightmare, and, 4 years later, a $1.5 billion acquisition by eBay.

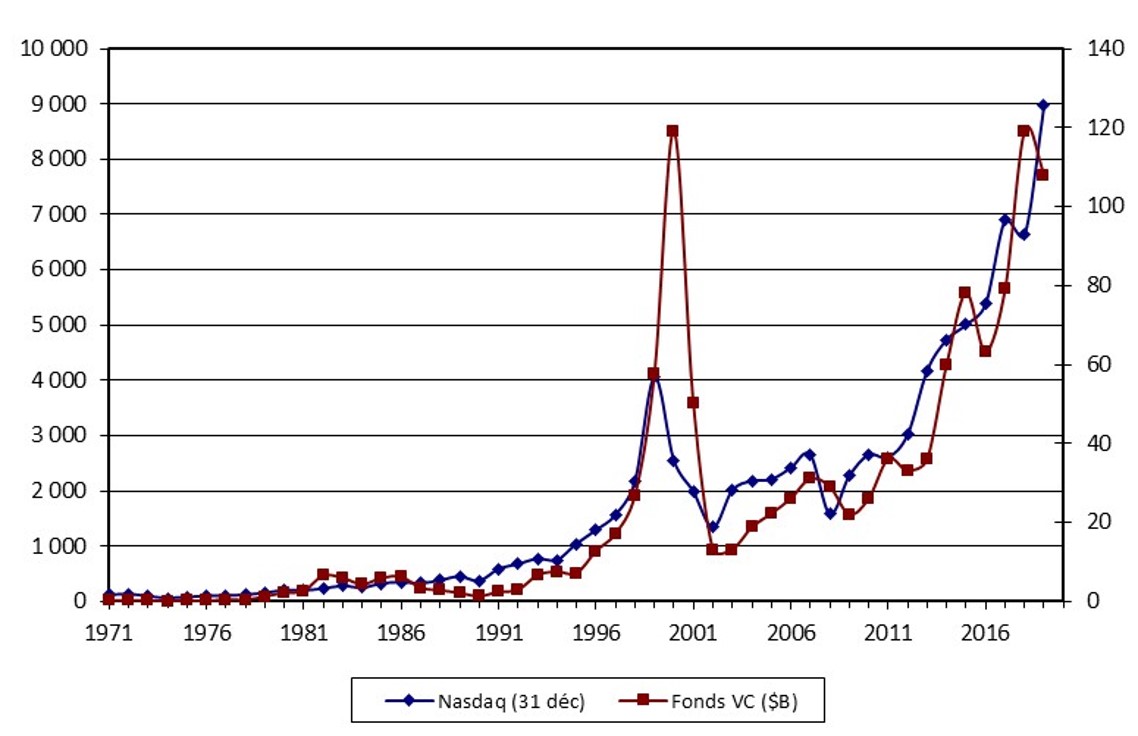

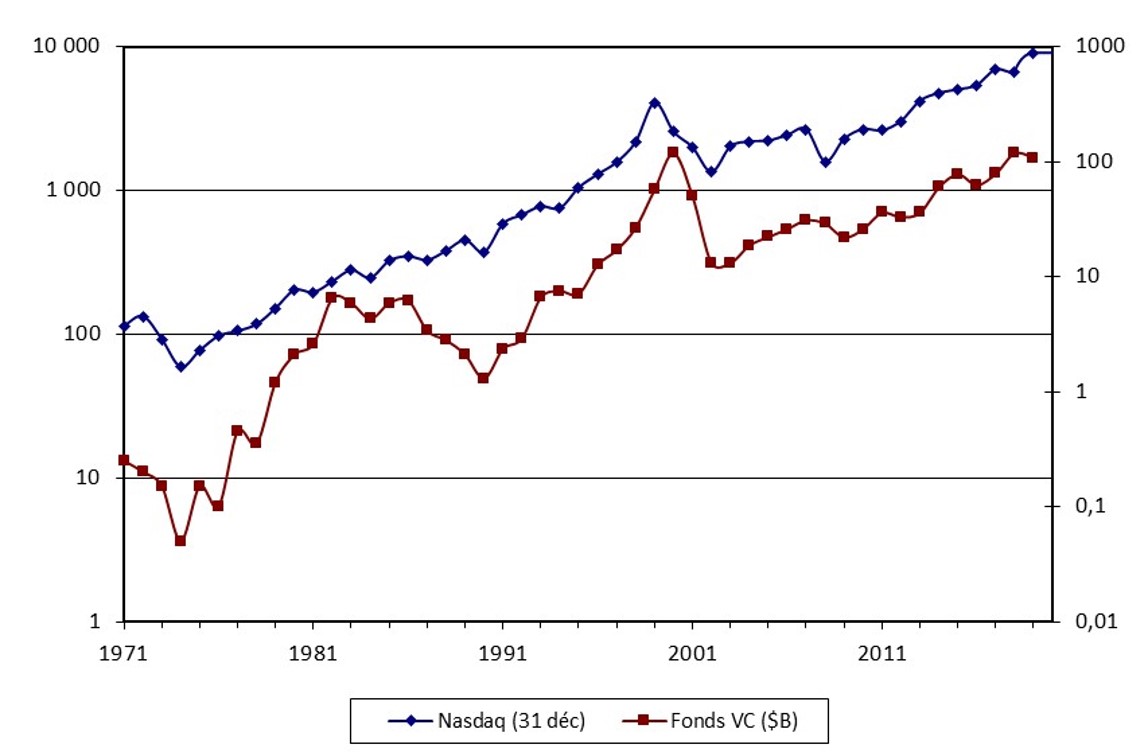

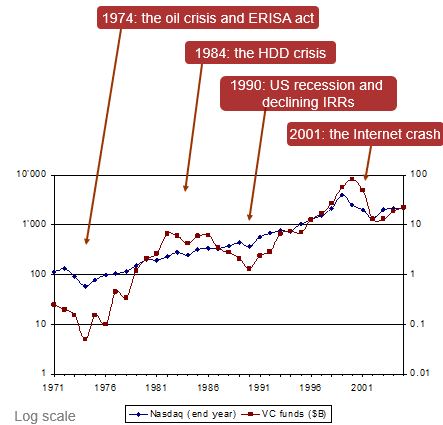

When I published the book which is the “raison d’être” of this blog, I had shortly analyzed the correlations between venture capital level in the USA, the Nasdaq index and their relationship to “crises”. Each peak and bottom level could be easily explained. I updated it to today levels with idea of revisiting when we zill be out of the Covid19 crisis. Comments welcome!

I just learnt the death of Don Valentine, the founder of Sequoia. For those of you who may not know him, you could visit my previous posts that mentions him, either through tag #sequoia or even better search Valentine. Just be aware he invested in Atari, Apple, Oracle, Cisco, Electronic Arts…

Or you may just read some of my favorite quotes of him:

“There are only two true visionaries in the history of Silicon Valley. Jobs and Noyce. Their vision was to build great companies … Steve was twenty, un-degreed, some people said unwashed, and he looked like Ho Chi Minh. But he was a bright person then, and is a brighter man now … Phenomenal achievement done by somebody in his very early twenties … Bob was one of those people who could maintain perspective because he was inordinately bright. Steve could not. He was very, very passionate, highly competitive.”

“Well, look, we’ll put up all the money, you put up all the blood, sweat and tears and we’ll split the company”, this with the founders. Then if we have to hire more people, we’ll all come down evenly, it will be kind of a 50/50 arrangement. Well, as this bubble got bigger and bigger, you know, they were coming and saying, “Well, you know, we’ll give you, for all the money, 5 percent, 10 percent of the deal.” And, you know, that it’s a supply and demand thing. It’s gone back the other way now. But, in starting with a team, it’s a typical thing to say, well, somewhere 40 to 60 percent, to divide it now. If they’ve got the best thing since sliced bread and you think they have it and they think they have it, you know, then you’ll probably lose the deal because one of these guys will grab it.”

I just read about Sebastian Quintero’s data analyses on start-ups on his web site Towards Data Science. Thanks Martin H. 🙂 I was really fascinated about his original way of looking at them, their failure rate, the valuation prediction, their runway between rounds, and his Capital Concentration Index or Investor Cluster Score. You should read them.

Of course, it rang strong bells with all the data analyses I have done in the recent past 8see end of the post if you wish)

So as an appetizer to Quintero‘s work, here are a couple of figures taken from his site…

Introducing the Capital Concentration Index™ Where c is the percentage capital share held by the i-th startup, and N is the total number of startups in the defined set. In general, the CCI approaches zero when a sector consists of a large number of startups with relatively equal levels of capital, and reaches a maximum of 10,000 when a sector’s total invested capital is consolidated in a single company. The CCI increases both as the number of startups in the sector decreases and as the disparity in capital traction between those startups increases.

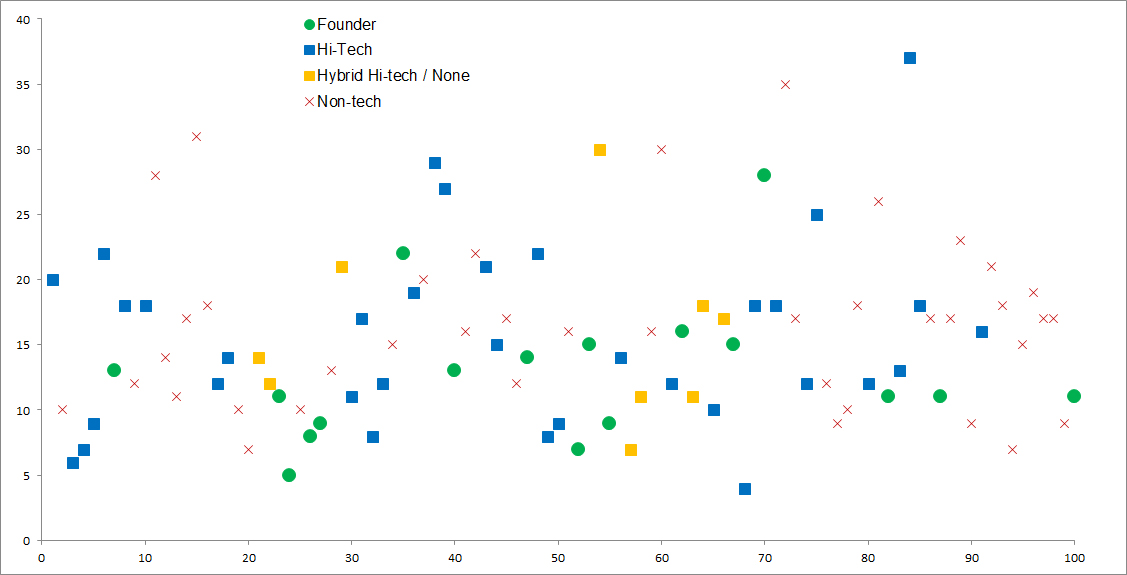

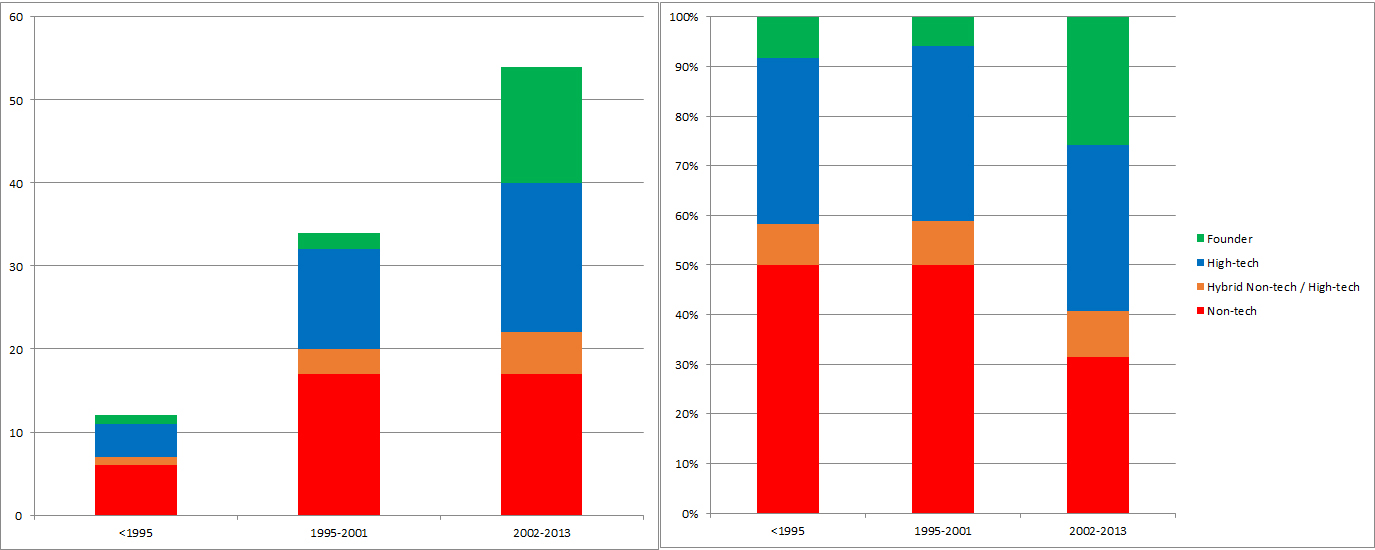

Yesterday, in Do Ex-Startup Founders Make The Best Venture Capitalists? I mentioned CB Insights analysis about the background of the top VCs, and expressed my doubts about comparing founders vs. non founders. So I used the Top100 list and had a different look: what about the background in high-tech or not? Here are some charts. Quick and dirty so do not take it as a scientific analysis. Still…

First a point of caution. This list is a little strange and the authors know better than me, but I am sure this list is not highly subjective… Now it seems founders were never a majority and VCs with no high-tech experience always a majority. Now what is puzzling is that these VCs are rather young and that a high majority of them having been in the business for less the 20 years… interesting. What would have been the results of the VCs active in the 70s and 80s? Not sure…

Also the change in the last 15 years is not the ratio with a tech background, but the ones who are founders has increased and the ones with no tech background has decreased…

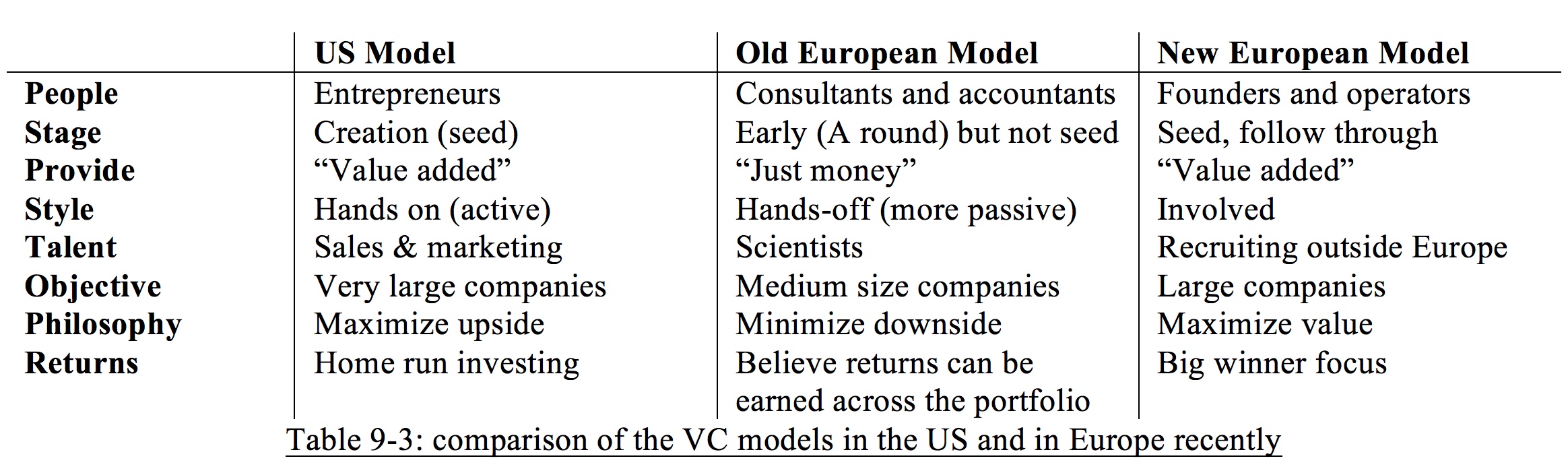

Interesting question as I have often claimed that there was a difference between US and European venture capitalist (VC), which had been also illustrated in the past by Tim Cruttenden (see below).

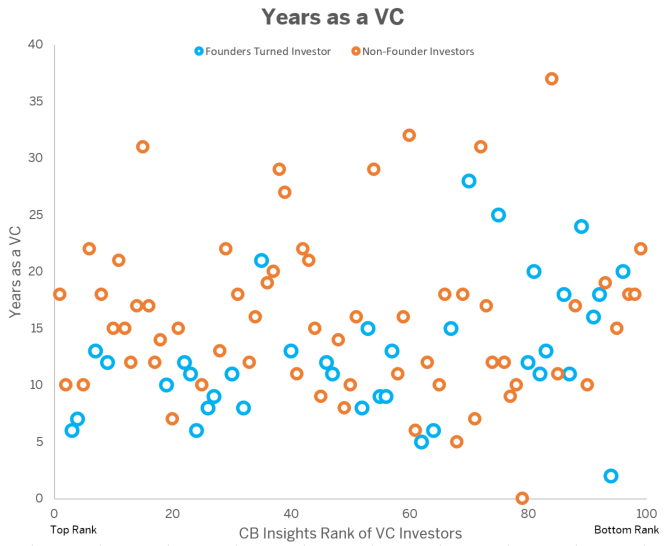

CB Insights, a leading firm analyzing data about start-ups, looked at the experience of VCs: Do Ex-Startup Founders Make The Best Venture Capitalists? The next figure illustrates their results and they additionally claim: “Of the 100 VCs, 38 founded or co-founded a company before becoming venture investors, while 62 did not. Six of CB Insights’ top 10 investors haven’t founded a company. That includes the top two: Benchmark’s Bill Gurley and the recently retired Chris Sacca.”

However interesting, I would have preferred a different analysis: how many had a direct experience in technology firms, whether in product / technology development or on the business sides such as sales or marketing compared to teh ones who were “only” consultants or bankers. This would be highly important as the value you bring t the board level may be entirely different. Look at what Tim Cruttenden explained in 2006.

Indeed Cruttenden says “entrepreneurs” too, but if we remember that Kleiner Perkins and Sequoia had a lot of managers more than entrepreneurs then, we might have obtained another measure of what makes a good VC…