In my previous post, I mentioned this anthology of articles compiled by Loup Cellard and Guillaume Heuguet. Consisting of six articles (5 of which are translated) and a long introduction by the authors, it is a most interesting dive into what this region represents from a historical and political point of view.

So here is what I noted:

– the authors restrain the influence of the counterculture in the origins of Silicon Valley. “The economic power and the culture of technical innovation of the region far precede the hippie movement.” [page 18] then “government contracts or the existence of a surplus of capital should probably be given as much importance as utopian imaginaries” [page 19].

– The authors go further regarding the ideological inclinations of Silicon Valley entrepreneurs. I have already expressed a certain skepticism on the subject but the debate remains interesting. The authors mention another book on this subject that I am not familiar with, Une histoire politique de la Silicon Valley (A Political History of Silicon Valley) by Fabien Benoit. I do not believe that the following statement is correct: “Stanford University, which specializes in hard sciences, has the particularity of not claiming intellectual property rights on patents developed within its walls.” [Page 19] The subject is well-known (see here) and I am surprised by such a statement. Mariana Mazzucato is also called to the rescue of the arguments and if I have also expressed strong nuances there, one can hardly doubt the influence of Fred Terman, HP and MIT well before the emergence of the counterculture.

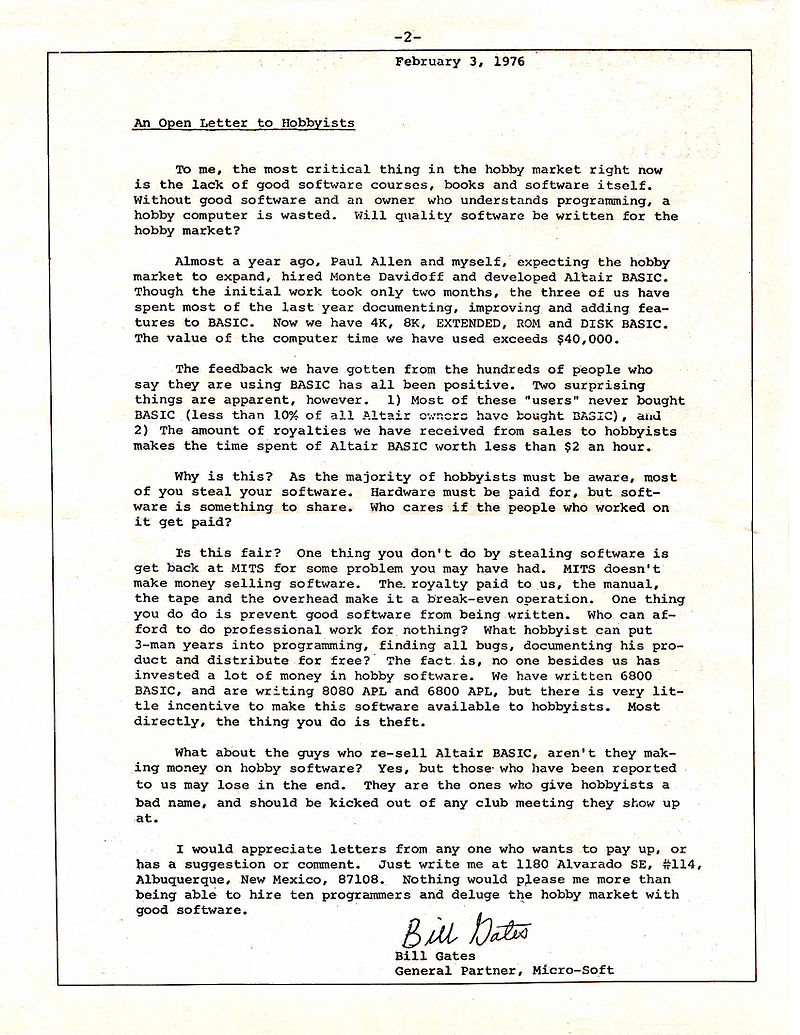

– In the same introduction, Bill Gates’ open letter to the Hobbyists of the Homebrew Computer Club is mentioned.

This introduction by the authors is fascinating and we have once again the confirmation of the complexity of the genesis of the region where hippies like Wozniak and engineers like Noyce often collaborated with the greatest respect. (See again this article for the curious, The tinkerings of Robert Noyce)

– The articles about design are surprising given how fashionable the subject has been (and had so far left me circumspect and silent). Fred Turner’s chapter Such Old Promises is an interesting analysis of the links between prototyping and Protestant puritanism! Ruha Benjamin’s article, translated as Le design est complice (Design is an Accomplice) goes much further. I take away the following strong statements: “Design Thinking is Bullh*t” and the author “urges practitioners to avoid jargon and trendy buzzwords and to engage more in self-criticism: what are the theoretical and practical effects of using the language of design to describe all our hopes, dreams, critiques and visions of change? What is gained and by whom in the process of associating such heterogeneous things under the rubric of design? […] I think one of the reasons it reigns is that it has managed to fold everything and anything under its agile wings”.

– The authors are very critical of some of the region’s personalities that they associate with the ancient world. Charlie Tyson’s Reactionaries invest (Les réactionnaires investissent) is an interesting analysis of Peter Thiel who would like to present himself as an intellectual. And the conclusion is: “The man himself remains a mystery […] who offers us the spectacle of a brilliant mind housed in a deformed personality, a man who has transformed his armchair philosophy into an imposed vision of the world”. The following chapter, Capital risks nothing (Le Capital ne risque rien( by Fabien Foureault is a fairly correct description of the history of venture capital. The only criticism I would make is that the transition from American roots to the history of the activity in France somewhat forgets the risks taken by the pioneers in the 60s and 70s. The criticism of venture capital remains well argued as follows: on three major criteria, VC is criticized:

+ a dysfunctional character that prevents stability through boom and burst cycles

+ a lack of social utility by moving towards short-term profitability that forgets the fundamental issues (climate, affordable health)

+ an unprofitable activity, at best with a low return of 8% in the long term. I discovered a researcher, Ludovic Phalippou, very critical of Private Equity in general which lack of transparency leads to undoubtedly very overestimated performances. I encourage you to read How Ludovic Phalippou Became the Bête Noire of Private Equity. The post-sciptum will undoubtedly make smile fans and connoisseurs of French venture capital…

– What can I say about the last two chapters? They are simply fascinating. First of all, Optimization Replaces Progress by Orit Halpern and Robert Mitchell. I had the intuition that optimization, a subject that is dear to me since it was at the heart of my doctoral thesis, was reaching the limits of progress. We no longer seek the best, but to be smart, intelligent, whether it be the city, mobility, education or war. The best being inaccessible, we simply seek to do better, and often while minimizing resources and costs… and to be resilient, which the authors describe as the ability not to be robust in a stable system, but to survive and win in an uncertain and unbalanced system. Disruption is not far away. The chapter’s conclusion may seem scary: “Instead of seeking utopian answers to our questions about the future, we focus on quantitative and algorithmic methods and logistics: how to move things from point A to point B, rather than asking where they should end up (or whether they should even be there)” [page 129].

– The last chapter is called Apocalypse Replaces Utopia by Dave Karpf. It is about long-termism. “The moral value of human life today is no different from that of potential post-humans who might come into existence in the distant future. From this premise, they come to fantastical and counterintuitive conclusions. They claim that economic growth, technological progress, and the prevention of existential risks, i.e. risks that could wipe out humanity (asteroid strikes, deadly super viruses, hostile artificial intelligence, etc.) matter most to humanity. Improving the situation of humanity today by addressing systemic inequalities, curing cancer, and preventing malaria are lesser initiatives. Today’s humans are merely the precursors of a post-human future scattered across space.” The promoters of such ideas are known and the author speaks of the Californian Ideology. I would like to think that they are only in the heads of a few deformed minds. The author concludes: “We should therefore recognize long-termism as a pernicious movement of thought. It is a philosophy that says we should not concern ourselves with the fate, dignity or injustices suffered by people living today, because these people do not matter more than those who will live millennia from now. […] It is a recipe that too easily excuses cruelty, suffering and social harm.

So this is a fascinating little book, which does not describe Silicon Valley, but through its roots and wings, some of its most astonishing excesses. And as I said in my previous post, this does not necessarily represent the majority, but at least a minority, perhaps tiny but undoubtedly very and too visible.

PS: for those who are not interested in long analyses, here is a rather funny video